I'm Bullish Oilfield Services, But I'm Passing on This Levered OFS Stock

This stock could work if the cycle gets very strong, but I think the risk/reward is much worse than the OFS stock ideas I've shared here on Bison Insights.

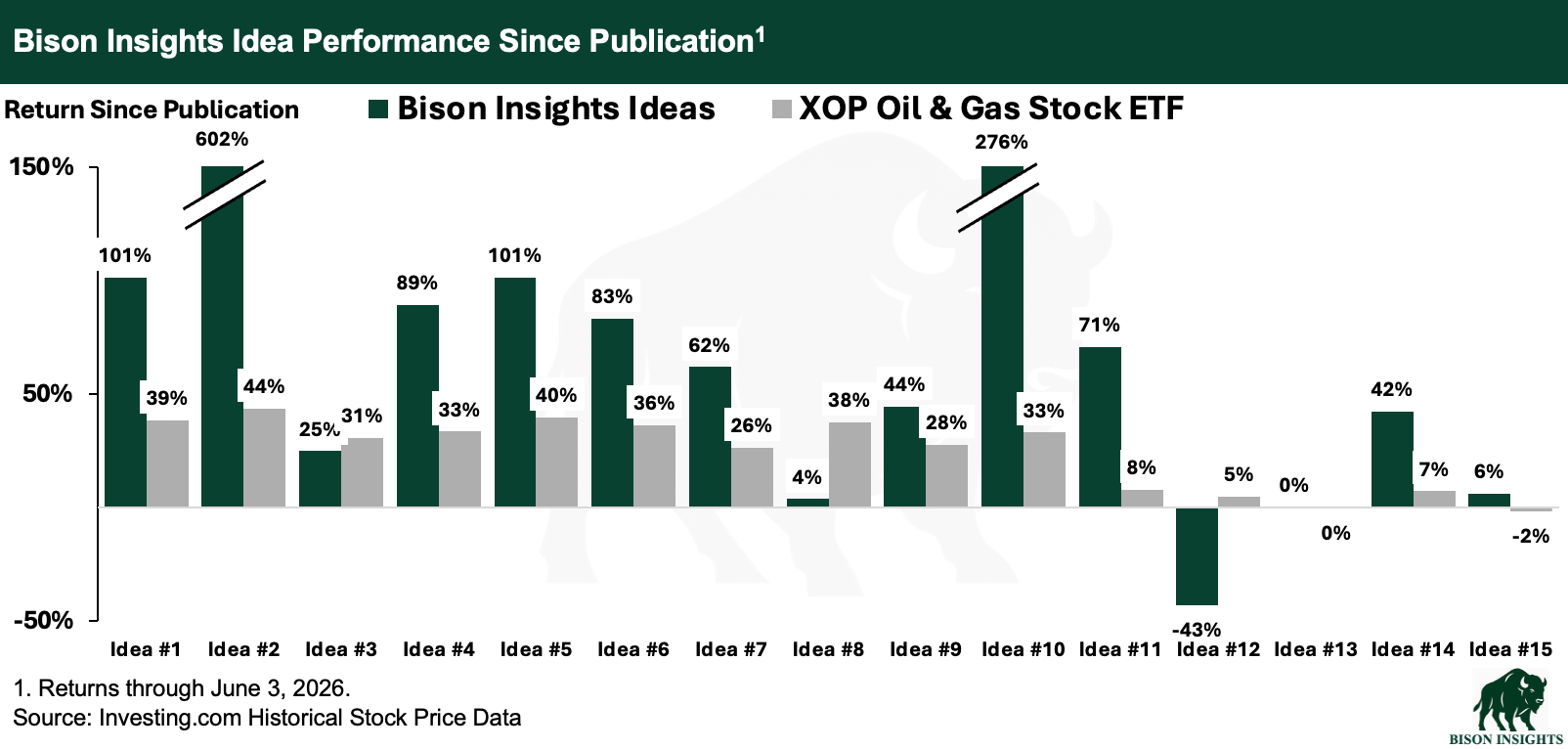

So far on Bison Insights, I’ve written extensively about specific oil and gas company stocks and related securities that I own and like. These have mostly performed very well since publication:

In this article, I’m writing about a stock that I don’t like.

The stock is of an oilfield services company (OFS), and if you’ve been following my writing here on Bison Insights, you know I’m very bullish on the OFS sector right now for two primary reasons.

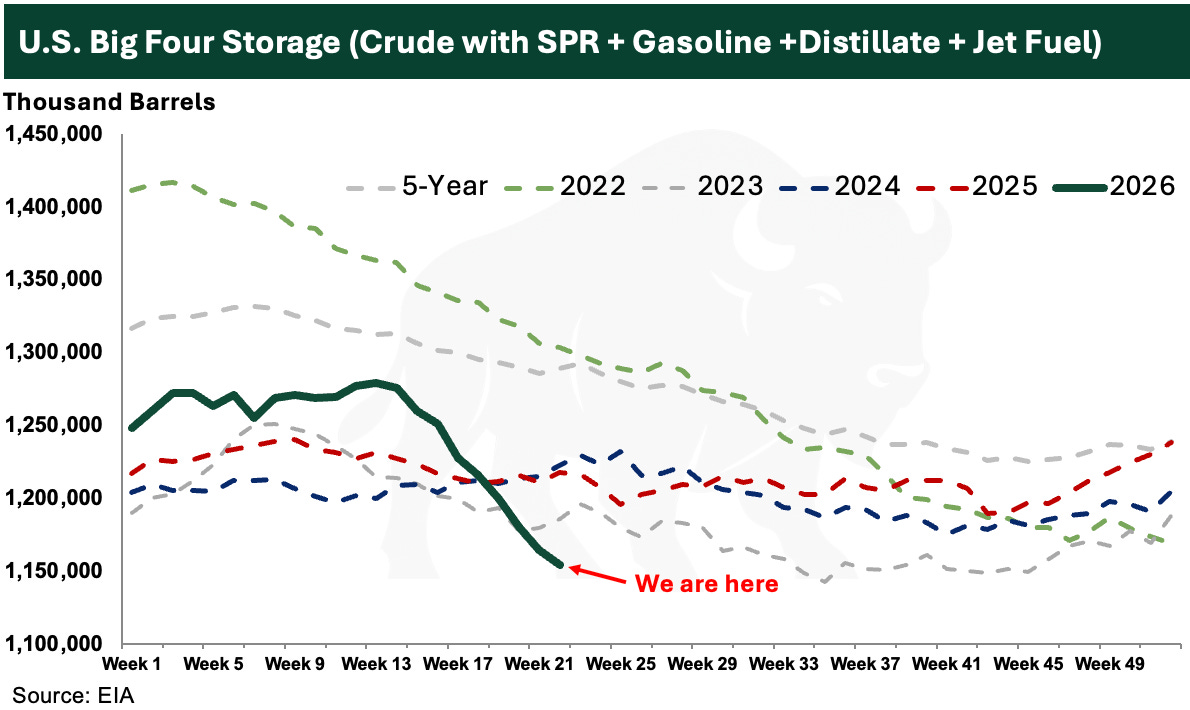

First, we’re in the midst of the largest oil supply disruption in history, and it remains unclear when the disruption will end. Meanwhile, U.S. oil inventories are drawing at a record pace. They are expected to reach all-time lows within the next two weeks:

Oil is essential to the global economy, so those missing barrels will need to be replaced. To replace them, producers will need to drill more wells, which means more work - and profits - for oilfield services companies.

Second, the OFS sector has consolidated tremendously over the last decade. When oil prices crashed in late 2014, and then again in 2020, there were a lot of bankruptcies and consolidation in the sector which has significantly reduced the number of competitors, particularly in the onshore drilling space:

The companies that survived are competing in a much less crowded market. As a result, we’ve already seen resilient pricing and margins, despite a decline in the rig count over the past few years. Continuing this trend, I think that OFS margins and free cash flow will increase far more than the market expects as the cycle turns.

Considering these factors, I think the outlook for OFS looks very bright - but not every OFS company is equally attractive. In this article, I’ll walk through one specific OFS company stock that I don’t like, explain why I’m passing on it, and compare it to several OFS companies I’ve written about that I believe offer a much better risk-reward profile.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance is not indicative of future results.