$58 Billion Dollar Oil & Gas Merger: Deworsification Is Not a Strategy

A detailed look at how the Devon–Coterra merger compares with the "Moneyball" playbook behind my latest stock idea.

I recently highlighted the “Moneyball” company in the oil and gas space as my latest stock idea for Bison Insights. This company buys out-of-favor assets, improves capital allocation and operational efficiency, and generates cash. In some cases, it also sells assets at high prices to reduce leverage and fund the next acquisition.

The recent merger between Devon and Coterra stands in contrast to this Moneyball approach, with Devon effectively doing the opposite of “buy low, sell high” — Devon is issuing its own shares, which are trading at depressed levels today as an oil-weighted producer in a weak oil price environment, to acquire Coterra, a primarily natural gas company that is trading at a higher multiple after gas prices have risen over the past ~18 months and sentiment around gas has turned bullish.

The result is that Devon shareholders are being diluted on key cash flow and reserve value metrics:

The pro-forma entity expects to achieve $1 billion in synergies, but in my experience, such projections are often optimistic. Even if the claimed synergies are realized, they are not expected to be fully in place until 2027 and would barely offset the dilution Devon shareholders are absorbing today. Deals that rely on synergies to become accretive are rarely great transactions for shareholders, especially with substantial non-overlapping assets and operations.

By contrast, the company I wrote about in “Oil & Gas Moneyball” also recently completed a large acquisition - but followed the opposite playbook. It acquired assets at a depressed valuation and structured the transaction in a way that increased, rather than diluted, per-share value, in part by selling non-core assets at premium valuations to help fund the purchase. With no reliance on “synergies.”

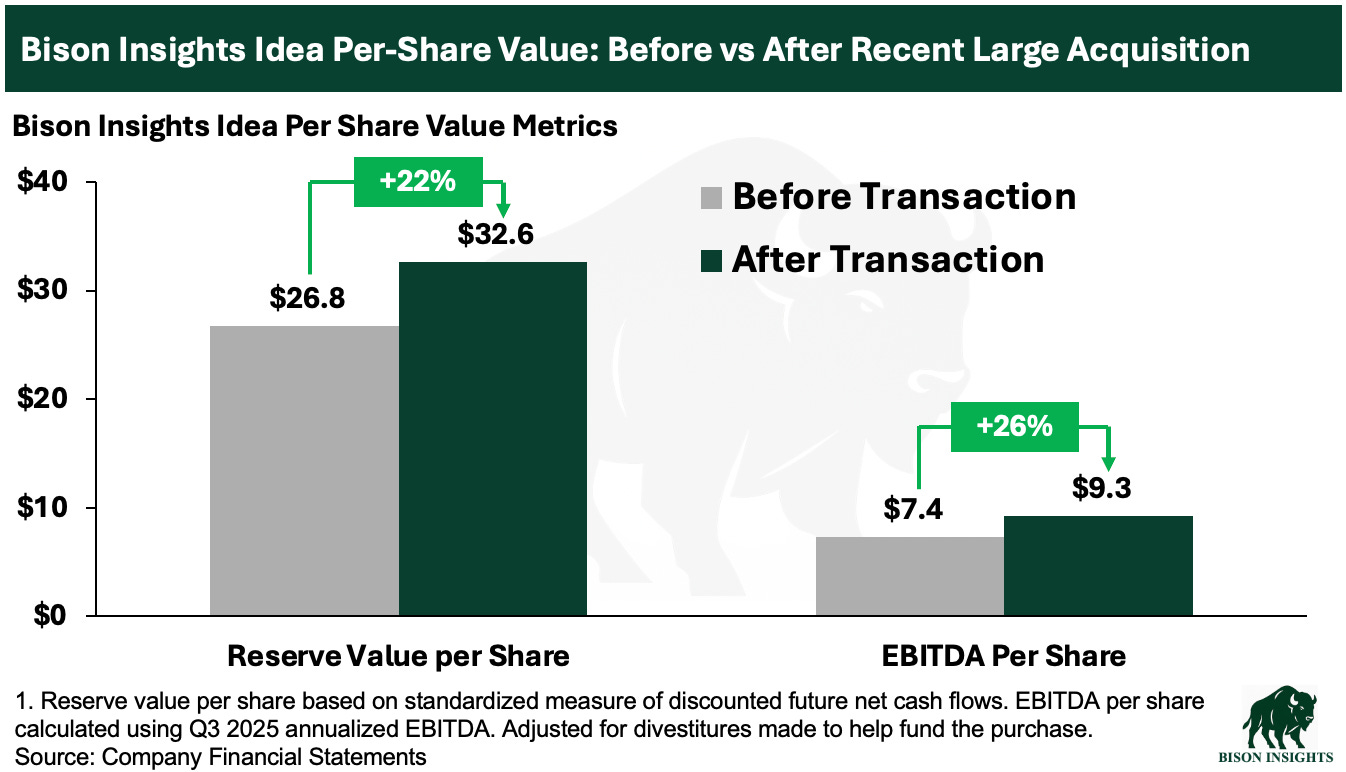

Here’s how the before and after per-share reserve values and cash flow stacked up in that transaction:

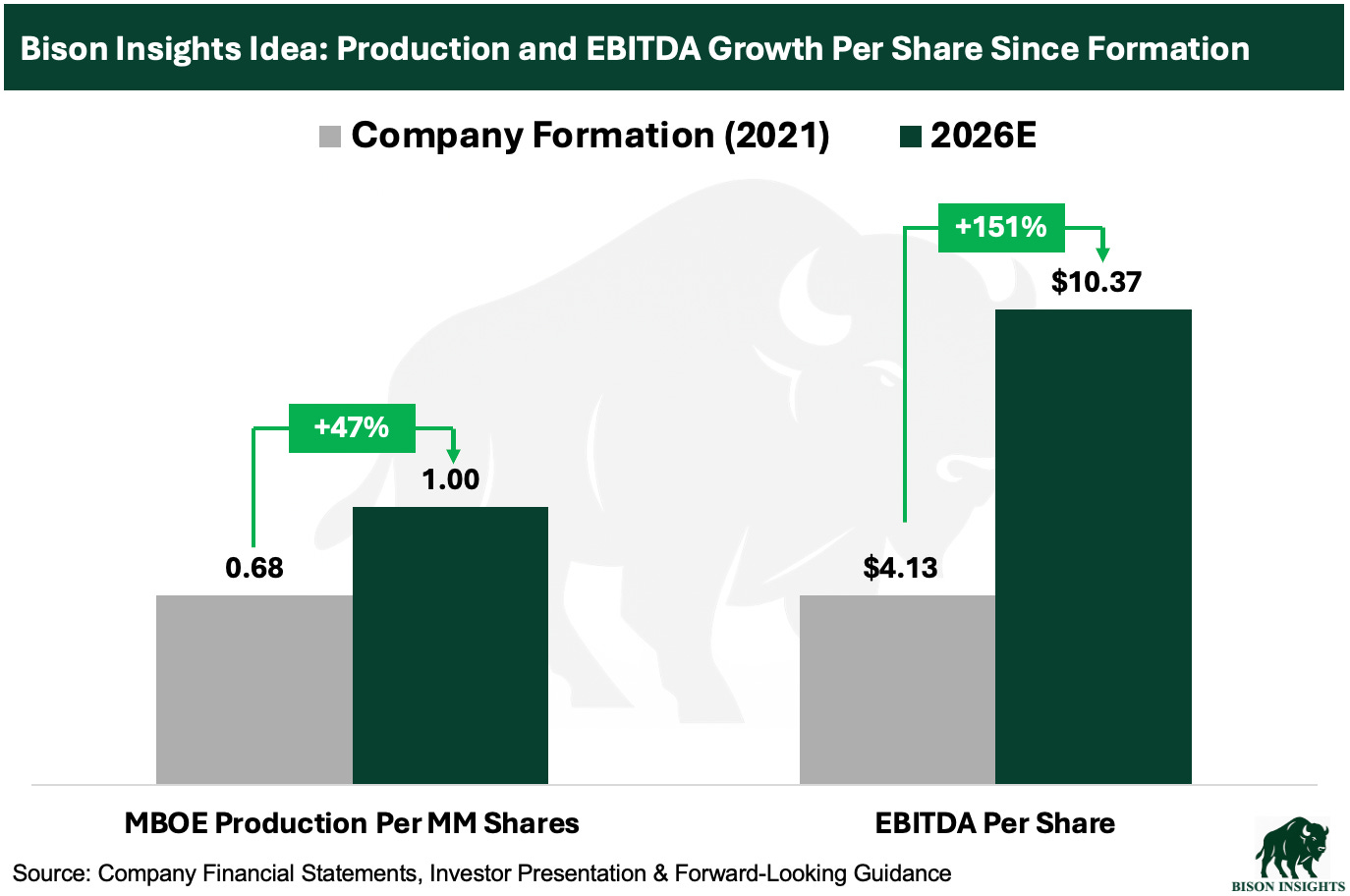

One year prior to this most recent transaction, the company also completed an accretive, natural gas-focused acquisition at the depths of the gas cycle in mid-2024, taking advantage of extremely depressed prices to execute a textbook “buy low” acquisition.

Taken together, these recent large acquisitions, as well as a number of smaller bolt-on acquisitions, have driven substantial increases in both cash flow and production per share since the company’s inception coming out of COVID:

What is interesting to note is that the reserve value per share and EBITDA per share of this company now roughly matches that of Devon’s. What is striking, however, is that while Devon trades at ~$40 per share, the “Moneyball” company I wrote about trades at a small fraction of that, despite nearly matching reserves and EBTIDA per share!

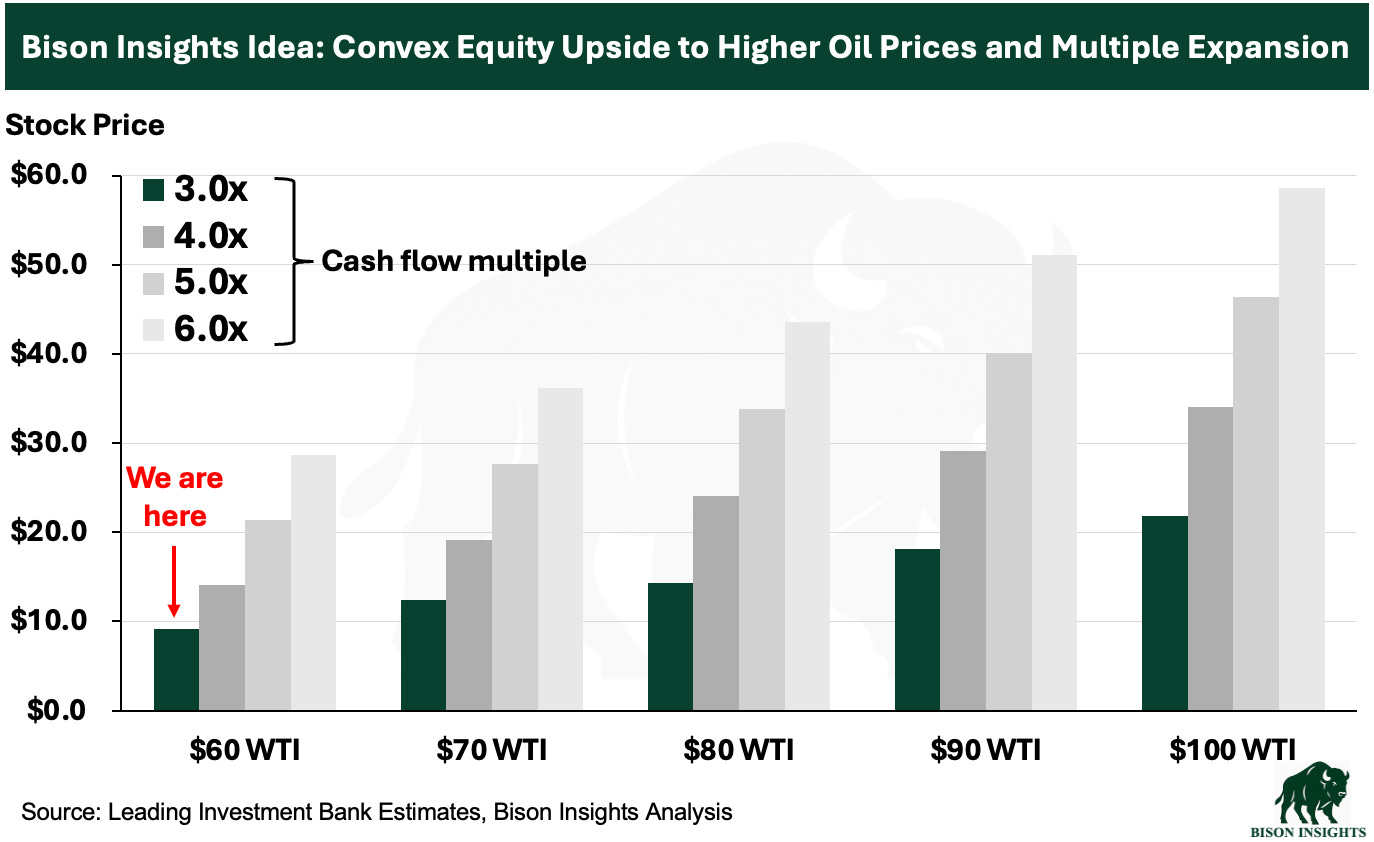

Indeed, the Moneyball company is like a coiled spring as the dust settles around its recent transactions. The market has yet to fully recognize the value of its business and has certainly not assigned any premium for its astute dealmaking. In a higher oil price environment, and with a higher cash flow multiple, the upside potential is significant:

Looking ahead, I expect this company to continue executing on its strategy, especially considering the track records of success of those leading the company. Long track records of intelligent capital allocation are rare in oil & gas, and they offer the promise of doing more with less.

That’s why I call it the “Moneyball” company of oil & gas. It’s misunderstood, undervalued, and positioned for outperformance.

Disclaimer: I own shares and related securities of companies referenced here and I may buy or sell them at any time without further notice. This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence.

appreciate the analysis. I do hold a sizeable devon position. This merger is overdue. From my reading one thing that maybe coterra has that devon doesn't is reserve life. Also I hope that the entity will sell the gas play to the likes of eqt/exe and focus on their other basins. we'll see what happens