The IEA Capitulates: Less Bearish Oil, But Still Too Pessimistic

Promising for oil drilling and producing companies

Since its founding in the 1970s, the International Energy Agency (IEA) has evolved from an institution created to safeguard oil security into one increasingly focused on promoting renewable energy and emissions reduction. That shift in emphasis has coincided with consistently conservative outlooks on long-term oil demand, and critics have noted that its scenarios appear more aspirational than descriptive, aligning with policy goals rather than market trends.

Against this backdrop, it is striking that the IEA now highlights how sharply oil supply would fall without sustained, large-scale upstream investment in their recent report titled The Implications of Oil and Gas Field Decline Rates.

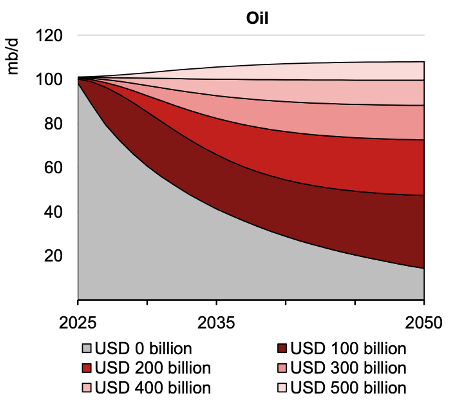

According to the IEA’s estimates, it takes nearly $500 billion a year in upstream capital just to hold global output roughly flat. They note that the capital investment requirement is expected to rise as unconventional production, with its steeper decline rates, makes up a larger share of supply, and as new conventional discoveries become increasingly scarce.

What’s striking is that $500 billion is the IEA’s highest investment case, and even then, oil production merely plateaus through 2050. Why so low? Because the IEA demand scenarios assume oil use stalls out and then goes into decline.

But what if that view is wrong? What if demand keeps expanding in line with the trend of the past century? If past is prologue, the capital call on oil is far greater than the IEA estimates, and the implications for supply, price, and energy equities are significant.