Large Position Review: Undervalued Oil Producer Buying Back Stock and Paying Off Debt

The second in a series of in-depth updates on my favorite oil stock ideas.

This is the second article in a series covering my favorite oil stock ideas that are among my largest positions. These are the ideas I think can do well even if oil prices decline, while offering multi-bagger upside potential if oil prices go higher.

As an investor, I think that having this asymmetric potential is crucial for my large positions in this time of elevated uncertainty surrounding future oil prices. WTI oil has sold off sharply this morning after the U.S. and Iran agreed to an MOU that includes a reopening of the Strait of Hormuz.

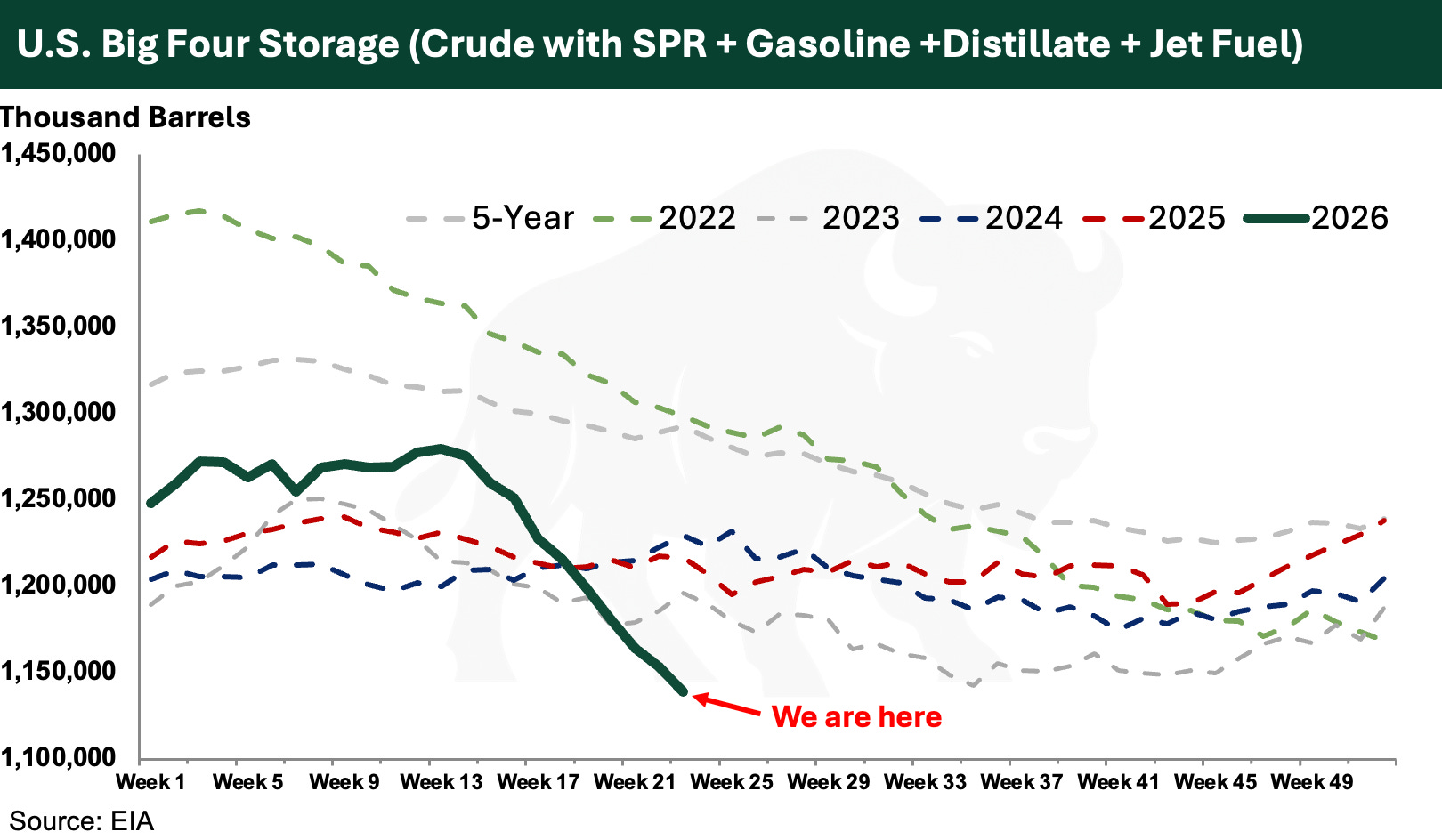

The strong bearish narrative is that once the Strait of Hormuz reopens, shut-in barrels will quickly return and tip the oil market into surplus. On the other hand, traffic through the Strait remains heavily constrained and it’s unclear whether the MOU will actually be signed on Friday. Even if it is signed - or perhaps it was already signed, as some reports indicate, it is unclear how long it will take shipowners and insurers to feel comfortable transiting the Strait again considering the risk of mines, ongoing conflict in the region, and Iran’s idea of charging fees or service charges to transit the Strait. Meanwhile, inventories continue to draw quickly and are already very low:

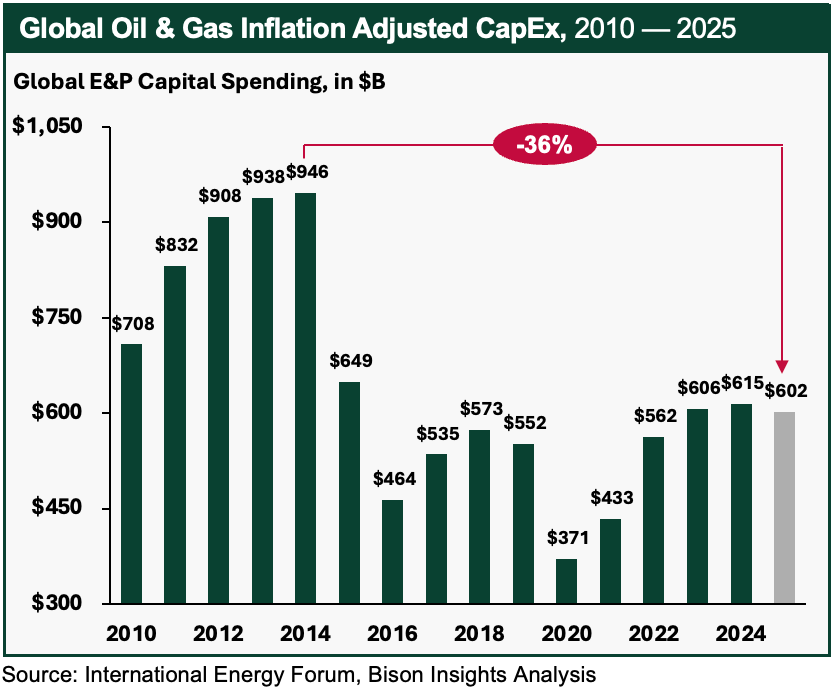

These low, declining inventories may accelerate and exacerbate the cyclical bull market for oil, similar to the energy crises of the 1970s. My oil bull thesis has never been that the Strait of Hormuz would stay closed forever. My view is that insufficient exploration and delineation over the past ~12 years, alongside growing demand, have set up a cyclical increase in oil prices and drilling activity. That thesis has not changed, and the spending and drilling activity necessary to bring a new wave of global oil production has not yet arrived.

Still, short-term narratives can be very powerful, and can suppress prices. So in the face of this uncertainty and likely short-term volatility, I’m focusing on the ideas that I think offer the best combination of upside in both a lower and higher oil price environment.

For example, in this article, I’m discussing a company whose stock trades at a steep discount to reserve value in a lower oil price environment, with very high potential upside in a higher oil price environment:

This is a smaller company with legacy governance issues, which is likely why the market appears to be overlooking and undervaluing it.

The market seems to have missed that this company has demonstrated a successful turnaround over the last few years. It has executed disciplined capital allocation: debt repayment, share repurchases, and highly accretive tuck-in acquisitions.

Now, the company is pursuing an exciting, relatively new oil development approach, with high returns on invested capital. The market does not appear to have caught on to this - for now.

This is the second article in this stock idea update series and is an in-depth update on the company I originally wrote about back in April in This Undervalued Oil Producer is Buying Back Stock and Paying Off Debt.

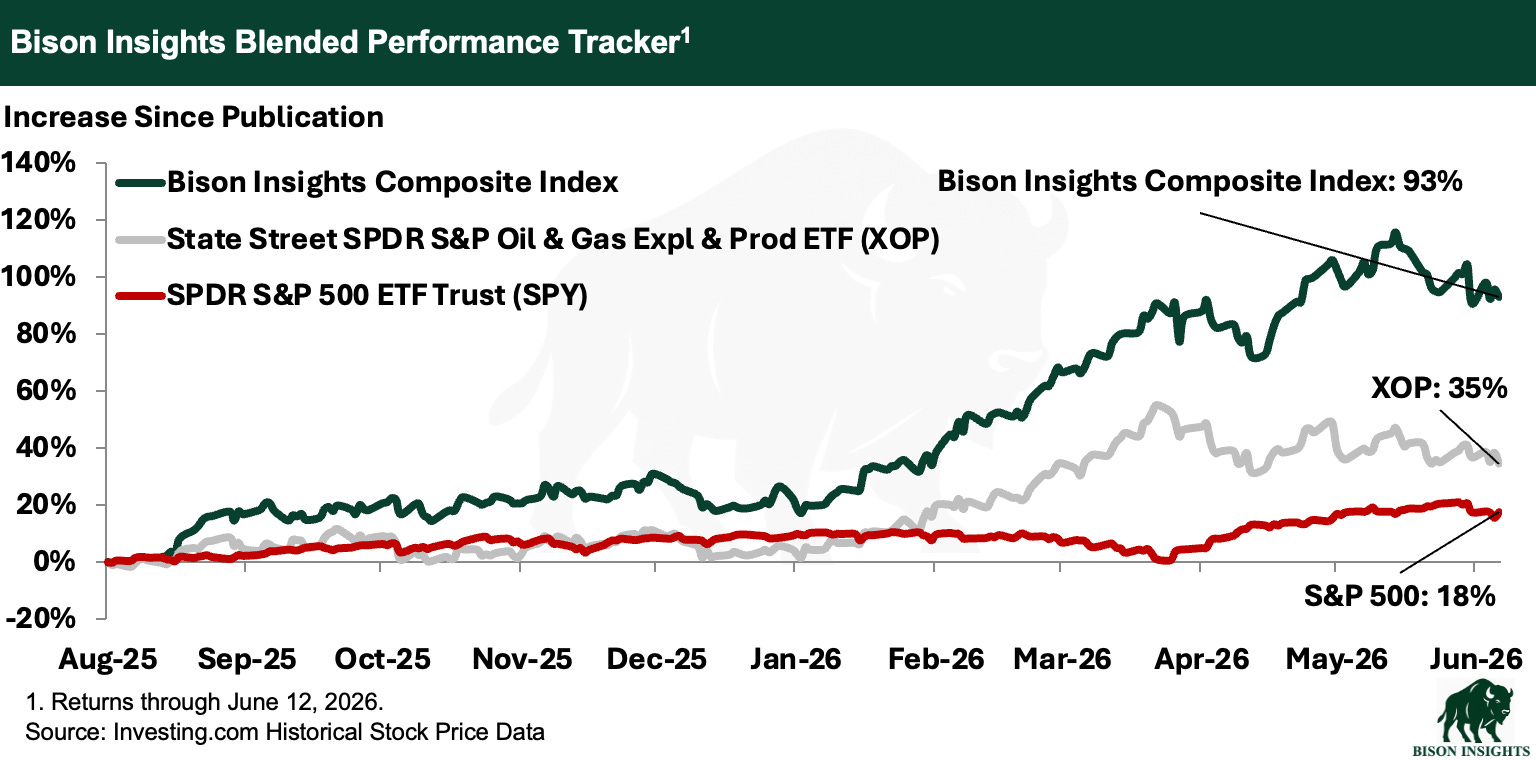

These stocks represent a large portion of the Bison Insights composite tracker, which has been crushing oil stock ETFs like State Street SPDR S&P Oil & Gas Expl & Prod ETF (XOP) and broader market ETFs like State Street SPDR S&P 500 ETF Trust (SPY):

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance is not indicative of future results.