Natural Gas Producer With A 10%+ Dividend Yield - Simplified Business, More Cash, Plenty of Upside

After a recent divestiture, this U.S. natural gas producer now delivers more natural gas per dollar of valuation than the big ones, while also paying a dividend yield of over 10%.

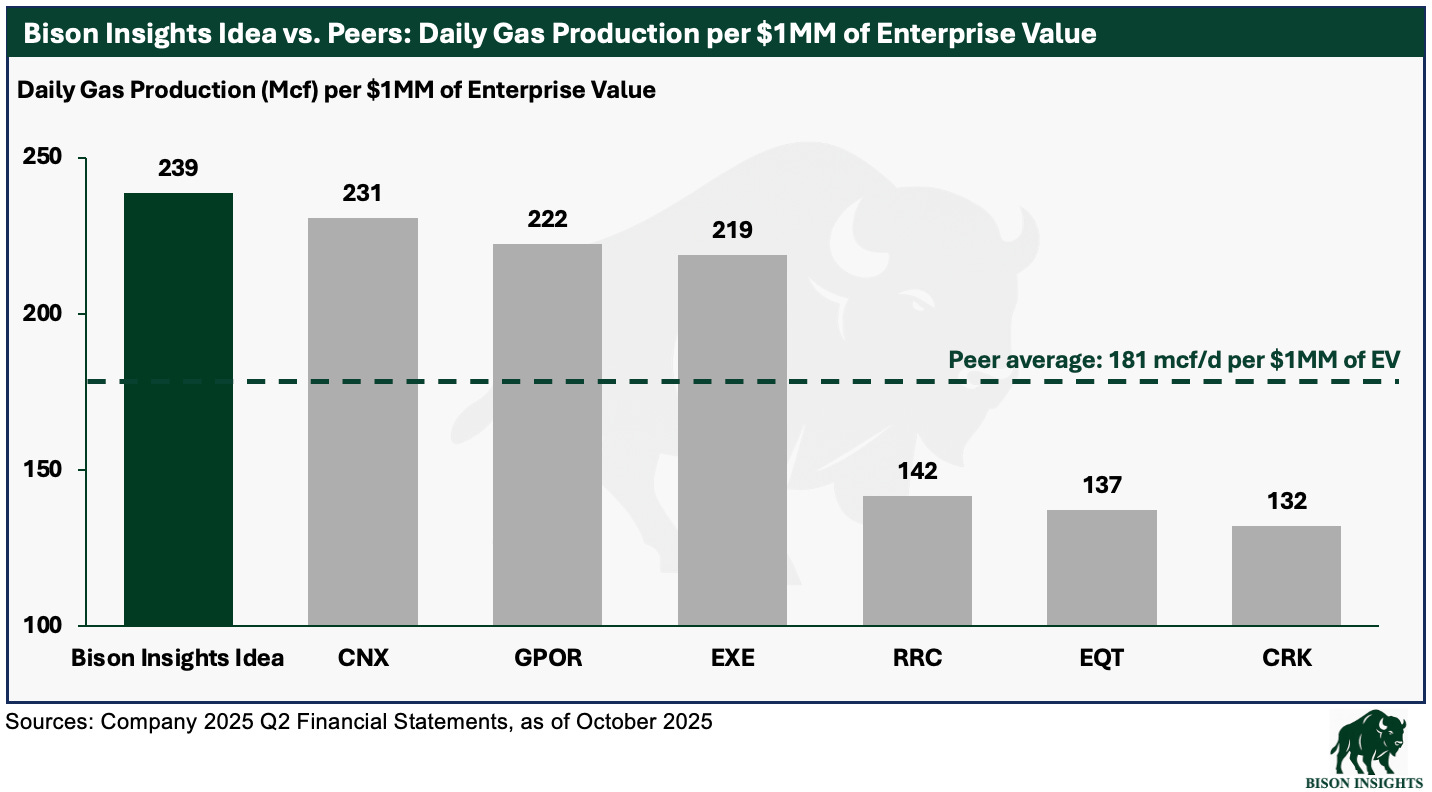

After a recent large divestiture, the company I wrote about in Undervalued Small Natural Gas Producer With a 10%+ Dividend Yield has greatly simplified its business. On an enterprise value basis, it now produces more natural gas per dollar of valuation than the big natural gas companies.

But this chart doesn’t tell the full story - natural gas is only half of this company’s output, with the rest being oil and NGLs. That means investors get more exposure to gas than these larger gas names, while also getting substantial oil and NGL production essentially for free.

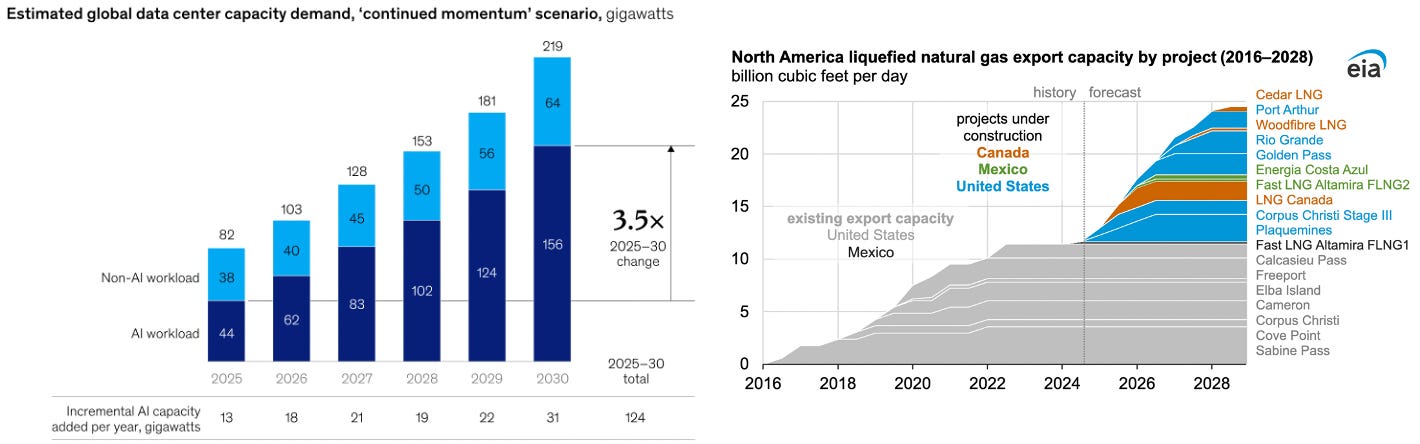

This gas leverage is especially compelling because natural gas demand is expected to climb sharply as AI data centers expand and LNG export capacity grows.

For this company, the combination of high leverage to gas prices, substantial oil production, and a large acreage position that has been increasing in value provide material potential upside from here.

Oh, and on top of that, the stock currently yields a dividend of over 10%, covered several times over by the net cash on the balance sheet and also covered by run-rate free cash flow.

My full walkthrough is below.