Deep Value Oilfield Services Opportunity Near the Bottom of the Cycle

I like this North American drilling stock because it has a high free cash flow yield while trading at a fraction of its liquidation value.

Recent strikes on Iran and subsequent retaliatory actions have pushed oil and gas prices higher as tankers have largely stopped transiting the Strait of Hormuz:

Iraq has begun shutting in oil production as its export logistics back up and storage fills, and Qatar has suspended LNG production following strikes on its Ras Laffan facilities; with flows through the Strait constrained, exports from other regional producers are also at heightened risk, putting upward pressure on oil & gas prices.

Higher energy prices directly benefit oil & gas producers, but to increase their production, those producers must hire drilling oilfield service companies, positioning oilfield services as key secondary beneficiaries of a higher price environment.

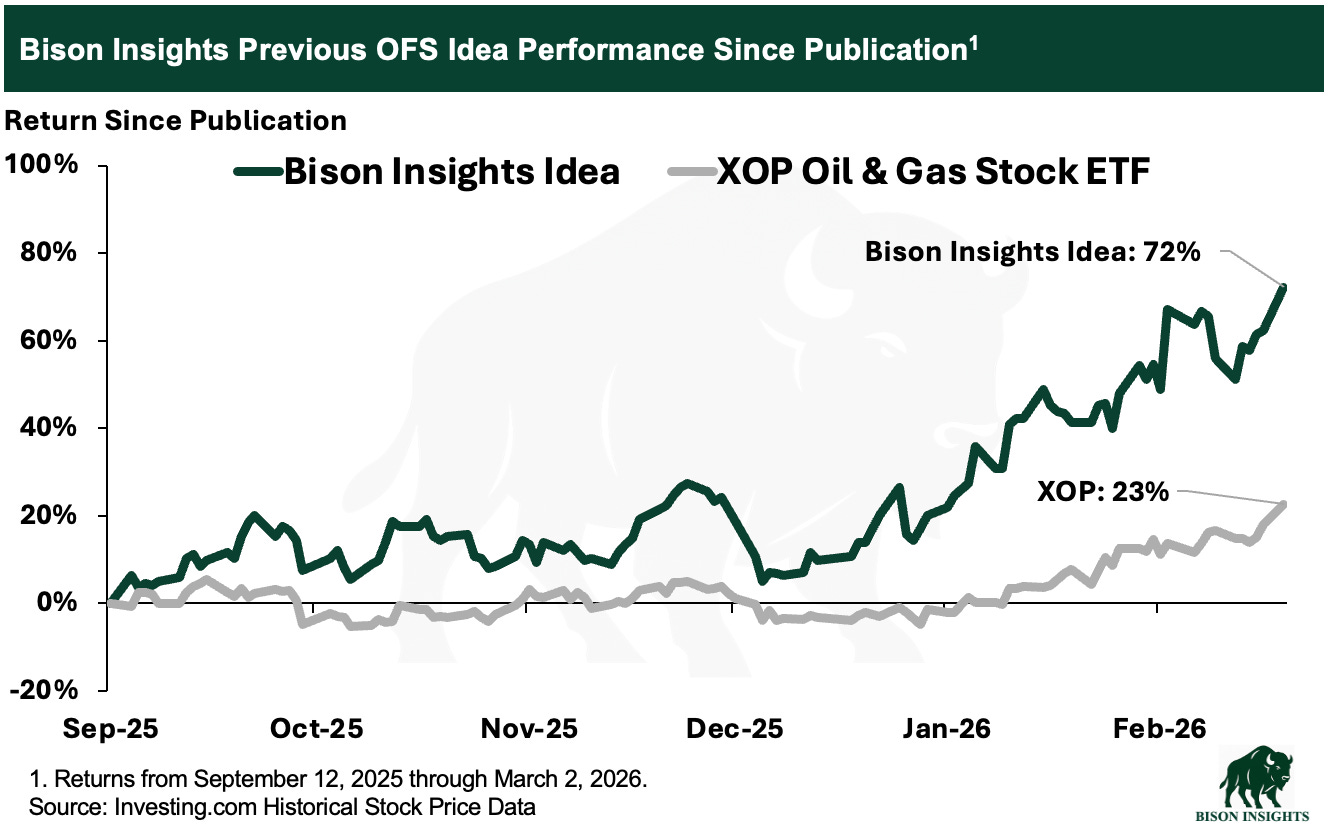

I previously highlighted my first drilling services idea in Cashing In on Gavin Newsom’s Presidential Ambitions – The Biggest Winner from California Energy Policy Moderation. Since publication, that idea has performed well and significantly outpaced the broader energy space as measured by the XOP Oil & Gas Stock ETF:

In this article, I’m highlighting another oilfield services company that I view as offering similar upside and a wide margin of safety.

With several rigs being redeployed into California given the regulatory changes, and into international markets such as Argentina and potentially Venezuela, drilling rig supply is tightening in the broader North American rig market.

Additionally, Cardinal Energy recently announced an equity raise to expand its oil sands operations, supporting at least one active rig and signaling potential for additional work in an area where the company I’m highlighting operates. Cardinal’s stock reacted positively to the announcement, prior to the recent geopolitical events, indicating market demand for E&P growth activity - which requires more drilling.

These developments are nice tailwinds that bolster my core thesis, which is very straightforward: the stock I’m writing about in this article trades at a steep discount to liquidation value while generating substantial free cash flow.

Stocks typically only trade at large discounts to liquidation value when they’re losing cash, are over-levered, or facing permanent structural declines in its end markets.

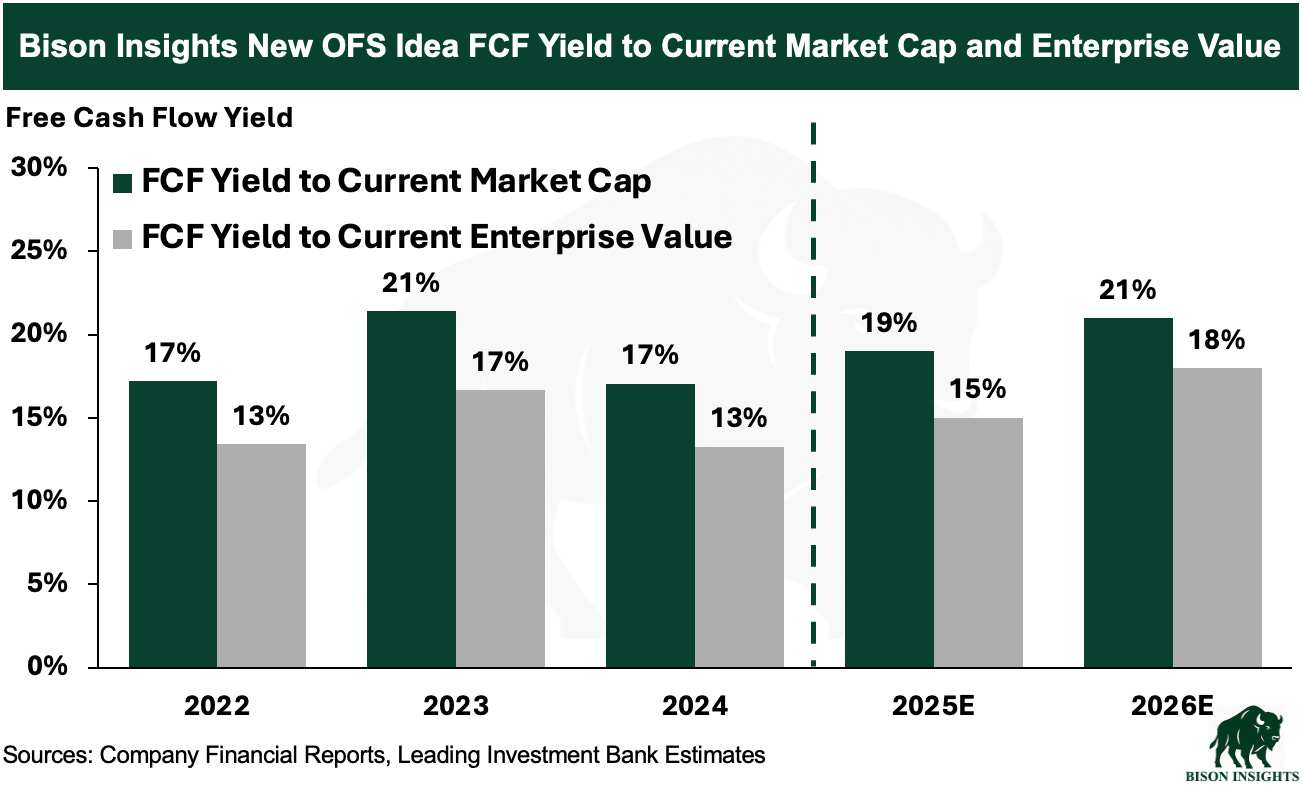

That’s not the case here — in terms of cash flow, this stock has averaged a remarkably steady ~15% free cash flow yield to enterprise value over the past several years (and nearly 20% to market cap), a free cash flow pace that is expected to continue in 2026:

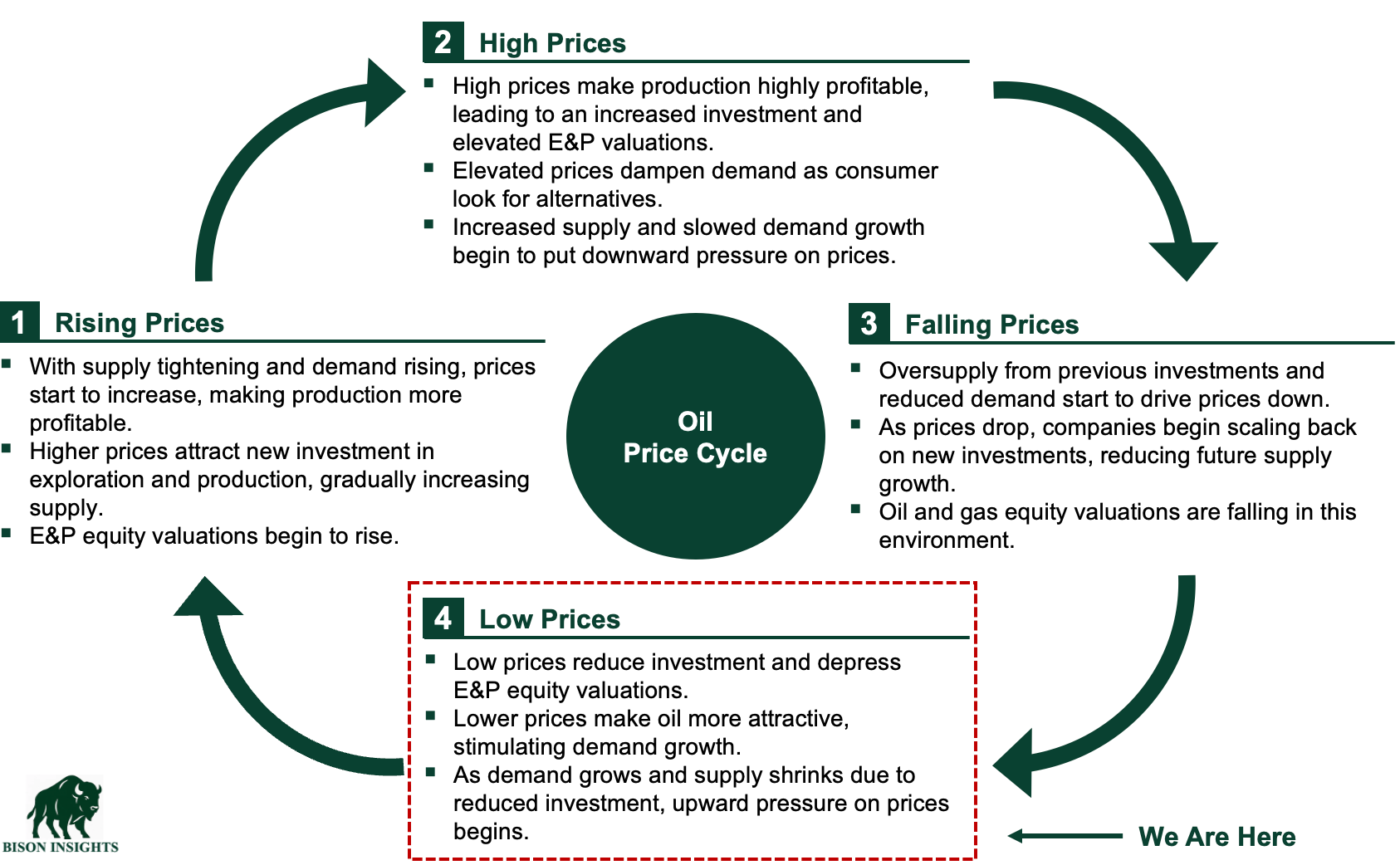

What stands out is that this level of free cash flow has been generated during a downturn in the cycle. Oil prices recently bottomed out at their lowest level in nearly four years, and the U.S. oil rig count has steadily declined alongside them, placing us squarely in the lower portion of the oil price cycle:

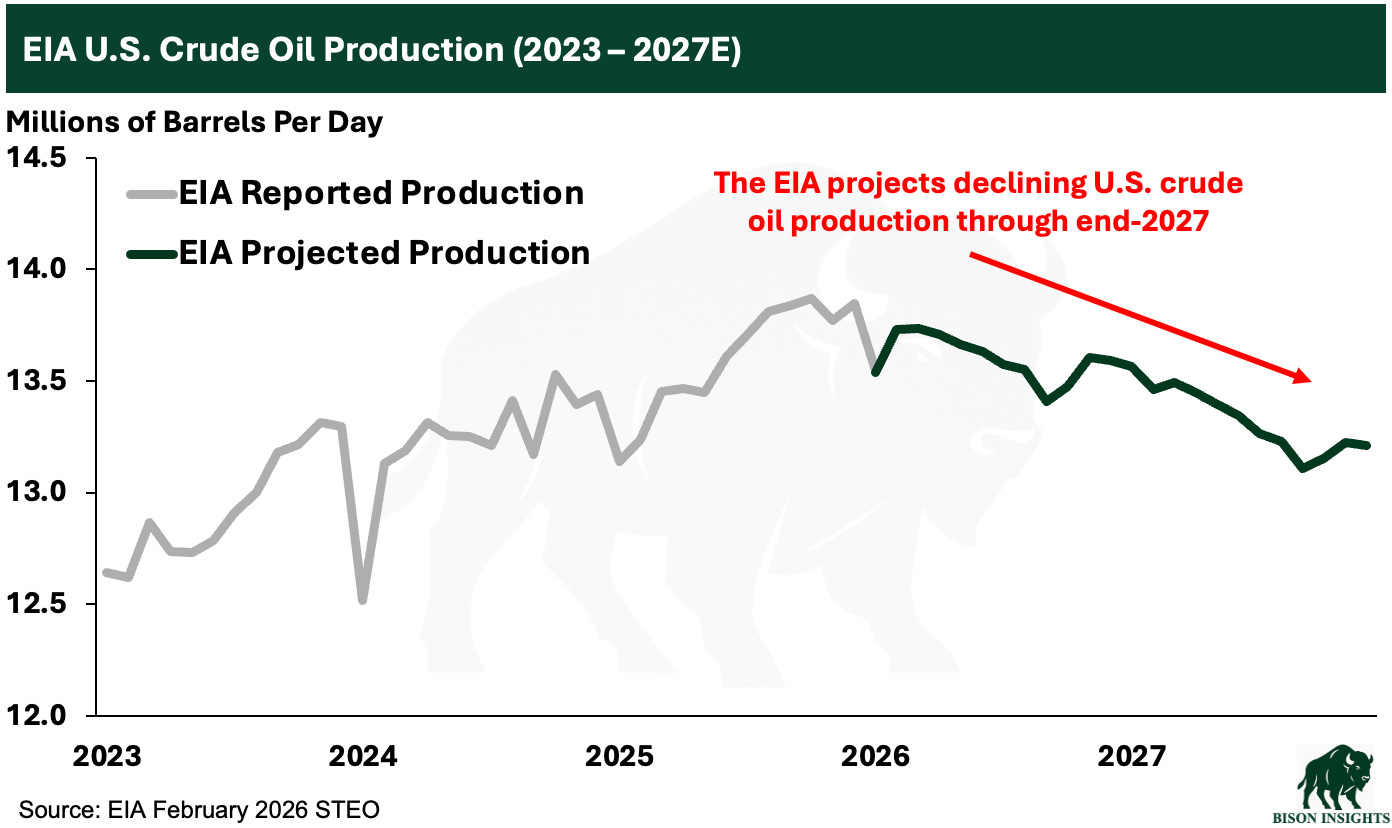

As a result, drilling activity has slowed dramatically, and in conjunction with declining per-foot productivity, the EIA projects that U.S. oil production will decline this year and next:

Declining production tends to lead to higher prices (and war in the Middle East also leads to higher prices), which will lead to producers adding drilling rigs. And because per foot productivity is falling as core inventory depletes, the call on drilling rigs may be much higher than anticipated to maintain or grow production, which would increase the already high free cash flow yield of this company.

While a higher call on drilling rigs would create upside for this stock, what I like about this opportunity is that such an outcome is not required for attractive returns. It’s wonderful that in the base case, the company is already trading at a double-digit free cash flow yield near the bottom of the cycle backed by hard asset value, just as the industry approaches the next upcycle, which perhaps has already begun.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance may not repeat itself.