$350 Million Canadian Duvernay Shale Deal

A U.S. shale pioneer buys in - promising for my favorite Duvernay producer

Yesterday morning, Northern Oil and Gas announced a large Duvernay acquisition. This has major value implications for the company I wrote about in From Money Pit to Money Maker, which owns a large nearby position with better well results.

It is a significant development - NOG was one of the original shale-era public companies and a pioneer in the space, with roots going back to the early Bakken days when the industry was first proving that oil could be produced economically from shale.

I was also involved with NOG early in my career and have been following them for nearly two decades. I led the first offering NOG completed coming out of the Global Financial Crisis, investing millions of dollars (for the investment firm I was at) into Northern at the start of their epic run from $6 to $40/share within a couple of years.

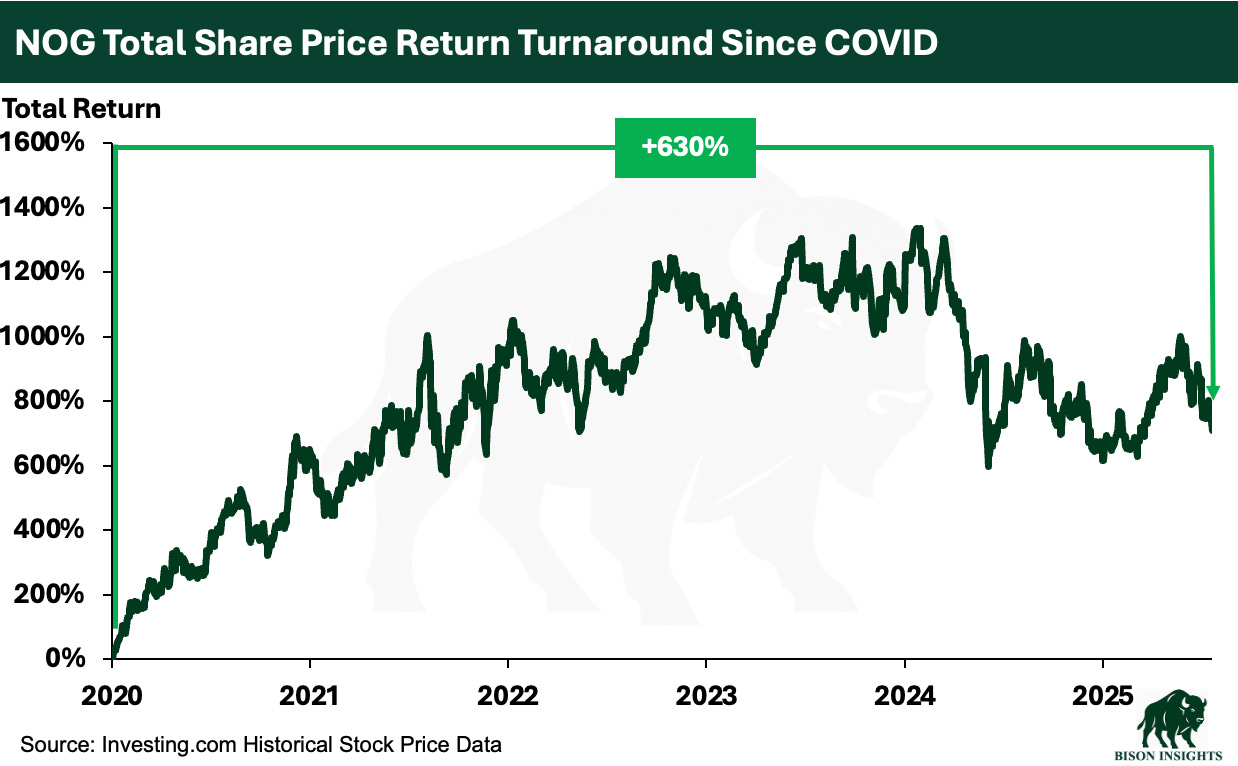

NOG’s history after that was rocky. The company became over-levered and ran into problems. They brought in their current CEO in early 2020. He helped guide the company through the COVID downturn, and the stock has gone from a low of roughly $3 per share during his first year as CEO to around $22 per share today:

Considering their long operating history and strong post-COVID track record, I think that NOG buying into the Duvernay is a major validation point for the play, and directly supports the thesis I laid out in From Money Pit to Money Maker, where the company I highlighted owns a core asset in the heart of the Canadian Duvernay oil window.

Read-Through Value Implication

NOG’s deal provides a fresh private market datapoint for Duvernay value from a credible, well known US shale buyer. Incidentally, the company I wrote about in From Money Pit to Money Maker owns a large Duvernay position that still appears to be receiving limited credit in the public market, despite strong early well results and a compelling development plan scheduled over the next several years.

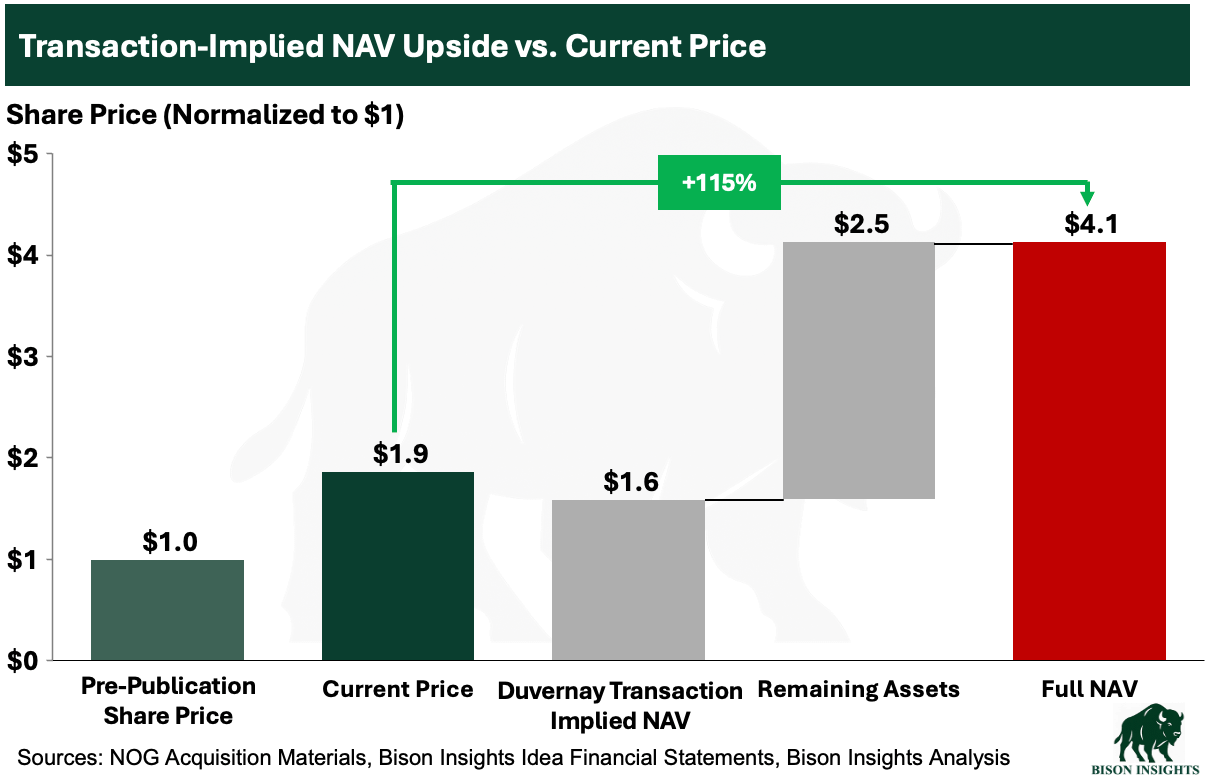

The value of this company’s Duvernay position implied by this morning’s transaction is nearly the entire value of the company, implying that investors are essentially receiving the remaining assets at a highly discounted valuation. The total company NAV, in my view, is much higher than the value at which the company is currently trading:

In the rest of this article, I’ll compare the transaction to this company’s Duvernay position in more detail and estimate what it implies for the stock.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance may not repeat itself.