$3.8 Billion Buyout of a Canadian Oil and Gas Company - What Could Come Next

NuVista bought at a 21% premium, the latest in a wave of deals. This company could be next.

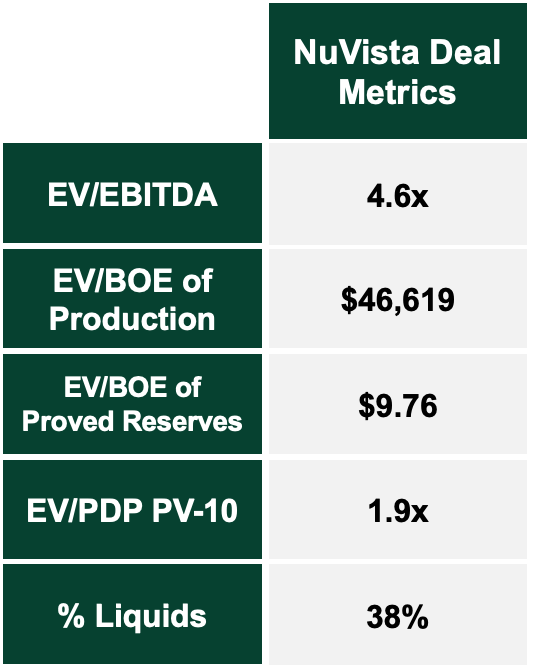

NuVista’s recent buyout by Ovintiv, a larger U.S.-traded oil and gas company, at a 21% premium demonstrates the strong appetite for high-quality Canadian producing assets right now. My view on the deal is that the buyer is paying fair value for NuVista, and a relatively high price compared to historical transaction multiples, both for Canadian assets overall and specifically for the Montney. Consolidation like this is healthy for the sector, and it’s encouraging to see formerly small-cap producers being acquired at fair valuations.

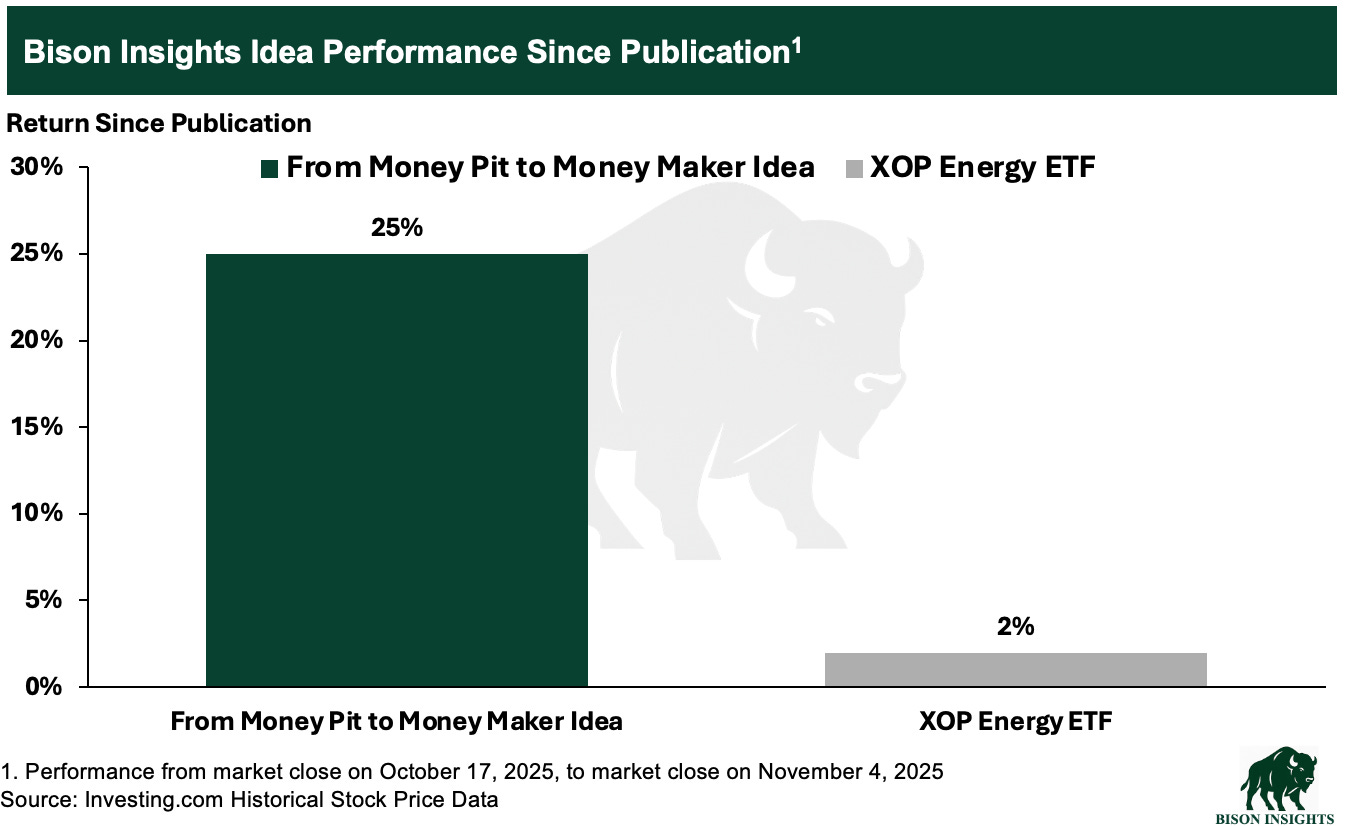

As the oil and gas consolidation trend continues, many are discussing which company could be bought out next. One potential buyout candidate that stands out for me is the company I wrote about in From Money Pit to Money Maker, which has meaningfully outperformed the broader oil and gas market, as measured by the XOP Energy ETF, since publication.

Even after the recent rally, the stock still trades at a steep discount to peers. One company in particular stands out as a natural acquirer, and a transaction between the two would make strong strategic and financial sense. Below is my analysis of why such a deal would be highly accretive to the buyer while offering existing shareholders a substantial premium.