45% Premium Buyout of Small-Cap Canadian Energy Company

I am finding compelling opportunities in small-cap energy - highlighted by ROK Resources premium buyout

ROK Resources ($ROK.V) was set to be one of my next Bison Insights ideas, but the company is being acquired at a 45% premium to the prior day’s closing price. Even so, the story is worth sharing because ROK is a great example of the incredible value still hiding in small-cap publicly traded energy stocks.

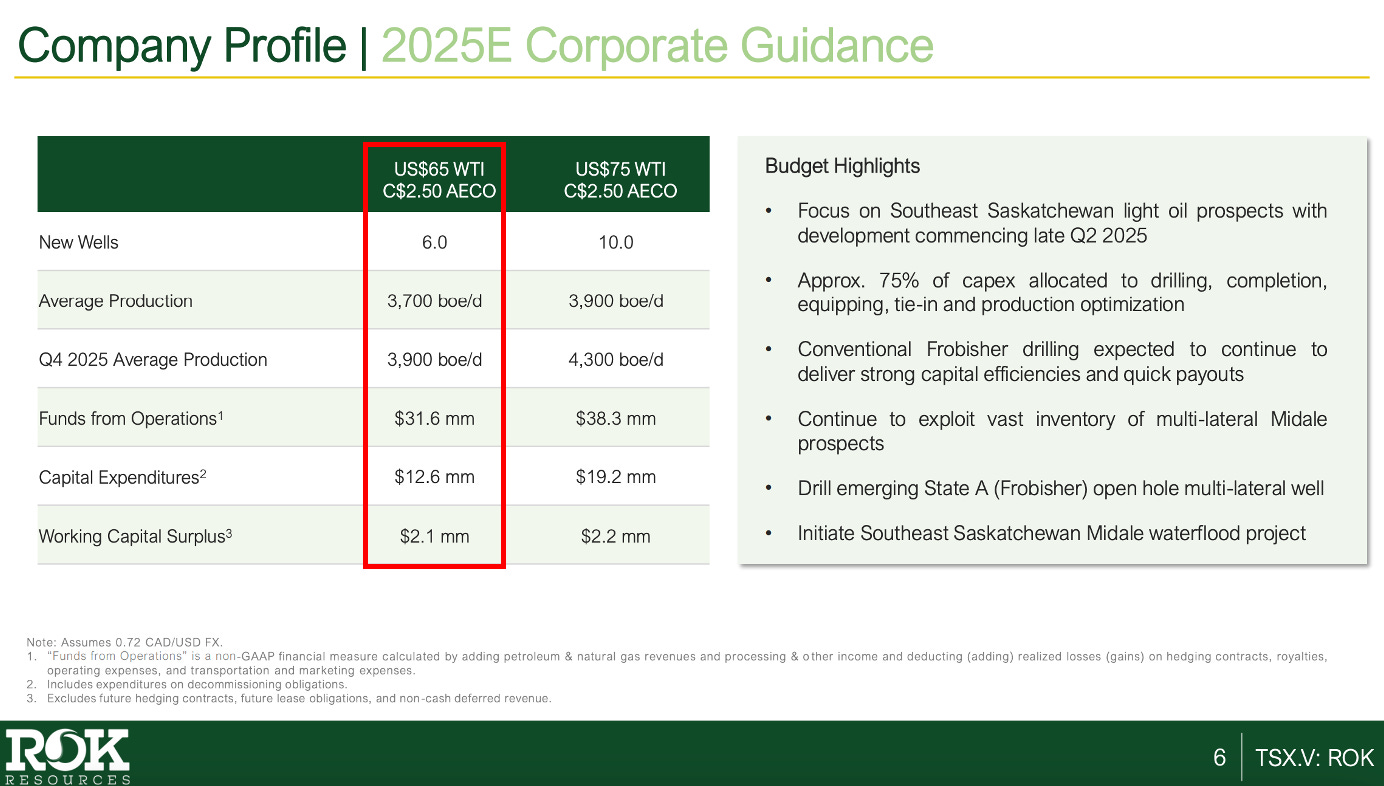

Before the transaction, ROK had an enterprise value of just under $40 million and was trading at an expected 2025 free cash flow yield of nearly 50%, based on ROK’s corporate guidance:

On top of that, ROK offered development upside and held a stake in a publicly traded lithium brine extraction business that accounted for a substantial portion of its market cap. And despite being a small company with some management transition risk, ROK carried a clean balance sheet with net cash, which helped reduce downside risk.

The acquisition is a reminder of how undervalued these names can be. While a 45% premium might sound like a great outcome, I believe it still undervalues ROK’s assets and future potential. This view is supported by the fact that a sophisticated private buyer is paying a 45% premium - indicating a belief they can still earn substantial returns on the acquisition beyond the premium.

This is exactly the kind of setup I look for in small-cap energy: high cash flow, hidden assets, limited downside, and huge potential upside. ROK will be gone soon, but there are more like it out there, and I look forward to continuing sharing them here.

*Disclaimer: Josh and funds Josh advises own ROK Resources shares and may buy or sell at any time without further notice. Bison Insights has a “cooling off” period for compliance where no shares are traded in a reasonable time period before and after publication. This article represents Josh’s opinion at the time of publication - there can be no assurance of return or accuracy. Any investment decision requires diligence and, if appropriate, an advisor should be consulted. Josh is not your advisor, and this is meant for general information and educational purposes and not as personalized investment advice. No personalized advice can or will be provided by Bison Insights. Past performance may not be indicative.

we know writing those deep dives takes time. You can share the names first and then follow up with deep dives later.

Honestly kind of annoyed at this takeout since there was also upside in the lawsuit against CNRL for their failure to transfer assets in 2022 as well.

Took about a month to accumulate a decent sized position.

They were Debt-free with the NCIB just getting online, warrant overhang gone as of 6 months ago, and their new wells are looking decent.

Still hopeful for a stronger offer.