Immediate Upside And Long Term Growth Potential, With Decades Of Oil Reserves

Major business inflection, multi-decade reserves, and a widening valuation gap offer both immediate upside and long-term compounding potential.

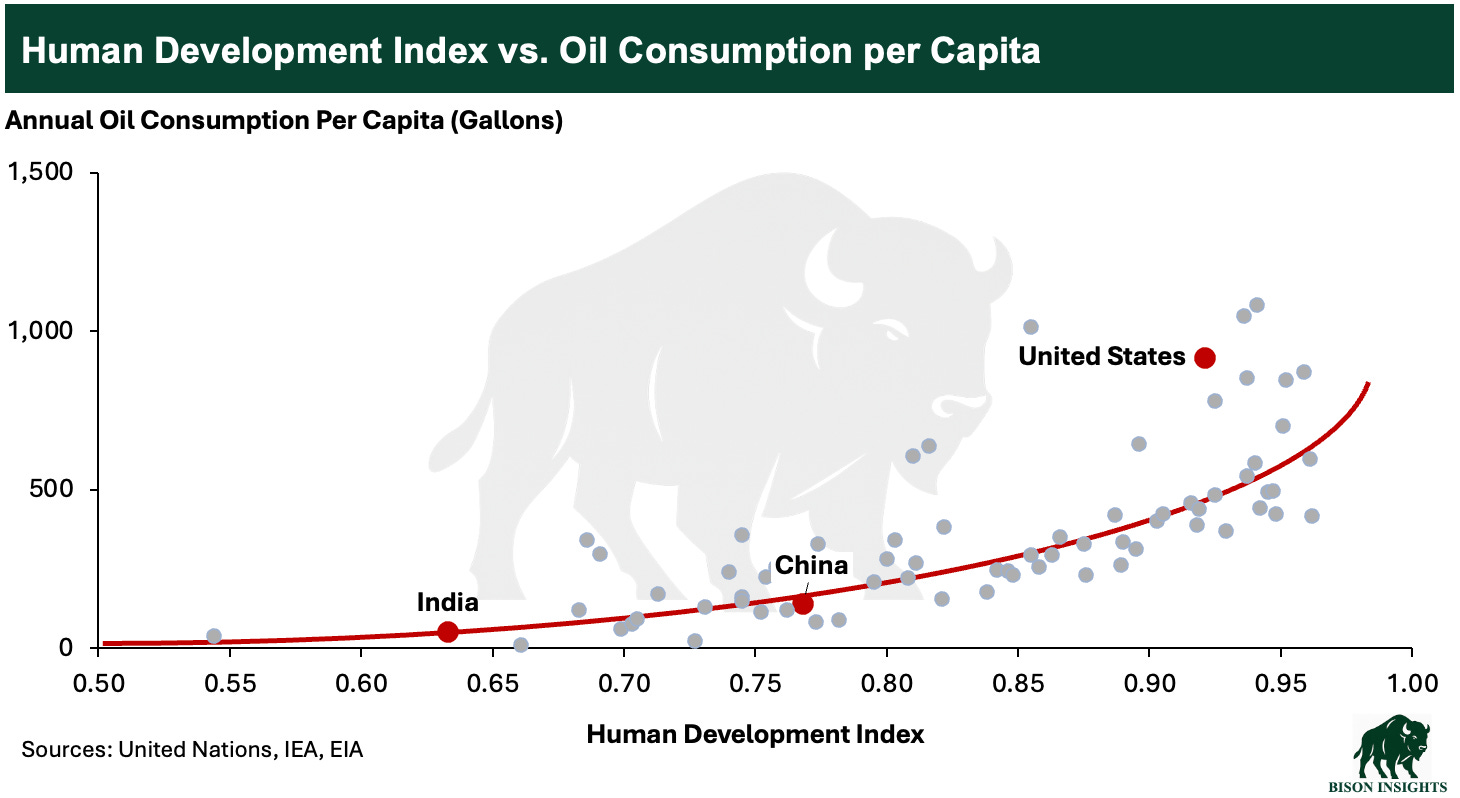

Major oil research organizations — most notably the IEA — are finally beginning to acknowledge that global oil demand is unlikely to plateau anytime soon. Most of the world’s population lives in developing or underdeveloped economies, and as these economies grow, their energy use rises with them. Oil demand, in particular, increases almost mechanically as standards of living improve. In my view, the world still has massive untapped demand growth ahead:

As an investor, the next logical question is how best to gain exposure to this long-term structural oil demand growth.

One answer is to own shares in a company with large, long-duration reserves. As global supply becomes harder and more expensive to add, oil prices must rise to incentivize new production. Companies that already control decades of low-decline resource don’t need to spend heavily to find more oil. They are positioned to harvest the bulk of the likely future price increase as pure profit.

The market has begun to recognize this dynamic and has begun to reflect the embedded value in the segment of the industry with exceptionally long reserve life — Canada’s oil sands producers. These companies often have 20 to 50 years of remaining resources, and they have substantially outperformed the broader energy sector, as measured by the XOP ETF, year-to-date:

The company I’m writing about in this article sits firmly within this group. It produces large volumes of oil and has more than 30 years of reserves at its current production rate, providing long-term exposure to oil prices and a significant margin of safety, but its stock price and valuation still lag its closest peers.

Closing this valuation gap implies substantial upside, driven by three factors that I think could also move the company toward a premium multiple, which I outline below.