This Undervalued Oil Producer is Buying Back Stock and Paying Off Debt

"Heads I win, tails I win less?" Amid historic oil price volatility, this oil stock could soar.

On Friday, an Iranian official said the Strait of Hormuz was open on social media. Trump amplified the claim, sending oil and related equities sharply lower. By Saturday, though, Tehran tightened control again, ships were turning back, and some vessels reportedly came under fire, leaving the Strait effectively closed once more and sending oil prices and equities back up to begin weekly trading.

This extreme volatility is essentially the story of the oil market over the last seven weeks: conflicting headlines from both sides of the conflict, with oil prices and related equities swinging wildly in both directions.

Oil market gallows humor, Strait of Hormuz edition, from X:

I’m not a military expert, I’m not a political guru, and I can’t accurately predict short-term oil prices. But I am an expert in evaluating and investing in oil & gas stocks. In the middle of this volatility, there is one oil producer that is particularly compelling. It could be a grand slam in the current price environment, while having valuation upside even at $70 oil.

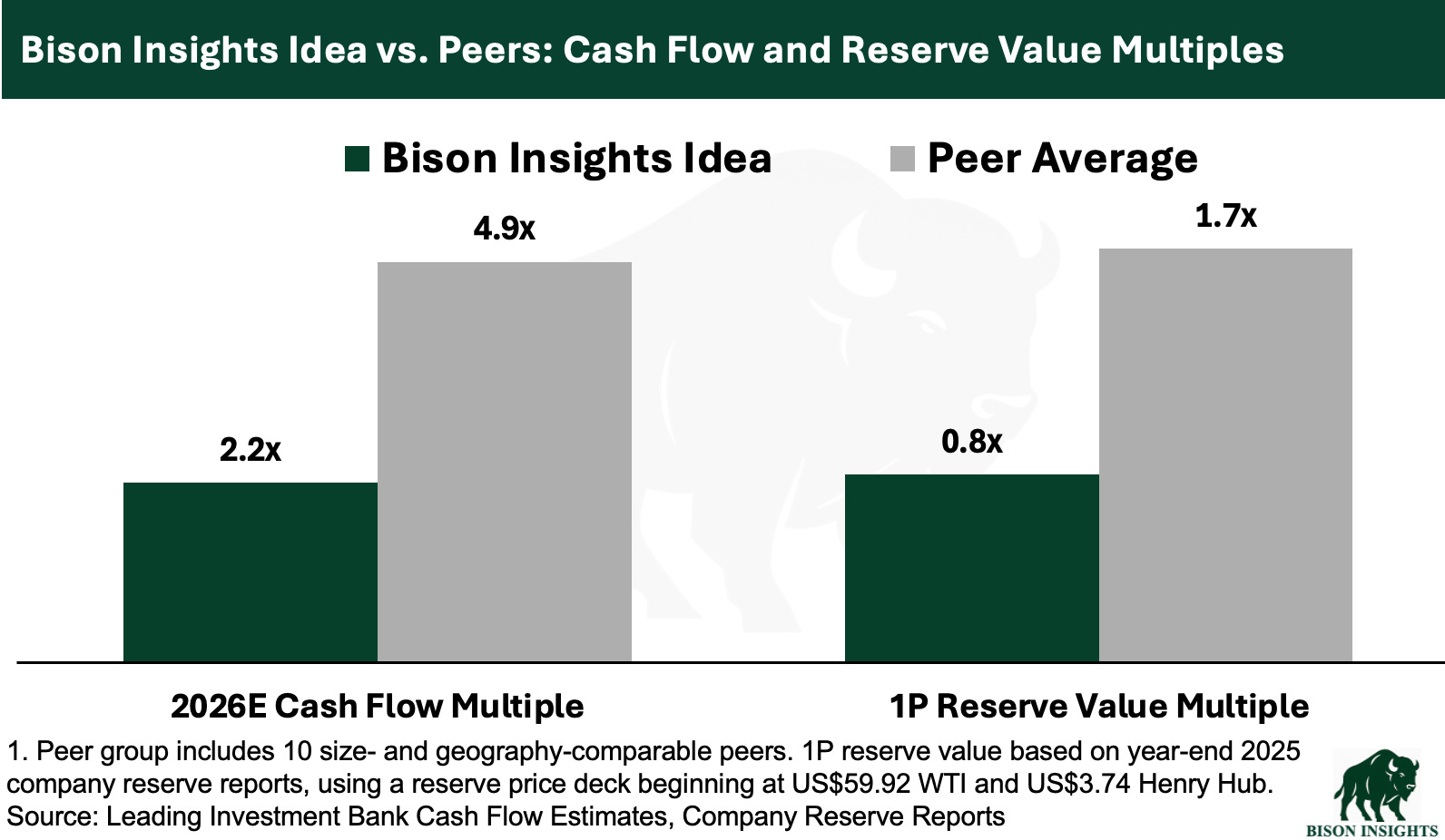

My thesis is straightforward: despite steady progress in an operational and financial turnaround, the market still does not fully appreciate these improvements. The company trades at a steep discount to peers on both cash flow and reserve value:

This undervaluation has persisted even after the company recently posted another very strong quarter, leading one leading investment bank analyst to comment:

“Overall, this is a solid quarter for them… We believe that posting better-than-expected quarters will start to earn more confidence in the story from the market and be a key factor in driving down the valuation discount relative to mid-sized peers.”

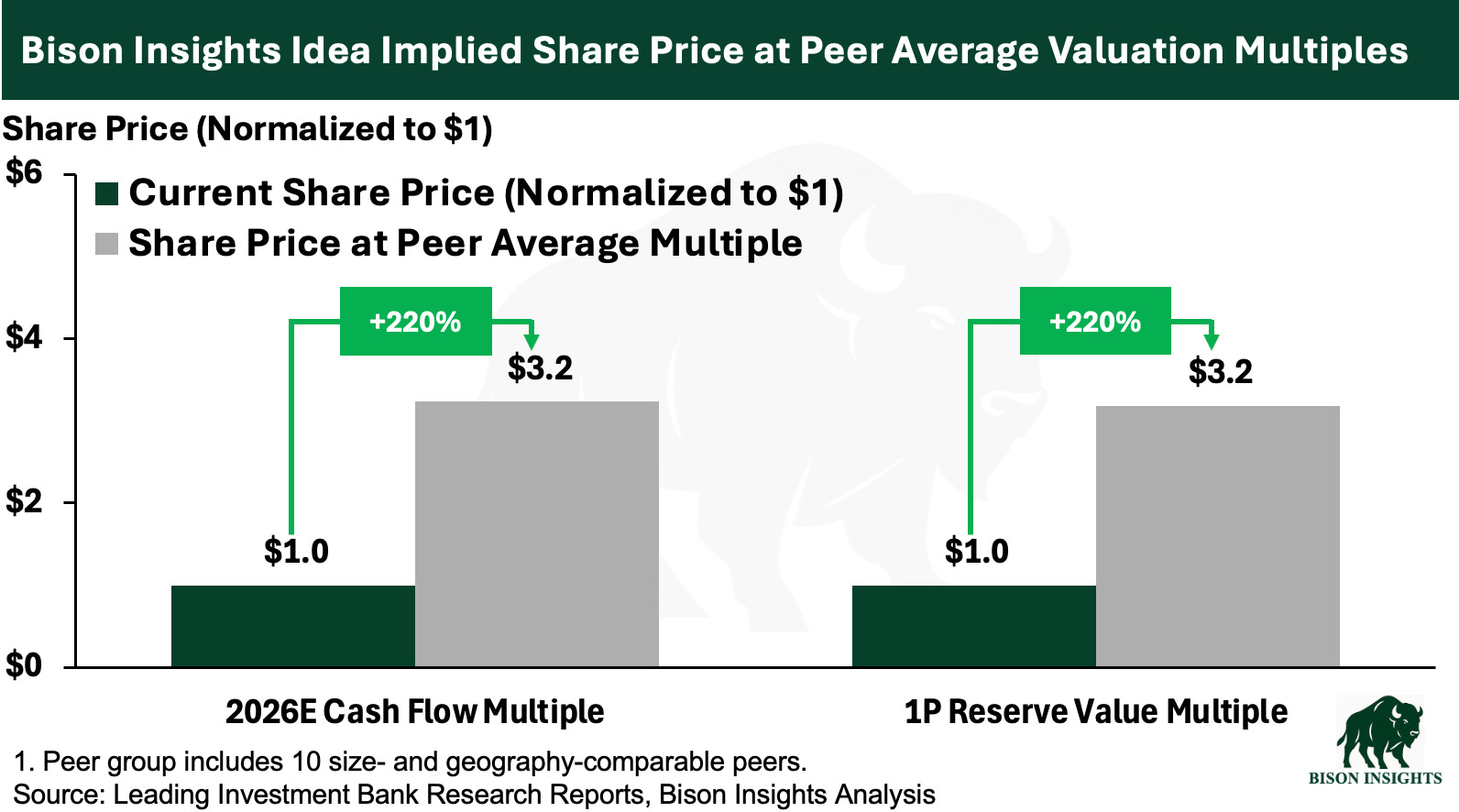

I agree. As this company continues to prove out its turnaround, reduce debt, and repurchase shares, the market should gradually narrow the valuation discount and may eventually assign the stock a premium multiple. If its stock were to merely rerate to the peer average cash flow or reserve multiple, the upside would be compelling:

The company’s oil weighted production provides it with strong upside to higher oil prices. But it is already generating substantially higher cash flow, which is accelerating debt reduction and share repurchases. This process should help drive a faster re-rating toward peer average valuations, which is why I think it offers some of the highest upside in the oil sector today.

This dynamic is simple, yet powerful. And it is happening monthly:

Meanwhile, the existing discount to peers and reserve value presents a wide margin of safety if oil prices move lower, creating a “heads I win big, tails I still win” type of setup. It may trade down in the short term if oil falls, but that could offer even more accretion to the active share repurchase program, which could lead to a higher fair value over time.

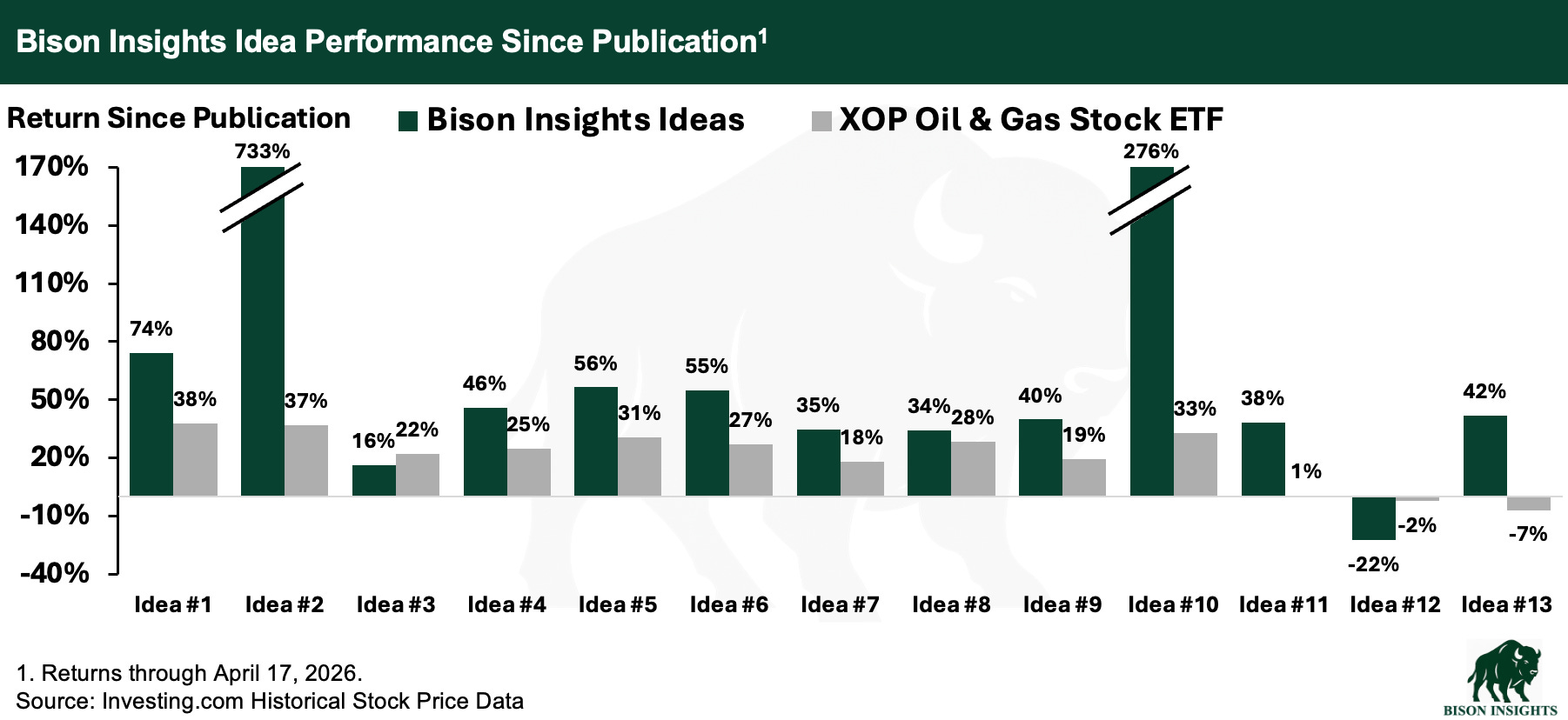

This stock is one of my largest investment holdings and is a new idea here on Bison Insights. Even after the recent pullback in oil equities, other Bison Insights ideas have continued to largely outperform the broader energy market, as they were before the war too:

Disclaimer: This material is for informational and educational purposes only and should not be considered an investment offer, solicitation, or recommendation. Please consult a financial advisor and conduct your own due diligence. Past performance is not indicative of future results.