Natural Gas: What You Don't Know Can Hurt You

Disclaimer: For informational purposes only. This is not an offer, solicitation or investment recommendation. Please consult an advisor and do your own diligence. Do not rely.

Bison Insights is where award-winning energy investor Josh Young and his team are sharing high-upside potential investment ideas he’s most excited about. In the first several features, we’ll be focusing on natural gas.

The consensus view on natural gas is now well established: structural demand is likely to significantly increase over the next several years, driven by the boom in AI data centers and the rapid expansion of U.S. LNG export facilities. Many analysts believe these factors will underpin a bull market in gas despite steady production growth from U.S. producers.

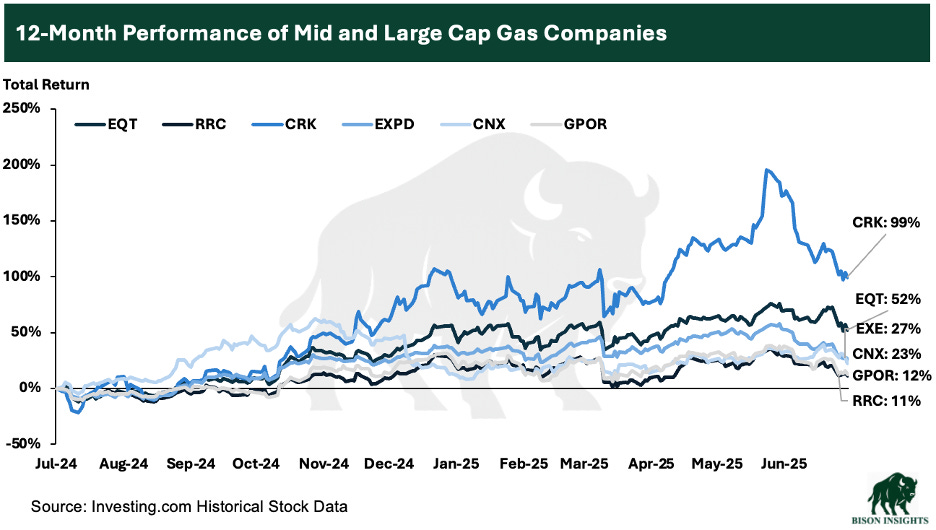

Mid- to large-cap gas producers have performed exceptionally well over the past year, as the market has priced-in higher future gas prices. As a result, these stocks now offer less upside if the thesis plays out, and greater downside risk if it does not.

Josh’s Variant View

Josh agrees that LNG expansion and AI demand are major factors, but he believes the market is underestimating how quickly these LNG facilities will ramp. He first highlighted this in January (you can read here), and so far it’s playing out: Plaquemines Phase 2 is already producing LNG and Golden Pass Train 1 is taking feed gas, both well ahead of the EIA’s October 2025 and May 2026 estimates.

Josh and his team have identified a third factor that the market appears to be missing when it comes to gas markets. This third factor is critical in understanding the North American natural gas market going forward. And it is actionable because Josh has uncovered several very cheap gas-weighted equities that he sees as mispriced today, each of which we’ll discuss in future issues of Bison Insights.

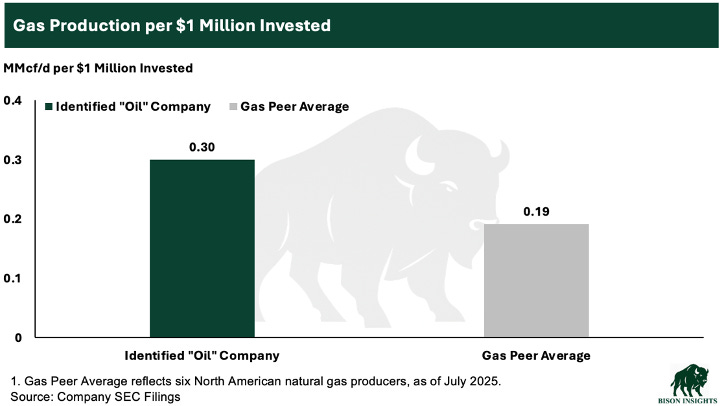

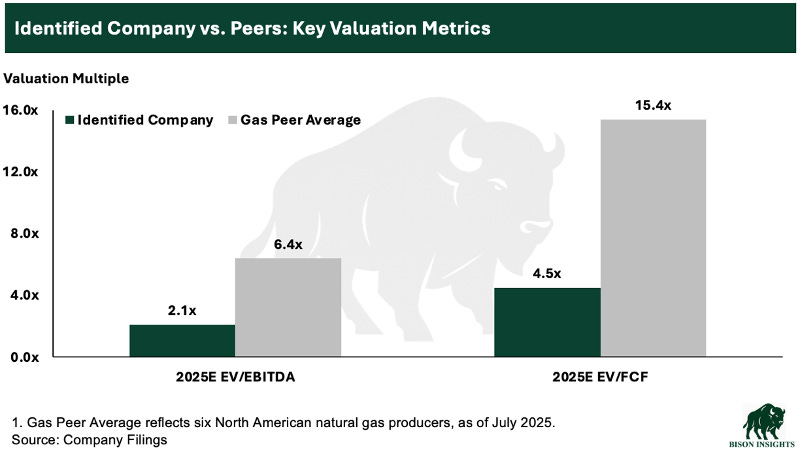

One example is a company typically classified as an oil producer, because over half of its BOE output comes from oil. Yet it generates so much associated gas that, on a per-dollar basis, it offers investors more natural gas production than many pure-play gas names.

Another name Josh has identified is a primarily gas-weighted producer with significant institutional ownership and limited trading volume. Its low visibility makes it a classic “value investment” candidate, as it’s a fundamentally strong company that appears to have been overlooked or misunderstood by the broader market.

Premium subscribers can read the full gas market analysis below, including this third critical factor: