Three Drilling Stocks with Big Upside Potential

These discounted OFS companies are positioned to be major beneficiaries as the oil industry works to rebuild depleting global inventories

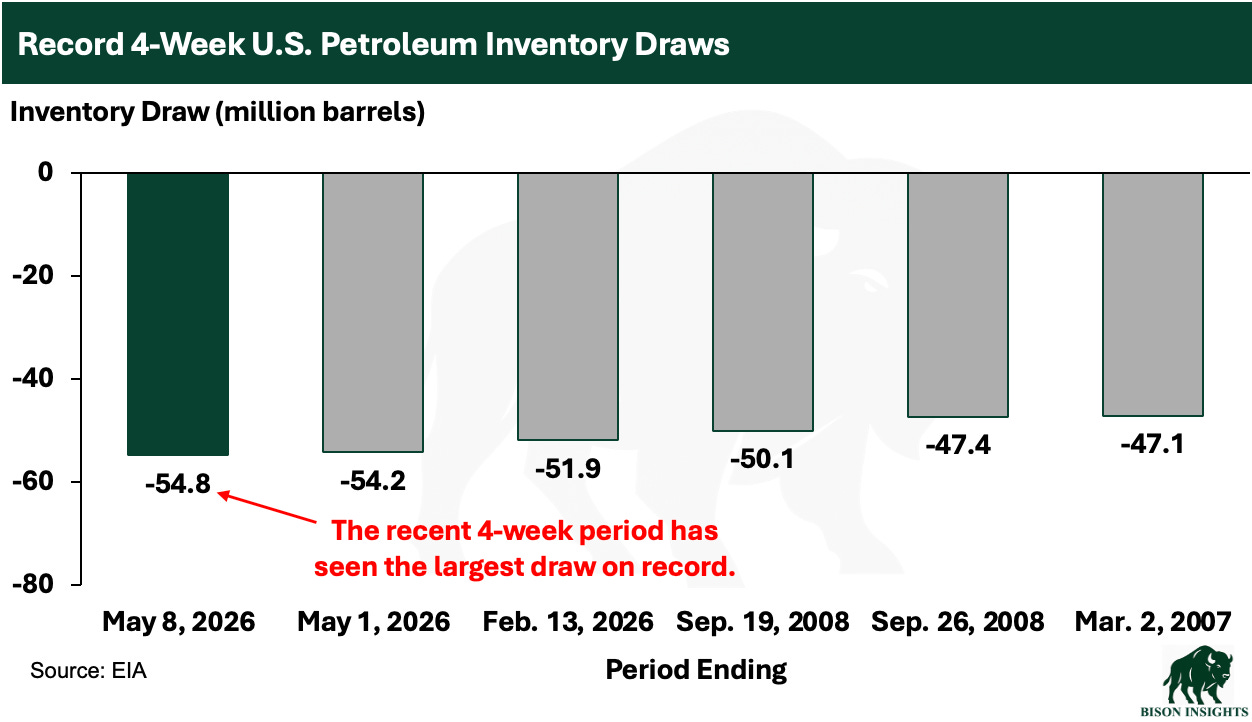

The EIA reported another large petroleum inventory draw this week of 13.7 million barrels. The latest four-week draw is the new largest on record, dating back to 1990:

These draws are consistent with what the IEA has described as the largest oil market supply disruption in history. I expect them to continue as long as the Strait of Hormuz remains closed, and even for some time after, as trade flows will take weeks to months to normalize.

Markets have been remarkably calm about this disruption, despite the enormous scale of it. Global inventories are likely to be drawn down by more than 1 billion barrels from this conflict, and potentially closer to 2 billion barrels if it continues. For an oil market that usually balances at the margin, where even a 1–2 million barrel per day deficit or surplus can drive large price moves, this truly is an unprecedented disruption.

These lost oil barrels will need to be replaced, especially considering that global oil demand hit a record high in 2025 and is expected to rise after this period of near-term demand interruption. Also, Iran has demonstrated that it can disrupt flows through the Strait of Hormuz. As a result, the market arguably needs even more inventory than before - as a cushion against future potential supply shocks.

There’s only one way to rebuild oil inventories, which is to produce more oil than is consumed. Since oil demand is inelastic, that means more oil production will be needed. And that means oilfield services (OFS) companies, which are the companies that producers hire to actually drill and complete their wells, are going to be in high demand.

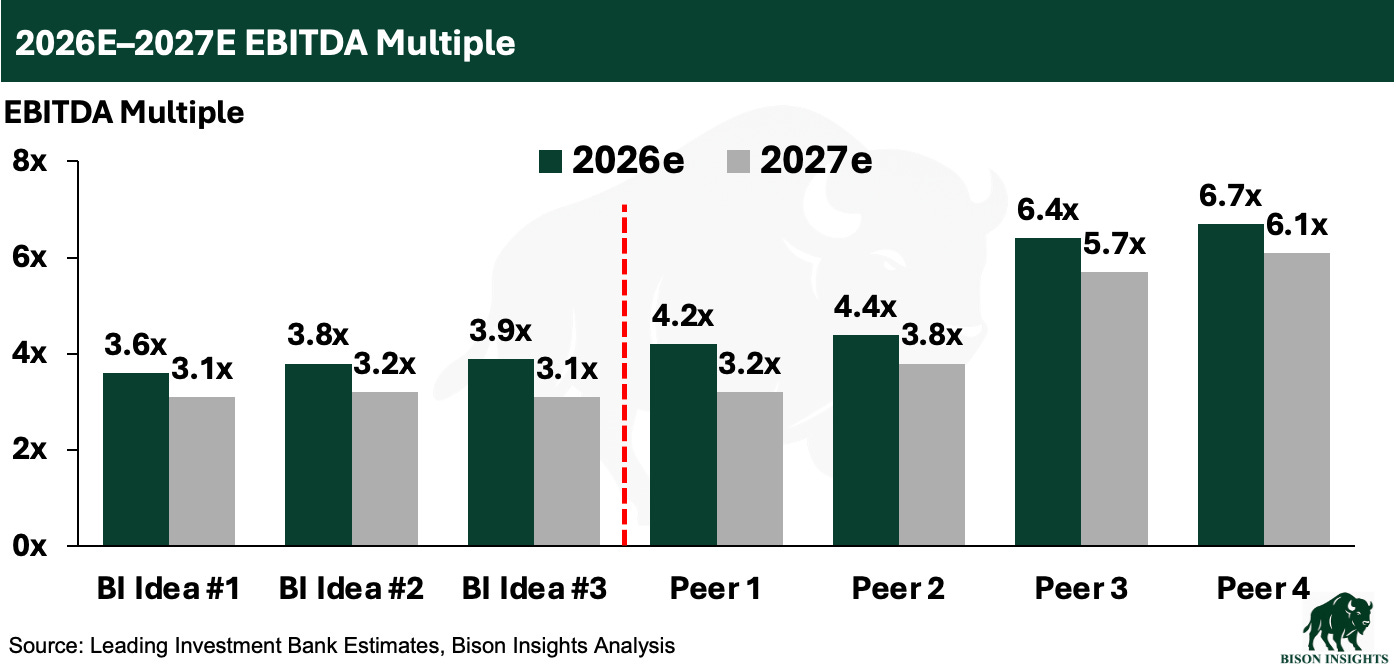

Here at Bison Insights, I’ve written about three OFS companies so far, two of which are focused on drilling services. The stocks have performed well since publication, but because of their smaller size and limited market recognition, they still trade at large discounts to peers:

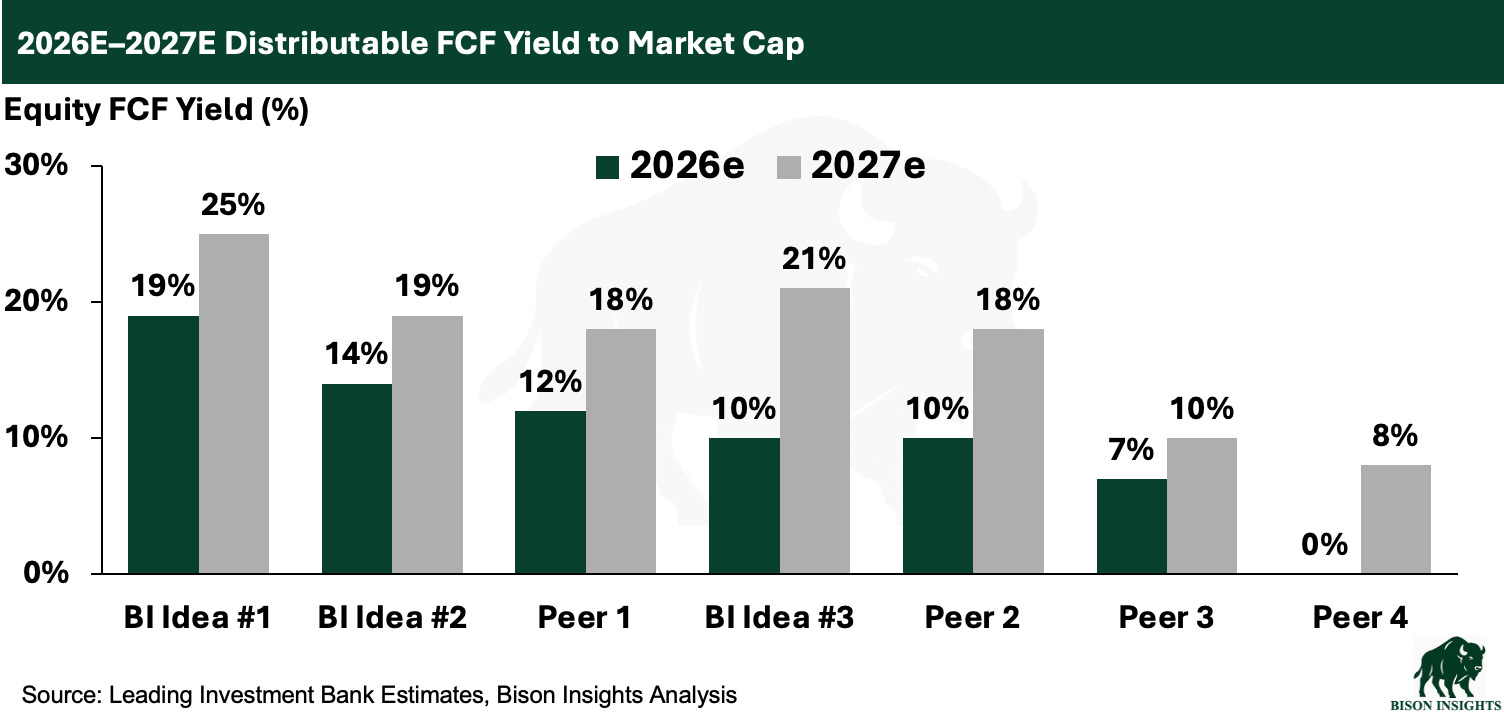

The same is true on free cash flow yield to equity:

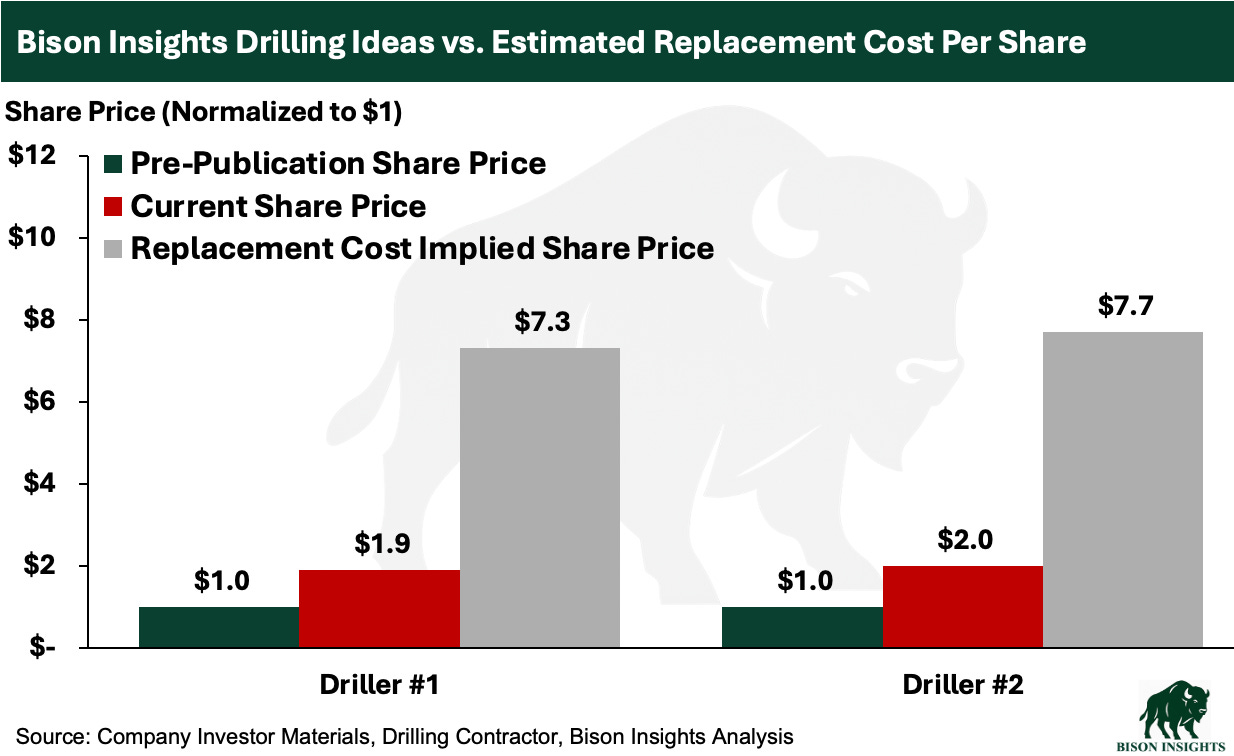

For capital intensive companies like these, I think a good marker for “fair value” is the replacement cost of rebuilding these companies from scratch. Because, as the market tightens, these companies get pushed up to the replacement cost of their equipment. There is a value investment aphorism, to “buy cyclicals at a discount to book value and sell on a multiple of earnings.”

In this case, the two pure-play drilling companies are generating lofty free cash flow yields while trading at a large discount to replacement cost:

Considering the massive oil supply shortfall, I think an “all hands on deck” scenario for OFS may be upon us shortly. In this environment, it makes sense to highlight the sensitivity of these companies’ stock prices in a higher utilization and revenue per operating day environment. In short - they have enormous potential upside, and demand for their services is inflecting higher right now.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance may not repeat itself.