Drill Baby Drill

Early signs suggest the oil drilling cycle is starting to turn - but the market isn't noticing yet!

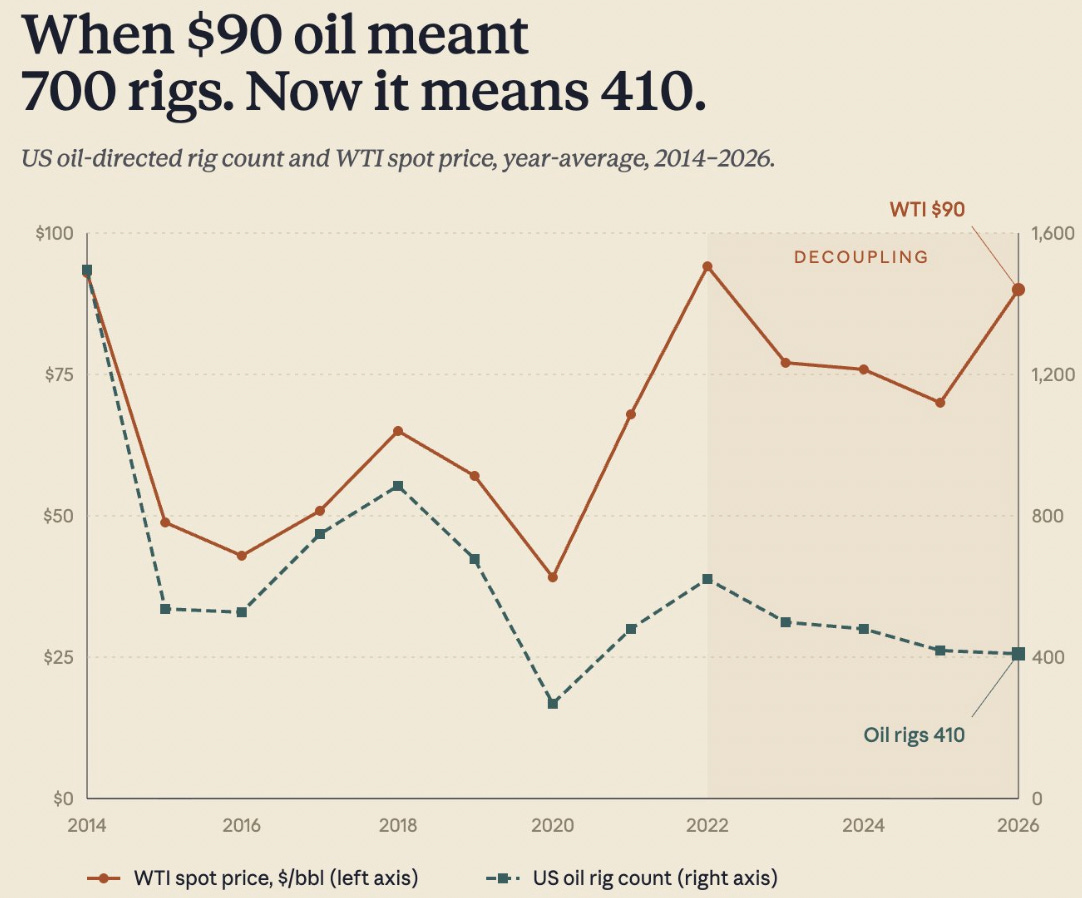

A recent popular article argued that U.S. shale will not respond to higher oil prices the way it did in the past. The article includes a graph titled: “When $90 oil meant 700 rigs. Now it means 410”:

Why does the author think a higher oil price no longer means more rigs?

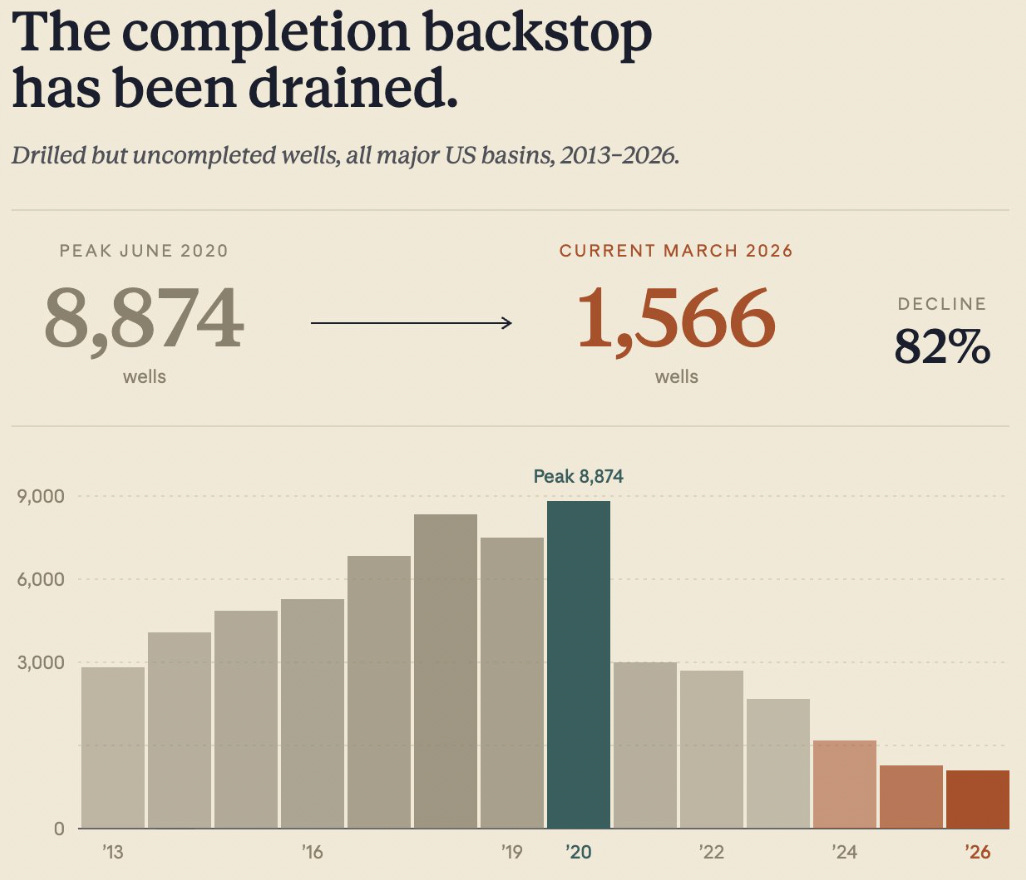

First, he cites low drilled but uncompleted well inventory, or DUCs, across major U.S. basins:

I think this actually cuts against his point. If operators are running low on already-drilled wells, they’ll need to drill more new wells to keep production flat or grow it.

Next, he cites three “breaks” that he argues make this cycle different:

E&P ownership has changed, and shareholders want returns instead of growth.

Core shale inventory quality is degrading.

Oilfield service equipment has been retired.

This all supports more drilling ahead, not less.

First, at $90 oil, well returns are very strong for many operators. Shareholders want returns, and one of the best ways to generate those returns is to drill high-return wells at attractive oil prices. The futures strip is lower than spot, but even at $75+ oil, IRRs are still very compelling across much of the industry.

Second, core inventory degradation means more wells are needed to keep production flat or grow, not fewer. Shale wells decline quickly, so as new wells become less productive, the industry has to drill more wells just to maintain production, let alone increase it.

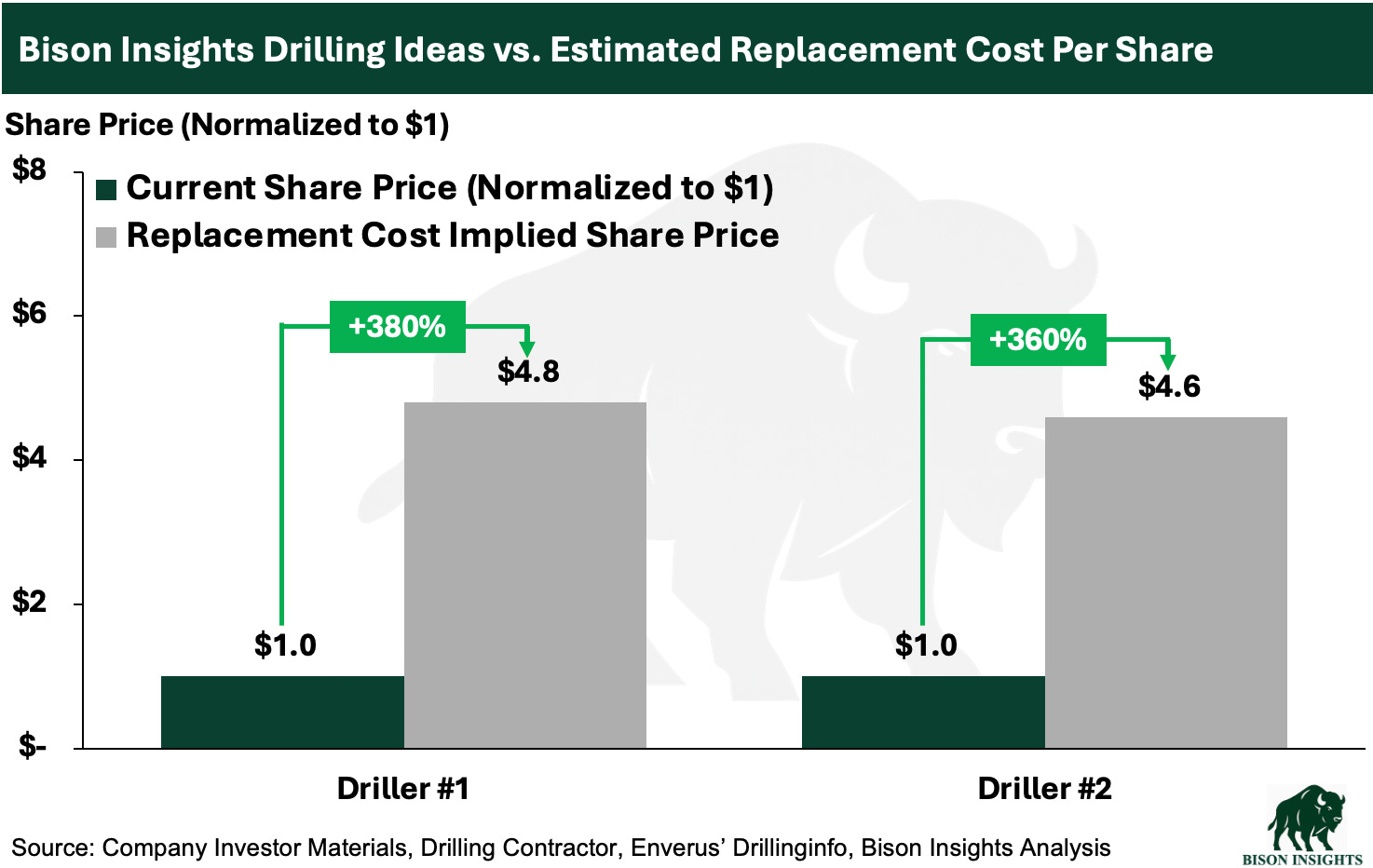

Third, retired oilfield service equipment does not change the fact that E&P companies still need to produce oil. Producers hire OFS companies to drill and complete wells, and if there is not enough capacity to meet demand, then new equipment gets built. That’s why replacement cost is such an important valuation anchor for drilling companies, and why I’ve emphasized it in prior articles. The two Bison Insights drillers I’ve written about still trade far below replacement value estimates:

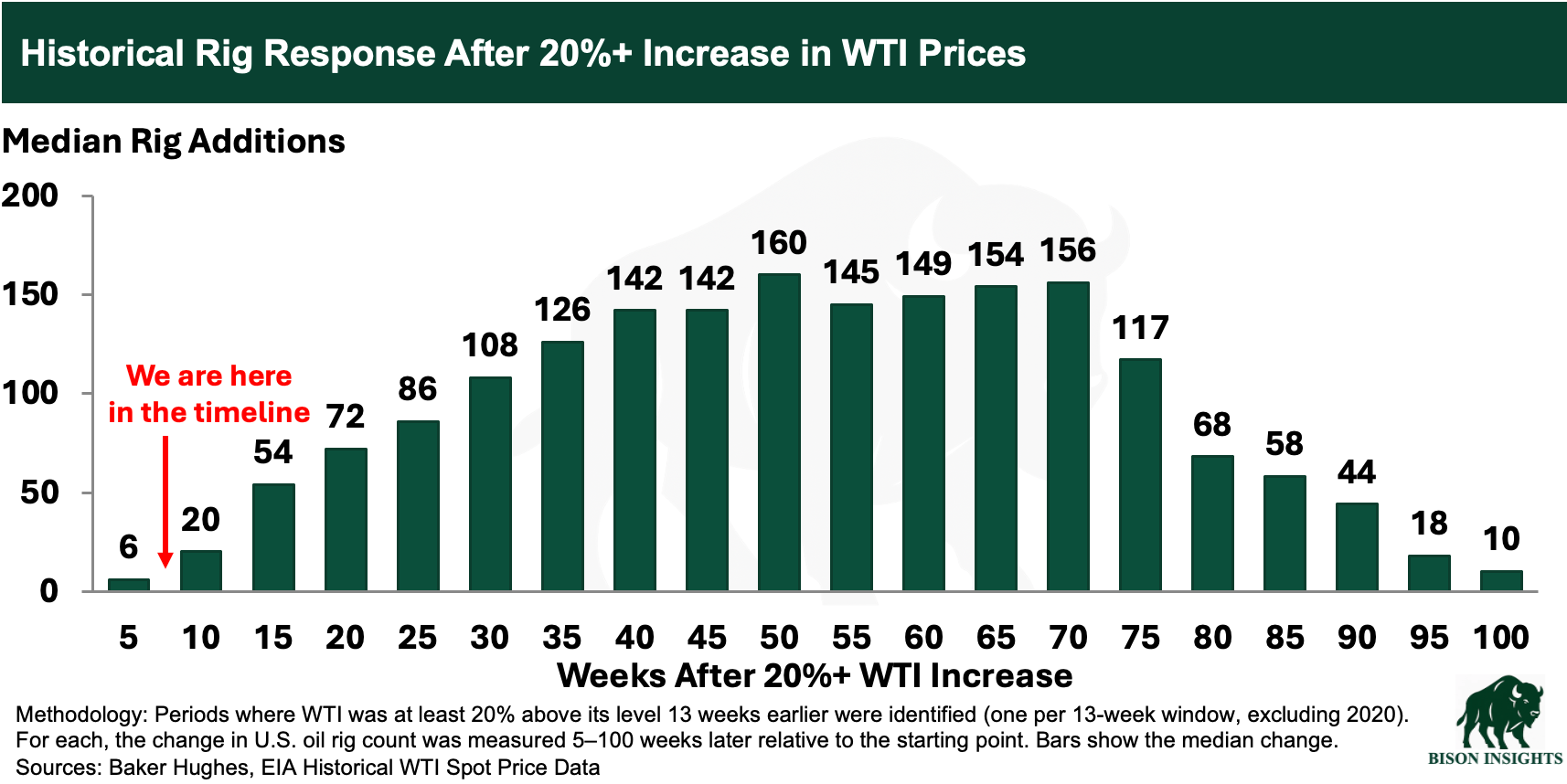

So if higher oil prices will lead to more drilling, why haven’t rig counts moved higher yet?

Because there’s usually a lag. Producers first need to approve budget increases and sign contracts, then OFS companies need to assemble crews and move rigs before activity shows up in the rig count. Historically, rig additions build over time after a move higher in WTI, often not peaking until around 40 weeks later. Today, we’re only roughly 8 weeks removed from the Strait of Hormuz crisis and the move higher in oil prices:

Recent on-the-ground data points support the view that activity is starting to rebound. In a recent Bison Insights interview, the CEO of a drilling company said inbound calls have increased and that he expects utilization to move meaningfully higher by June. A senior contact at an oil and gas private equity firm also recently told me the steel casing market is tightening. Since casing is required to drill new wells, tighter casing supply is an early sign that operators are preparing to drill more.

So yes, the old shale playbook has changed somewhat. U.S. shale is more disciplined and may not respond as quickly as it once did. But slower does not mean no response. And because rigs have been scrapped, the market is tighter, so even a modest increase in activity can move the needle much more for OFS valuations.

That’s why I continue to think the two pure-play drillers I’ve written about on Bison Insights are very compelling here, as are other ancillary beneficiaries. If we’re in the early stages of a multi-year drilling upcycle, I don’t think current valuations come close to reflecting that setup.

Below, I quickly revisit both names, discuss a third potential beneficiary, and share why I still think the market is underestimating their upside.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance is not indicative of future results.