Hidden Iranian Oil Supplies Increase Oil Geopolitical Risk and Upside Potential in Oil Prices

A closer look at Iran’s true oil production, how many barrels are actually at risk, and the promising upside potential in the ideas I’ve shared.

Tensions between the United States and Iran have re-escalated in recent weeks. President Trump has again threatened military action unless Iran makes concessions on its nuclear program and support for regional militant groups, after reports of mass-executions by Iran’s regime despite multiple Trump-imposed “red-lines”.

President Trump has warned that any future strikes would be ‘far worse’ than last June’s attacks. And the U.S. has deployed naval and air assets to the Middle East, including aircraft carrier strike groups. These developments raise the risk that Iranian oil export infrastructure or shipments could be materially disrupted. And at the time of publication, Iran is reportedly warning of a live fire naval exercise next week in the Strait of Hormuz, increasing tensions.

In this context, it’s timely to take a look at how much oil Iran is already supplying to the market to ascertain how many barrels are truly at risk, as estimates amongst data providers vary widely.

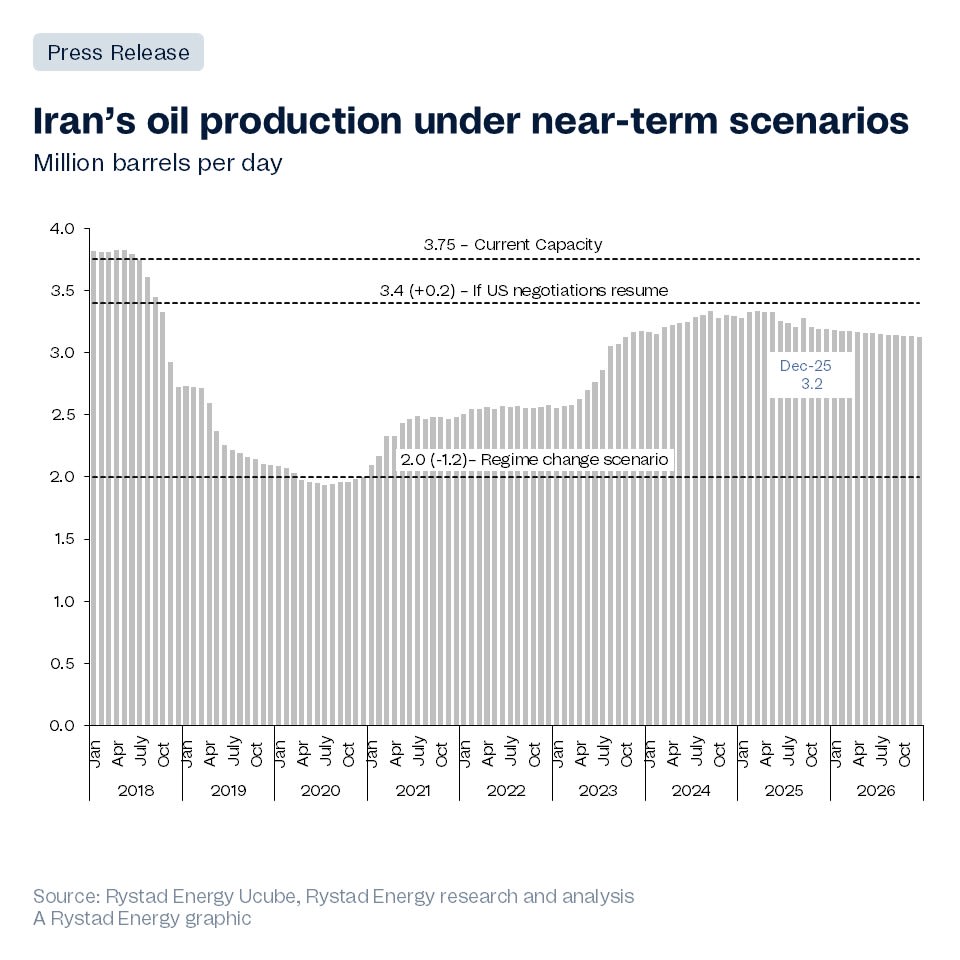

Rystad Energy measures Iranian crude production around 3.2 million barrels per day:

The EIA estimates Iranian production at 3.3 million barrels per day in December, and the IEA is slightly higher at ~3.4 mbd. Meanwhile, Bloomberg and the Energy Institute are materially higher, closer to ~4.2 mbd of crude, and 5.5 million barrels per day total including liquids and NGLs:

Which data provider is closer to the true production number?

Due to the sophistication of Iran’s shadow export network, which relies on ship-to-ship transfers, opaque routing, and other methods to move barrels under the radar (as recently detailed in a fascinating Reuters investigation), accurately estimating Iran’s true production has become increasingly difficult. Bloomberg and the Energy Institute appear to be accounting for more of these shadow barrels, but even their estimates may still be conservative.

If Iran’s oil production is indeed closer to or even higher than the Bloomberg and Energy Institute estimates, as seems likely considering the scale of its shadow export network and reporting from Bloomberg and Reuters, two implications follow:

Iranian production downside risk is much larger than consensus, as it means that more barrels of crude production are at risk than the market currently realizes. Tougher sanctions enforcement from the Trump administration, which significantly reduced Iranian crude exports during his first term, or any direct military disruption to Iran’s export infrastructure or shipping lanes, would remove more barrels than the market is currently pricing in. Even if they are only partially enforced. There is precedent for this, from Trump’s first term:

Sanctions work when they are enforced, illustration:

The upside to Iranian production growth is much smaller than assumed. If Iran is already effectively supplying over 4 million barrel per day of crude (and 5.5 mbd including NGLs), then the claim that Iran represents a large source of incremental future supply is likely overstated. This reduces the risk of a Venezuela-style potential oil supply upside scenario from possible regime change and/or trade normalization.

Against the broader backdrop of non-OPEC production expected to flatten/decline over the next year, and with OPEC unwinding cuts and several members still struggling to meet their stated quotas, spare capacity is thinner than in prior cycles.

We’re entering a period where supply is tightening cyclically, while a larger-than-realized share of global barrels sits in a highly geopolitically exposed region amid rising tensions. This is a classic right-tail scenario for oil prices.

Higher oil prices are ultimately needed to incentivize expensive, long-dated investment in incremental global oil production, which is required to meet growing demand. Some Bison Insights ideas have asymmetric upside exposure to higher oil prices.

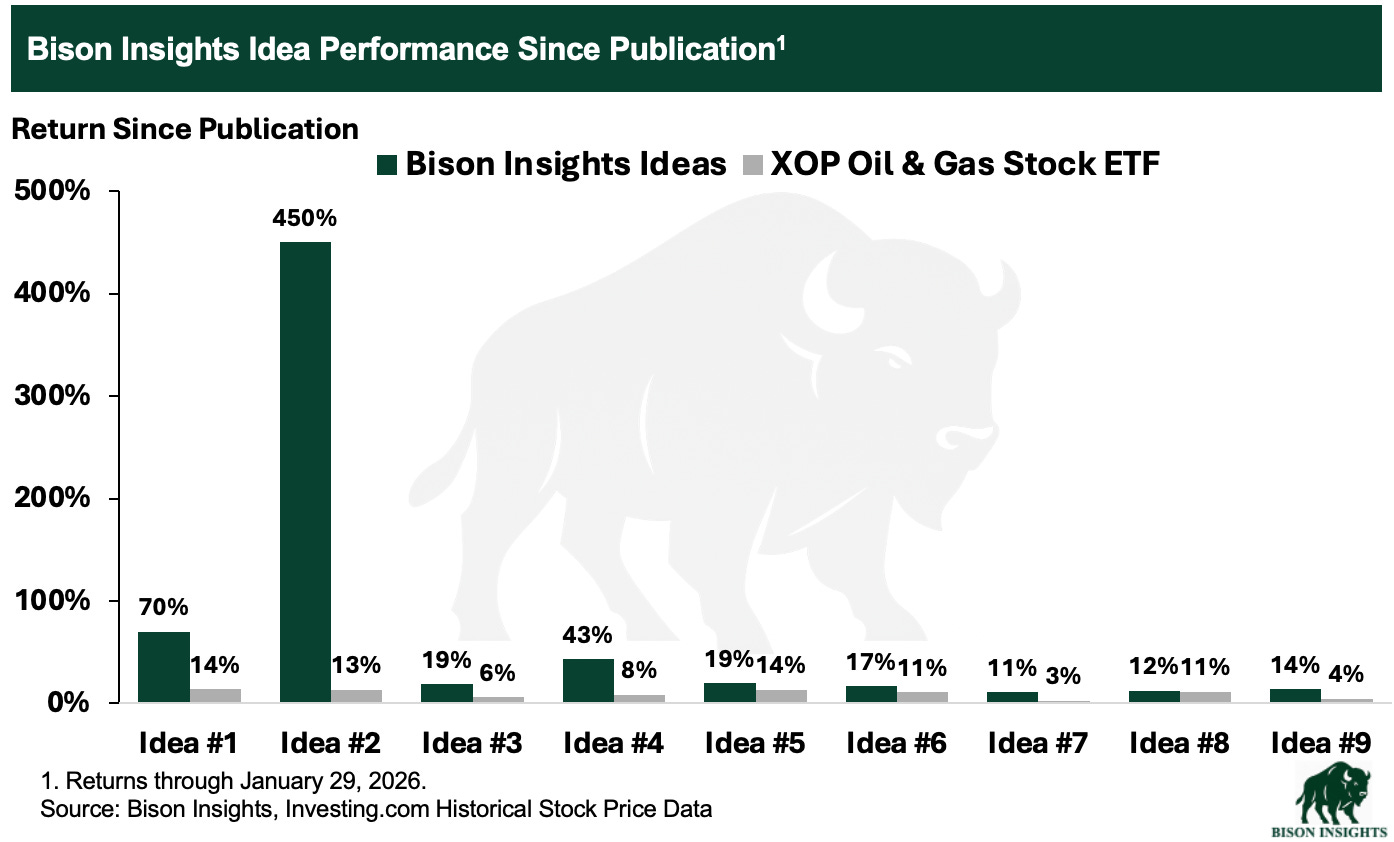

I highlighted this potential in a stock price sensitivity analysis in “Oil Geopolitical Risk, Surprising Positive Oil Fundamental Data, Ideas with High Oil Price Upside,” - while detailing these companies’ deep margins of safety. These oil upside-levered ideas, including my latest idea, are already outperforming the broader energy and market indexes as oil prices have risen.

Chart of all Bison Insights’ idea performance since publication, vs XOP energy ETF:

With rising tensions around Iran and stronger than consensus oil balances due to rapid demand growth and challenged supplies, this right-tail geopolitical risk could send oil prices soaring, as the longer-term fundamental oil bull market scenario unfolds.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation, and should not be relied upon. Please consult an advisor and do your own diligence. Past performance may not be indicative.