10x or Bust: An Asymmetric Distressed Oil Company Idea in the Midst of Soaring Oil Prices

Two distressed oil companies have turned into multi-baggers in recent months. After recent key developments, this company could be next.

When a company appears headed for bankruptcy, the equity often trades for pennies on the dollar because the market assumes there is little chance of survival. But if its outlook begins to improve, even modestly, its share price can move much higher very quickly as the market reassesses the probability that the company survives.

That dynamic has recently played out in the shares of two oil companies.

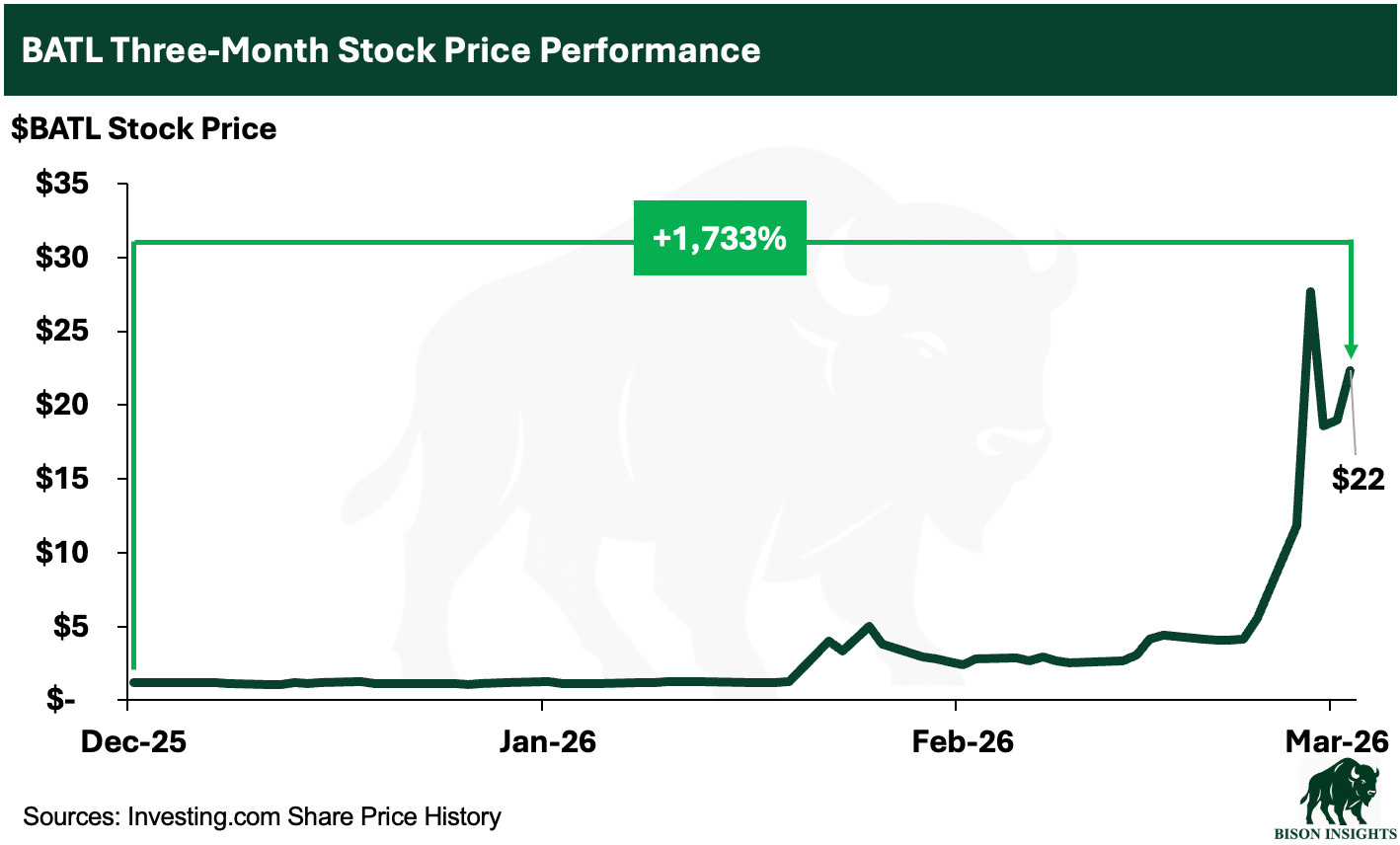

The first is Battalion Oil ($BATL). In its Q3 earnings release, the company had no remaining borrowing capacity, negative working capital, and warned it could fall out of compliance with debt covenants within the next year. At the same time, a key gas-processing facility went offline, reducing production and increasing costs. The stock was effectively trading like a distressed equity with high bankruptcy risk.

Over the past few months, however, several things improved. Battalion fixed its gas-processing issue, which increased production, sold assets some assets to pay down debt, and successfully raised another $15 million of equity at $5.50 per share. The company is by no means “in the clear,” but these steps have improved liquidity and reduced near-term financial pressure.

Because Battalion is a very small company and the stock had become so depressed, these improvements resulted in BATL’s stock price moving sharply higher:

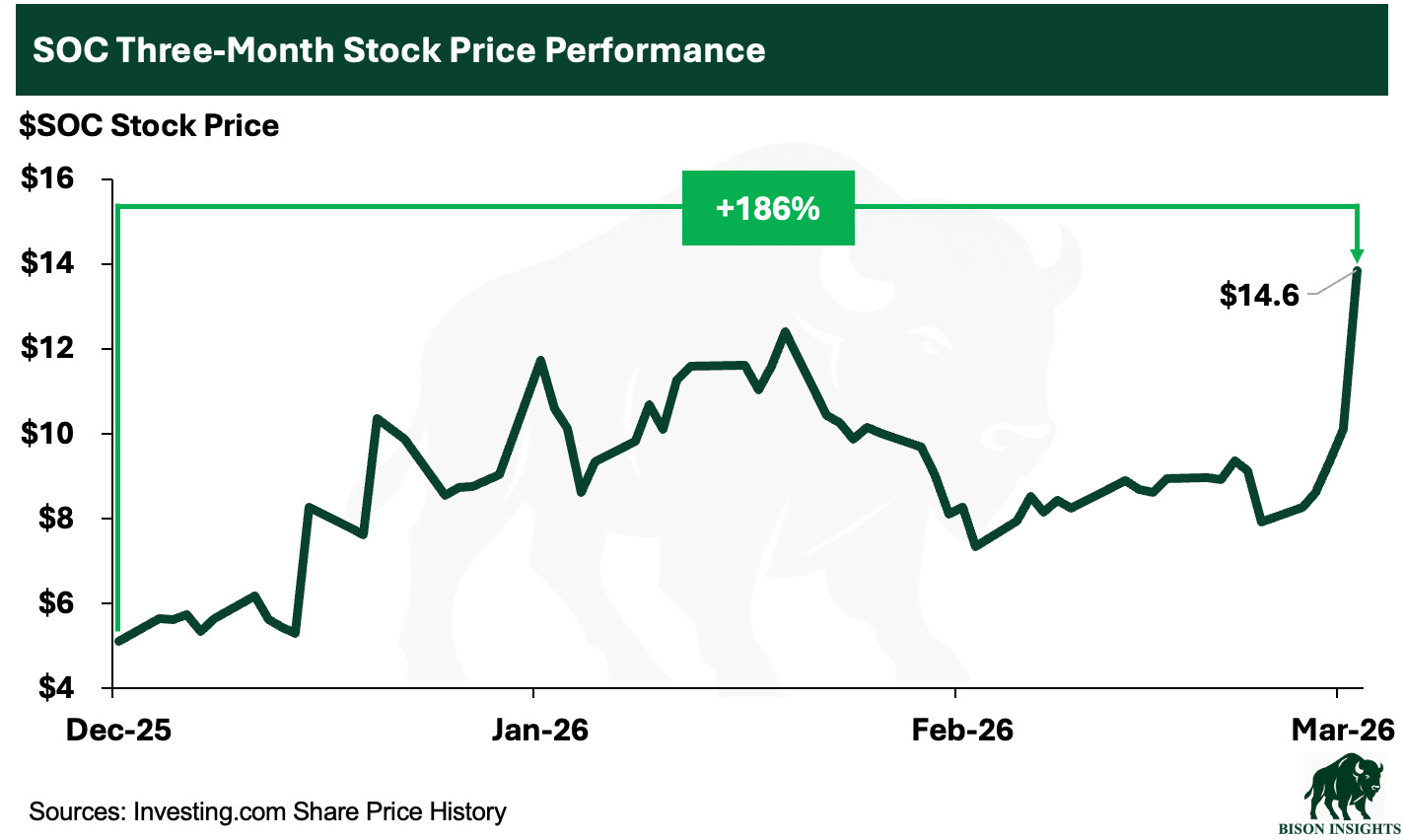

The second oil company is Sable Offshore ($SOC). Sable is essentially a one-asset story centered on restarting the Santa Ynez offshore field and related pipeline system off California.

Sable’s stock has had a choppy ride because California regulators, courts, and related permitting disputes have repeatedly delayed its asset restart path. Additionally, in November 2025, Sable raised $250 million of equity at just $5.50 per share, which signaled that the situation had become more difficult and more dilutive than expected.

The stock has since rebounded because the path to restart is looking more credible again. Federal support has improved, and within the past week the market appears to have reacted positively to a DOJ legal opinion suggesting that federal authority under the Defense Production Act could override conflicting state constraints.

In simple terms, the stock sold off when the market thought the project might be stuck and that Sable was headed for bankruptcy, and it recovered sharply when it looked more likely that the asset will still be able to move forward:

I’ve identified a third oil producer that the market currently views as financially distressed, but which I believe has a credible path to survival.

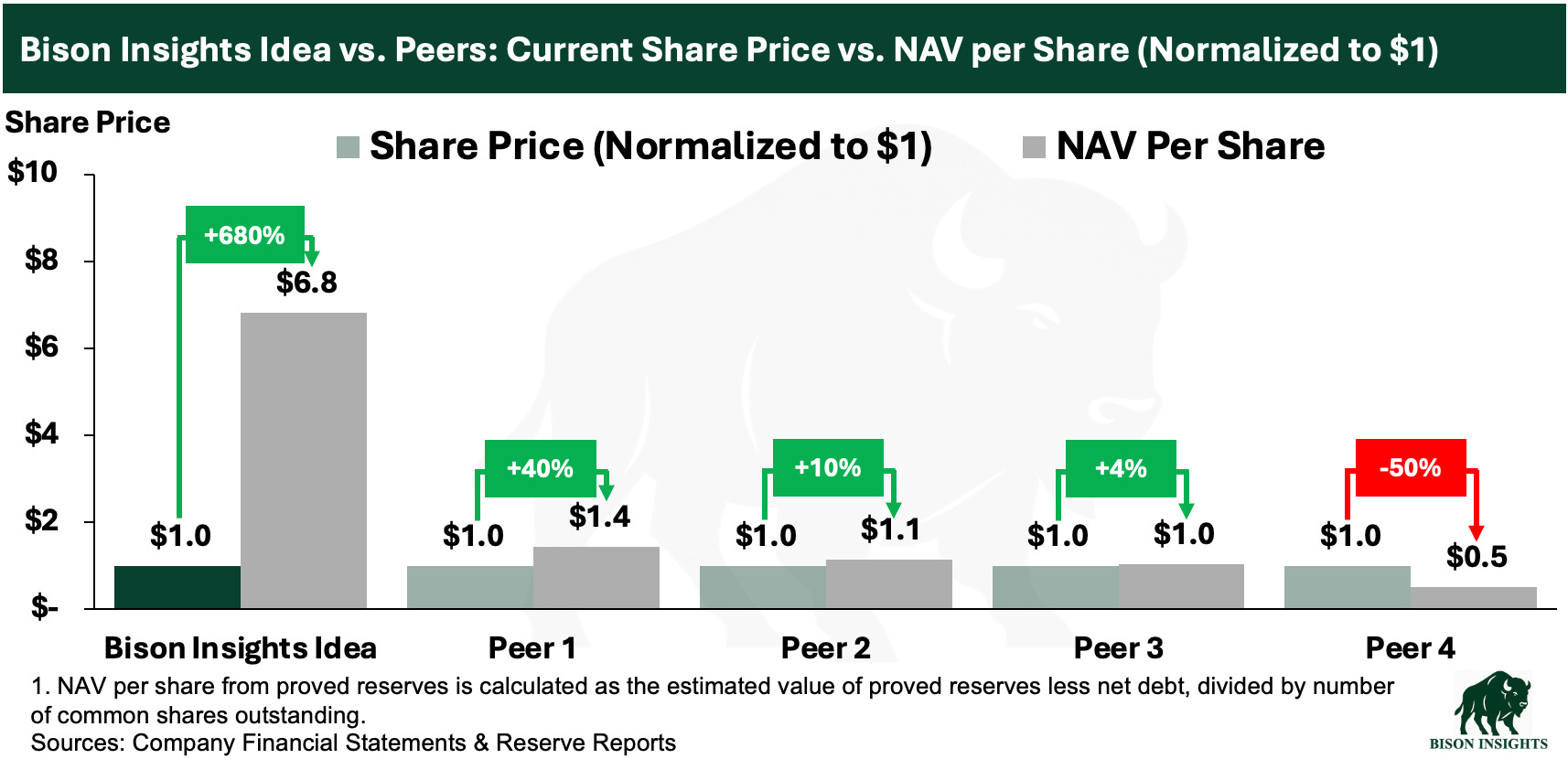

The value proposition is straightforward: the company trades at a fraction of its proved reserve value, a disconnect that’s even clearer when compared to several of its peers.

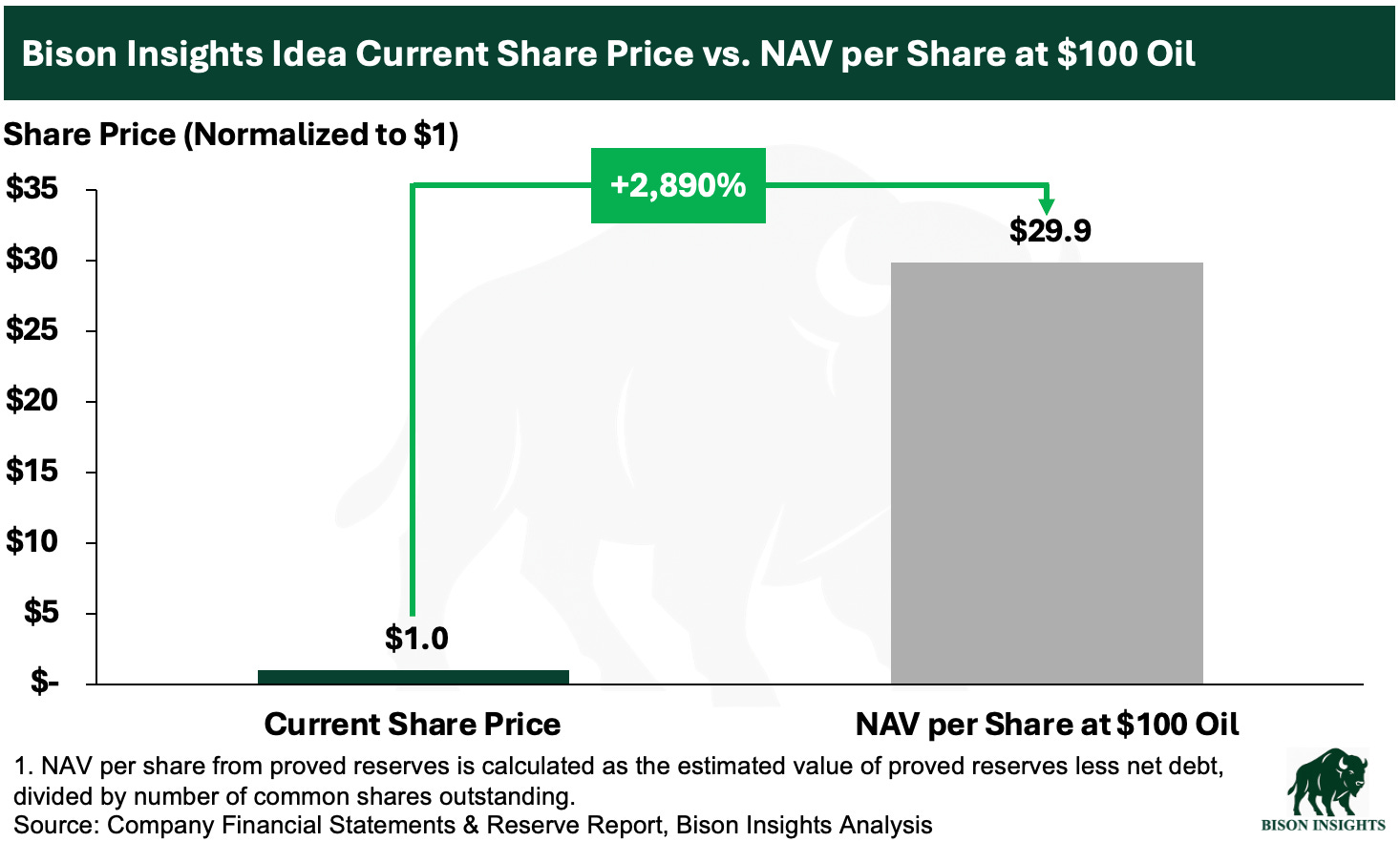

This NAV estimate, based on the company’s latest reserve report, assumes just $65 WTI oil. But with the Strait of Hormuz still closed following Iranian attacks on oil tankers, oil has already moved above $90 per barrel and may quickly move to all-time highs if the Strait remains closed.

Iranian oil infrastructure was also hit over the weekend, and with infrastructure damaged and the conflict escalating, oil prices may rise further and stay elevated for longer than the market expects. That creates enormous upside potential for an equity already trading at pennies on the dollar because investors view it as highly distressed. In a sustained higher oil price environment, the upside potential becomes far more significant:

In this article, I’ll walk through several key recent developments that I believe the market is overlooking, and one major catalyst that may be happening soon.

If this catalyst plays out like I think it will, this stock could experience a rapid equity rerating similar to Battalion or Sable as the market reassesses the equity, offering a true potential 10x boom-or-bust setup. And potentially even more if oil prices rise and stay elevated into the future.

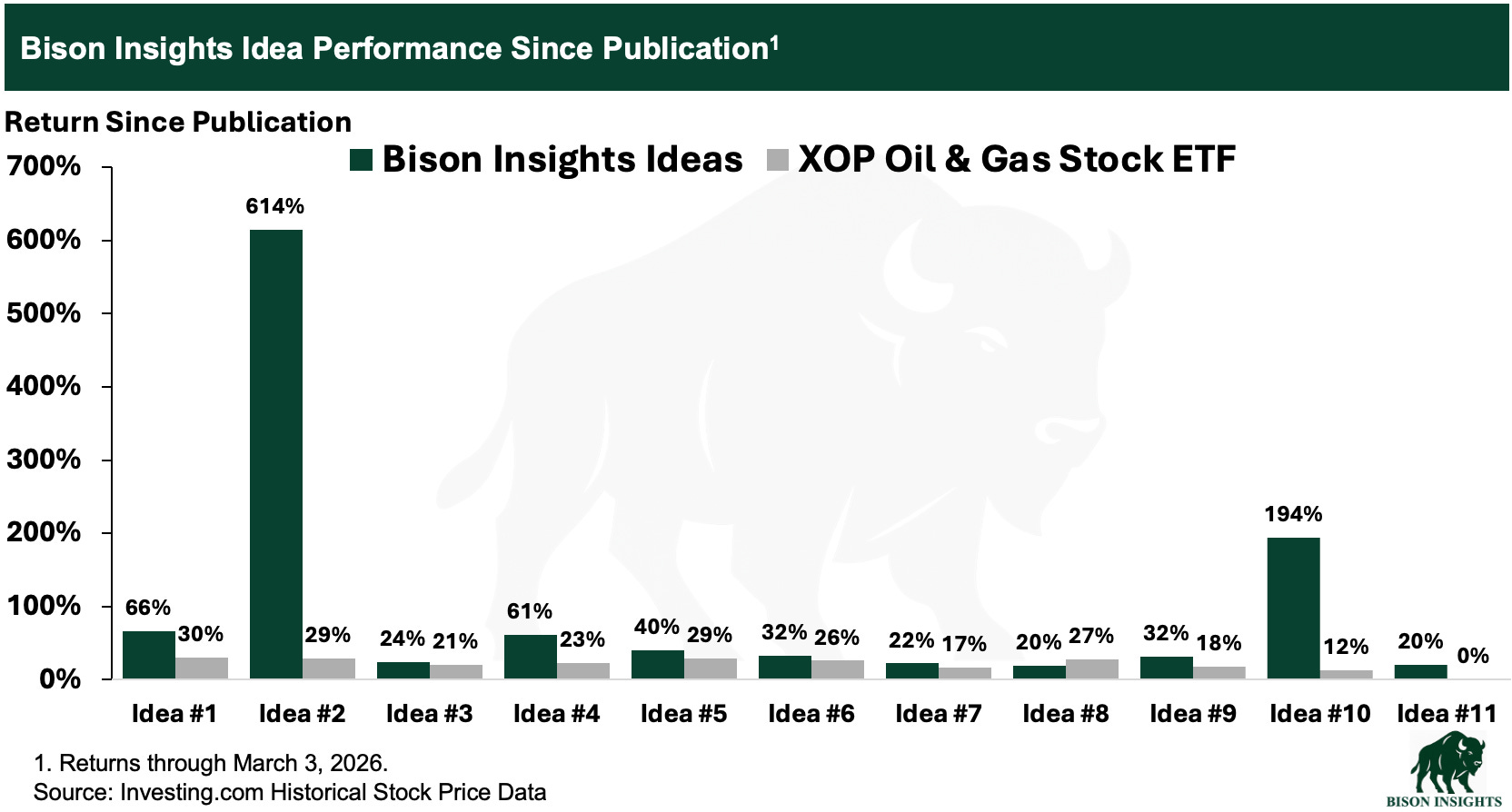

While this may sound aggressive, risky, and perhaps a little crazy, it is the third “10x or bust” idea that I’ve shared here on Bison Insights. You can probably spot the two that I shared on the idea performance chart below - one rose by 614%, and the other by 194% from the time that I wrote about them. This time could be different.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance may not be indicative.

Distressed Oil Company: Prairie Operating ($PROP)

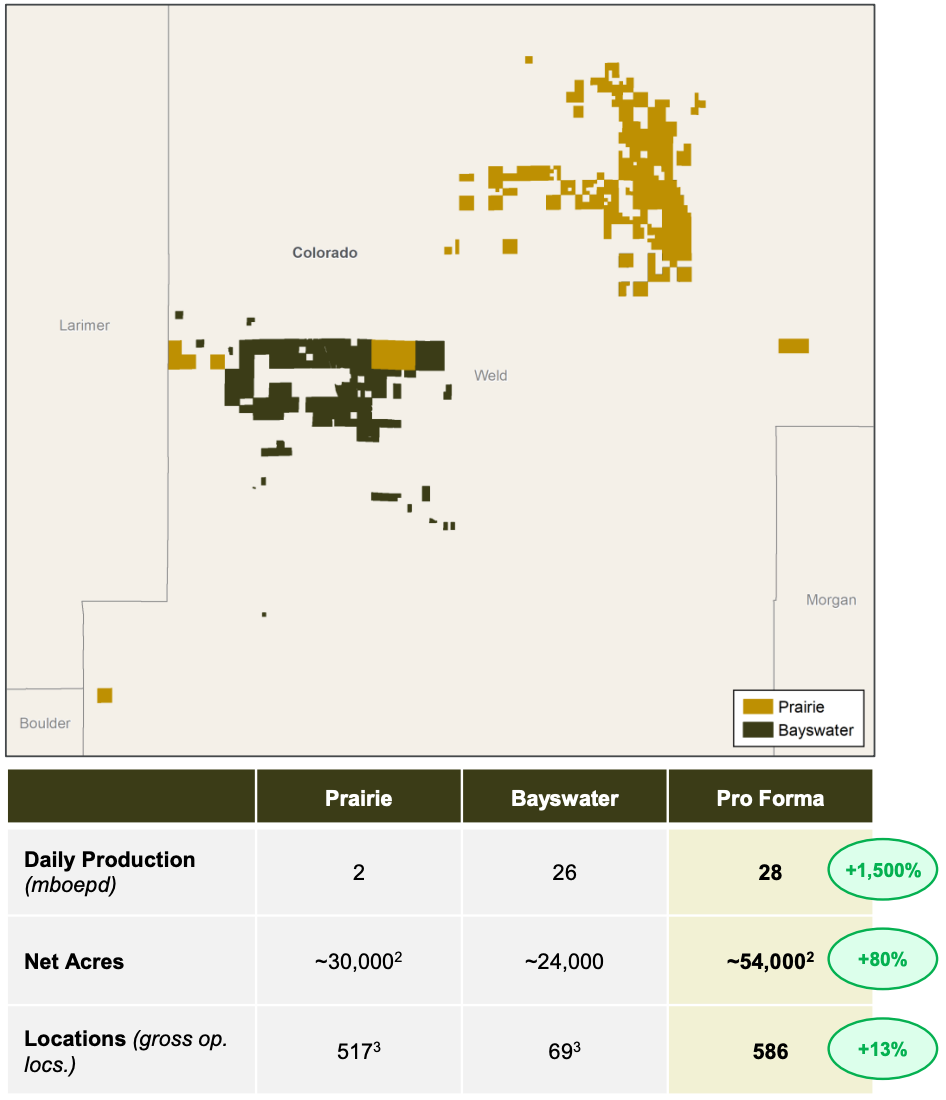

Prairie Operating had an unconventional beginning: it was created through a 2023 merger in which Creek Road Miners, a legacy public shell that had previously been involved in crypto mining, merged with Prairie Operating Co., LLC and took on the Prairie name. After that, the company began assembling a DJ Basin position in Weld County, Colorado through smaller acquisitions and leasehold deals, but it was still a relatively small operator.

Prairie underwent a transformation with its Bayswater acquisition in early 2025. Bayswater brought Prairie roughly 24,000 net acres in Weld County, Colorado, about 26,000 boe/d of mostly oil-weighted production, and about $1.1 billion of proved PV-10:

That deal was the step-change transaction that turned Prairie from a small Colorado DJ Basin story into what is now: a leveraged bet on a much larger set of oil & gas producing fields in the DJ.

Initially, the market approved of the deal, as investors focused on the asset quality and the apparent valuation gap relative to the purchase price. Prairie’s stock rose more than 20% in the week following the announcement, reaching $9 per share.

However, that early optimism overlooked a key issue: the Bayswater announcement did not fully reveal how burdensome the financing would be. In the initial press release, Prairie said the deal would be funded with cash on hand, expanded borrowings under its credit facility, and “one or more capital markets transactions,” which sounds manageable in the abstract.

But by March 24, the real financing package became clear: Prairie launched a common stock offering at just $4.50 per share alongside a Series F preferred stock deal with terms that were highly unfavorable to the common equity.

The Series F carries a 12% cumulative dividend and several very strong holder protections. Those protections include a large warrant package that, under the original terms, on the one-year anniversary of the issuance date (which is March 26th), Prairie must issue warrants if:

1) Any Series F remains outstanding, and

2) The stock has traded below 115% of the initial $4.95 conversion price during the prior 20 trading days.

Because Prairie’s stock is currently far below the conversion price, that second condition has already been met. The only way for Prairie to avoid issuing the warrants now would be to eliminate the remaining preferred before the March 26th anniversary, which would require a full cash redemption of roughly $175 million.

If Prairie cannot redeem the preferred in time, then based on Prairie’s most recent closing price of $1.60 per share, roughly 115 million warrants with a strike price of $1.76 (110% of the stock price) will be issued to the Series F preferred holder. That is nearly double the current ~60 million share count, representing substantial potential dilution. This risk helps explain why Prairie’s share price has been crushed.

In essence, the Series F issuance was a bad deal for common shareholders, and when the dust settled, what first looked like a company buying a big asset at an attractive valuation was actually a company taking big risks and stretching hard to grow.

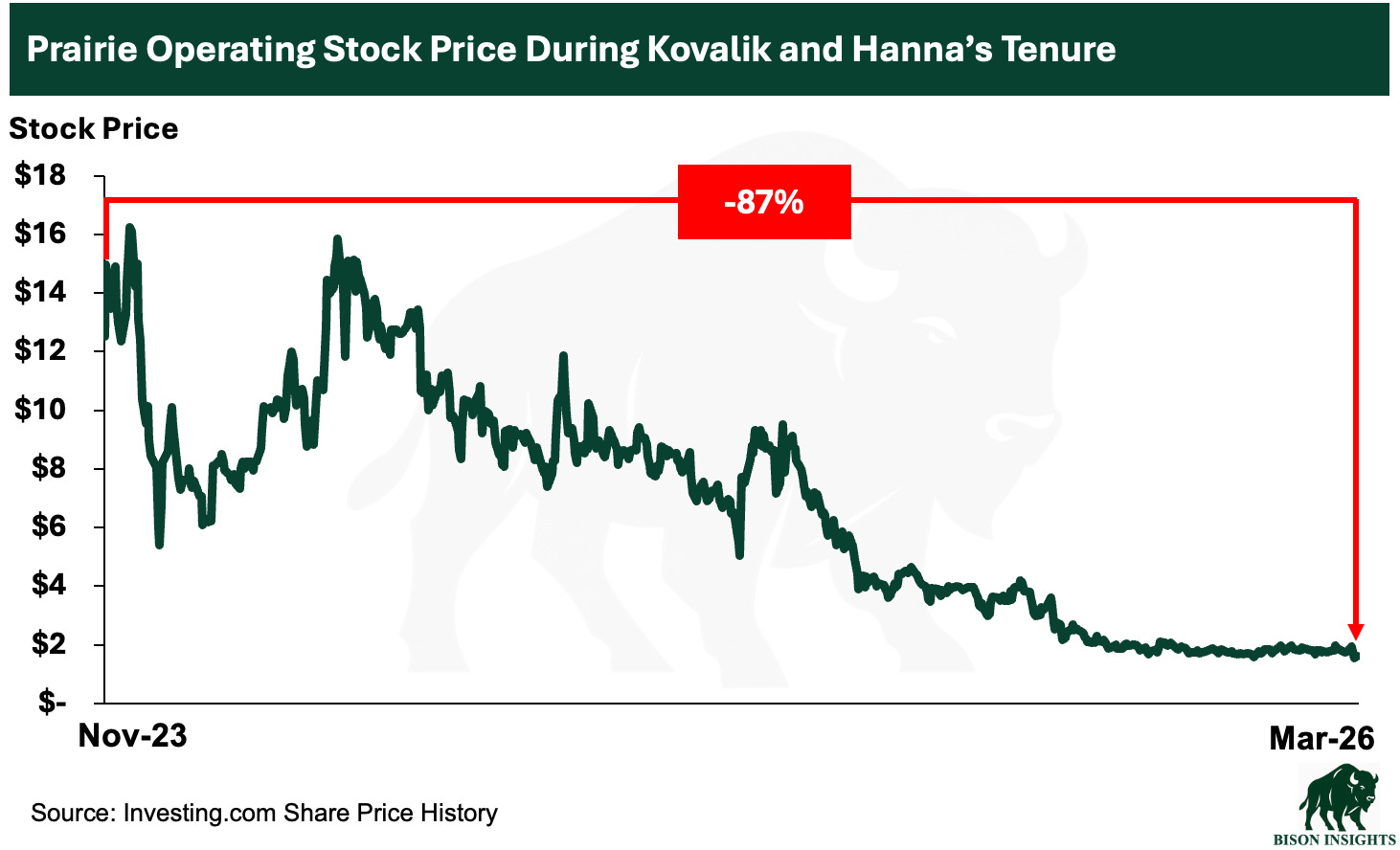

The Prior Leadership Team’s Track Record

The two executives who oversaw this transaction were Prairie’s CEO, Edward Kovalik, and the President, Gary Hanna. These two had teamed up on two other public ventures before.

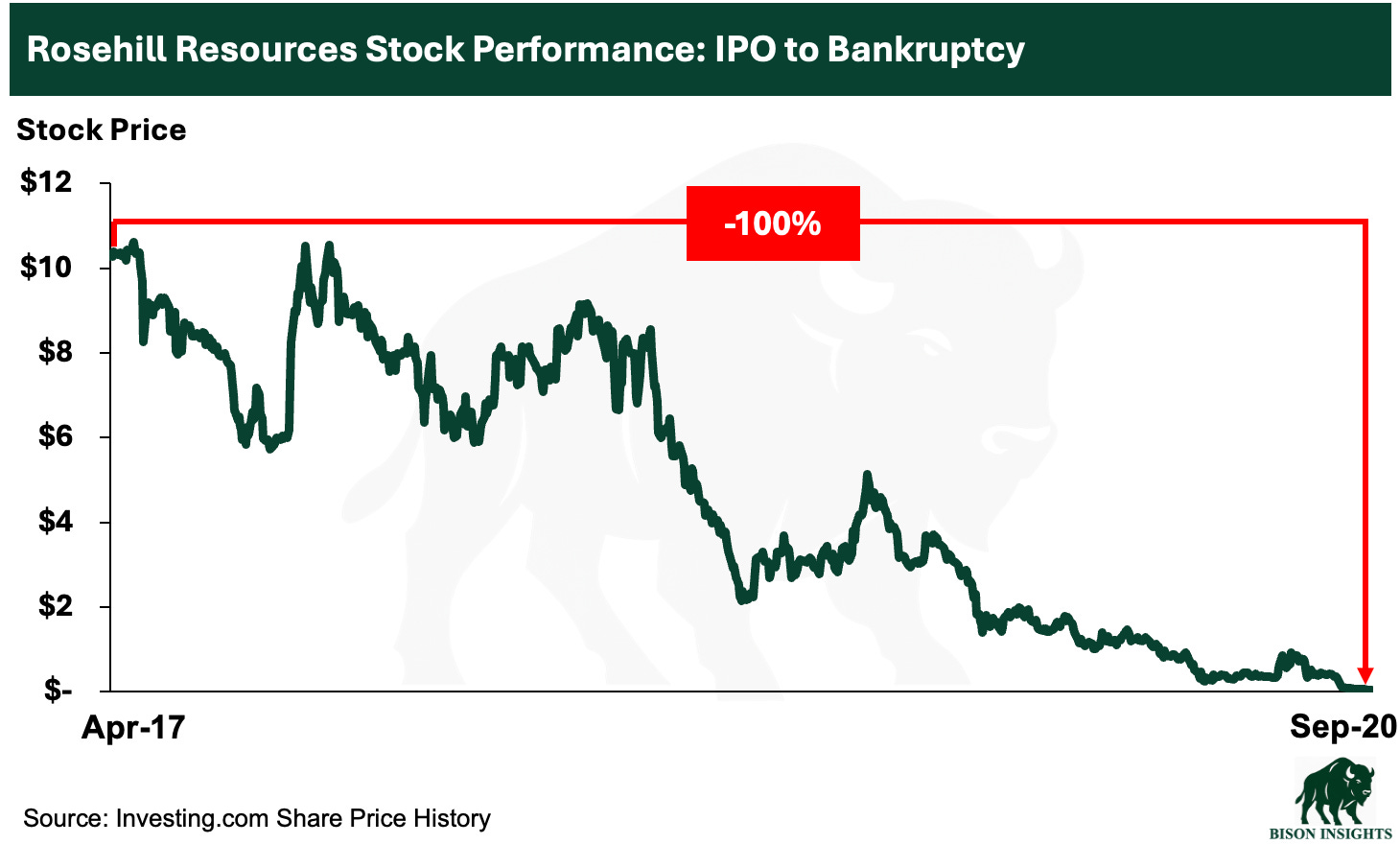

1) In 2017, Kovalik’s energy investment group led the creation of an oil and gas company called Rosehill Resources. Gary Hanna then ran Rosehill as CEO, which later filed for Chapter 11 in 2020:

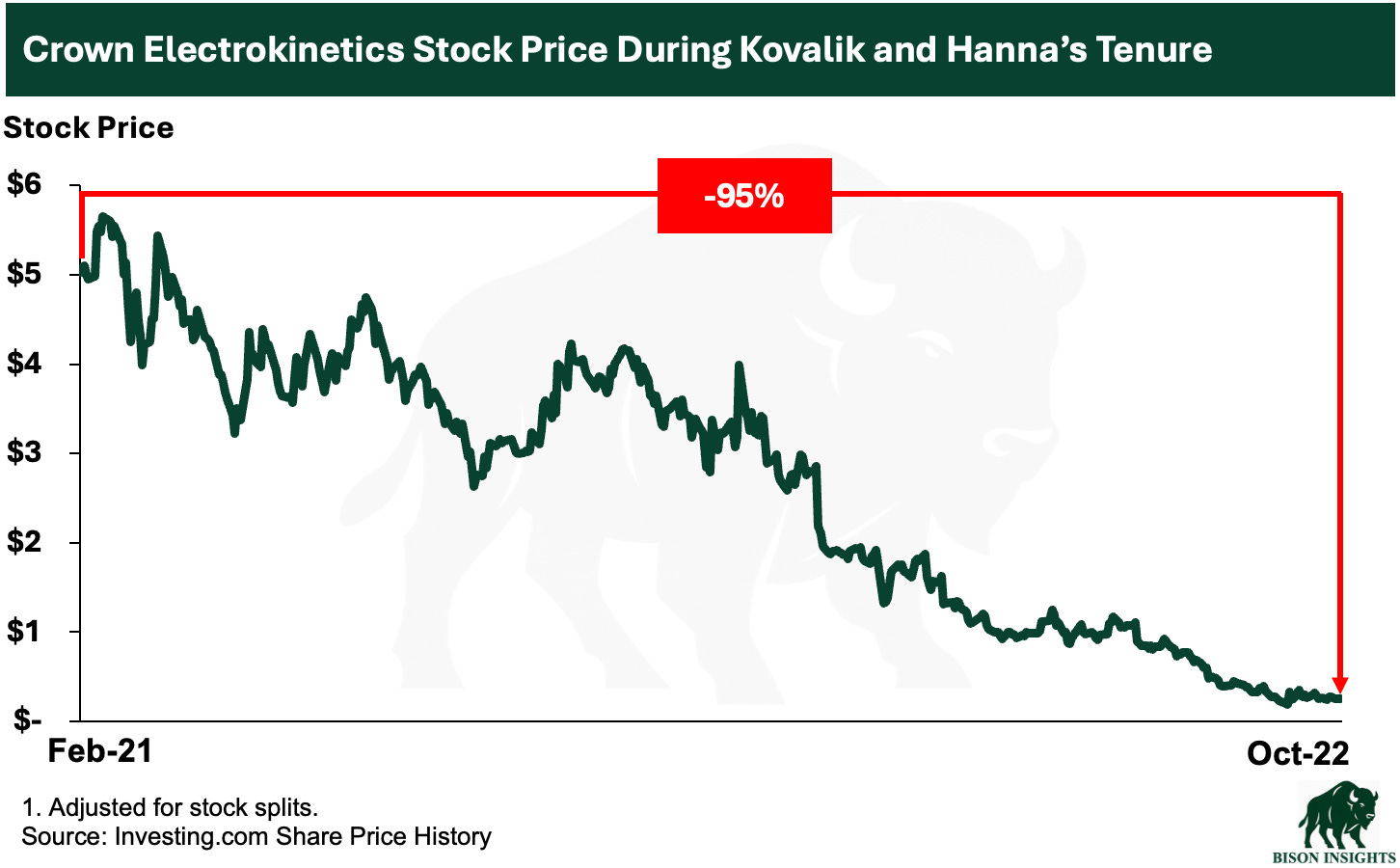

2) After Rosehill, and just prior to Prairie Operating, the two were again involved together at Crown Electrokinetics, a smart glass technology company, from February 2021 to October 2022 where Kovalik served as president and COO and Hanna sat on the board. During their tenure, the two oversaw a 95% decline in the share price of Crown, which was recently delisted from the Nasdaq:

3) Kovalik and Hanna then co-founded Prairie LLC in 2022 and took it public by merging with Creek Road Miners, a public crypto-mining shell. Unfortunately, the third time was not the charm. Here’s how Prairie Operating’s stock performed under their leadership:

New Leadership and Turning the Page

On March 2, 2026, Kovalik resigned as CEO and chairman and Hanna retired as president and director.

In their stead, Prairie has appointed Richard Frommer as interim president and CEO. Frommer is a much stronger fit for what Prairie needs right now. Frommer is the former CEO of privately held Great Western Petroleum, where under his leadership Great Western grew EBITDA from $12 million to more than $500 million, grew production from 1,000 boe/d to more than 60,000 boe/d, and ultimately merged with PDC Energy in a transaction valued at $1.5 billion.

The leadership change does not now guarantee success here, but it’s a great first step for turning Prairie around.

What Frommer Is Taking Over and What Needs to Happen Next

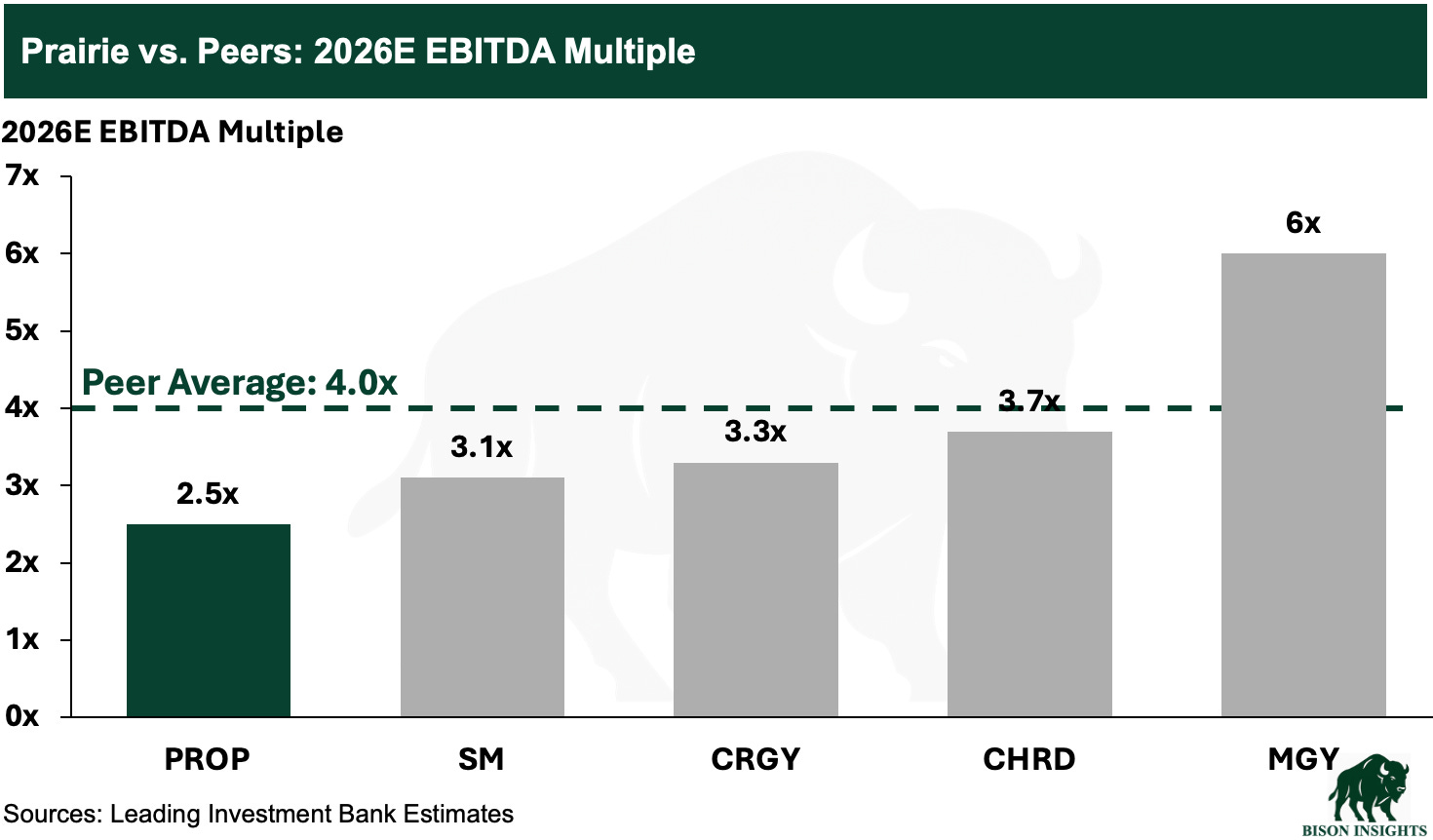

Prairie generates a large amount of cash flow ($250 million in annual expected EBITDA) relative to its current valuation and screens at a discount to other small-mid cap U.S. producers. The peers I’ve included below are representative of the SMID-cap group as a whole:

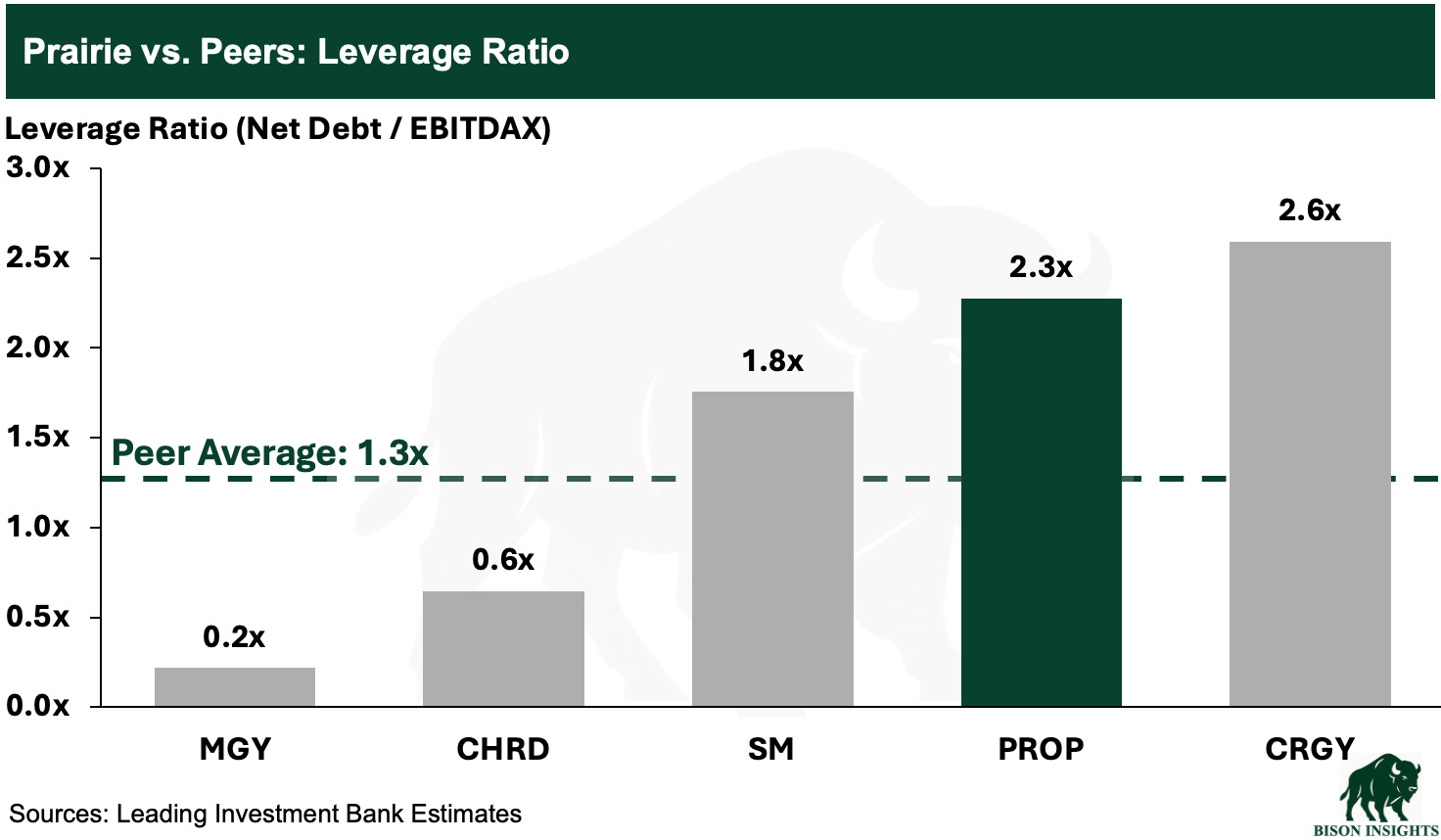

Prairie should use the cash it’s generating to begin reducing leverage, which is not extreme relative to peers:

Operationally, Prairie has recently shown some encouraging signs after initially poor results following the Bayswater acquisition. On the recent earnings call, management said the nine DUC wells it turned to sales on the Opal Coalbank pad delivered an average IP30 of about 525 boe/d per well, which exceeded its expectations, and the company is also successfully lifted base production through lower-risk optimization work.

Those improvements are beginning to show up in the numbers. A recent press release said production had reached about 28,000 boe/d, suggesting the asset base is responding as Prairie becomes more familiar with the properties.

These recent operational improvements and leadership change are extremely important, because it gives Prairie’s operating team more credibility and increases the odds that they can secure external financing to redeem the Series F preferred for ~$175 million and avoid the dilutive warrant issuance.

As I recently highlighted in my recap from a major oil conference several weeks ago, the structured credit market has been strong recently, which reflects rising North American asset values as we enter the twilight period of shale.

In this robust oil & gas financing environment - and as oil prices soar - I think it’s likely that lenders would be willing to provide capital against Prairie’s asset base, which the company’s most recent reserve report values at just over $1.2 billion of proved reserves. Especially considering the new management team and recent operational improvements.

If Prairie can secure financing to redeem its Series F preferred before the one year anniversary on March 26th, the equity would likely be a quick multi-bagger.

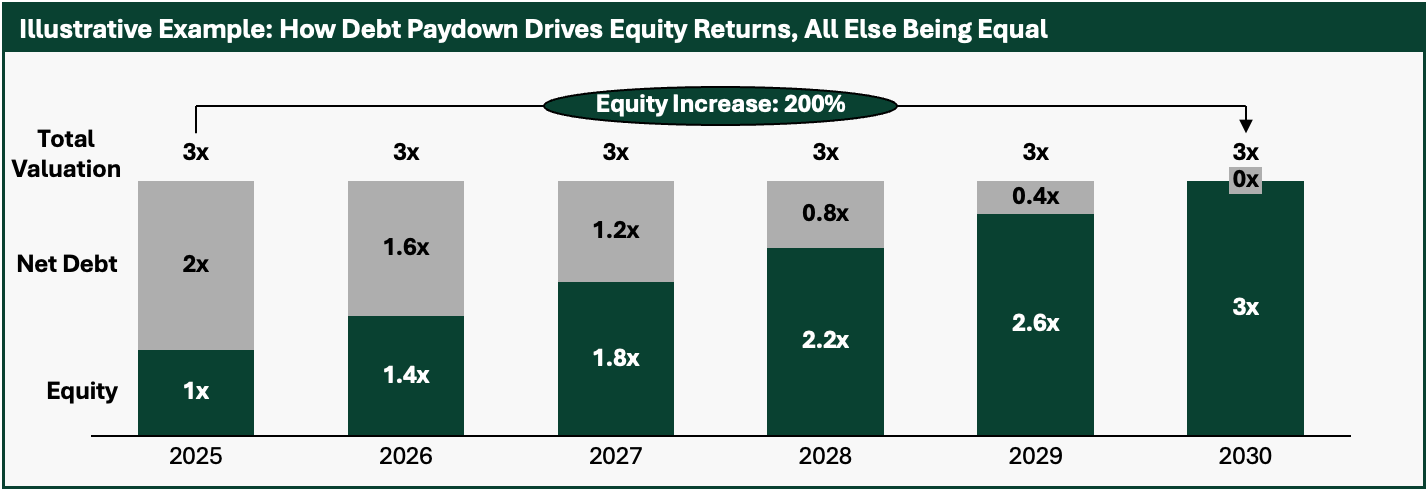

Once financing is secured - if it is secured - the Prairie story would be pretty straightforward. Prairie would need to convert its production into consistent free cash flow, which using management’s roughly 20% base decline estimate and current production of about 28,000 boe/d, I estimate would approximate ~$50 million in free cash flow per year after interest, which it could use to begin paying down debt principal.

As debt is paid down, interest expense falls, which then frees up more cash flow for additional debt reduction, creating a virtuous cycle. Prairie’s credit facility (which has $417 million outstanding as of the recent quarter) does not mature until March 2029, so Prairie has some time to do this.

Importantly, Prairie does not need to fully pay off its facility to secure a refinancing on its credit facility later on down the road. Even modest debt reduction between now and the 2029 maturity could be enough to improve lender confidence and materially change the narrative around the stock.

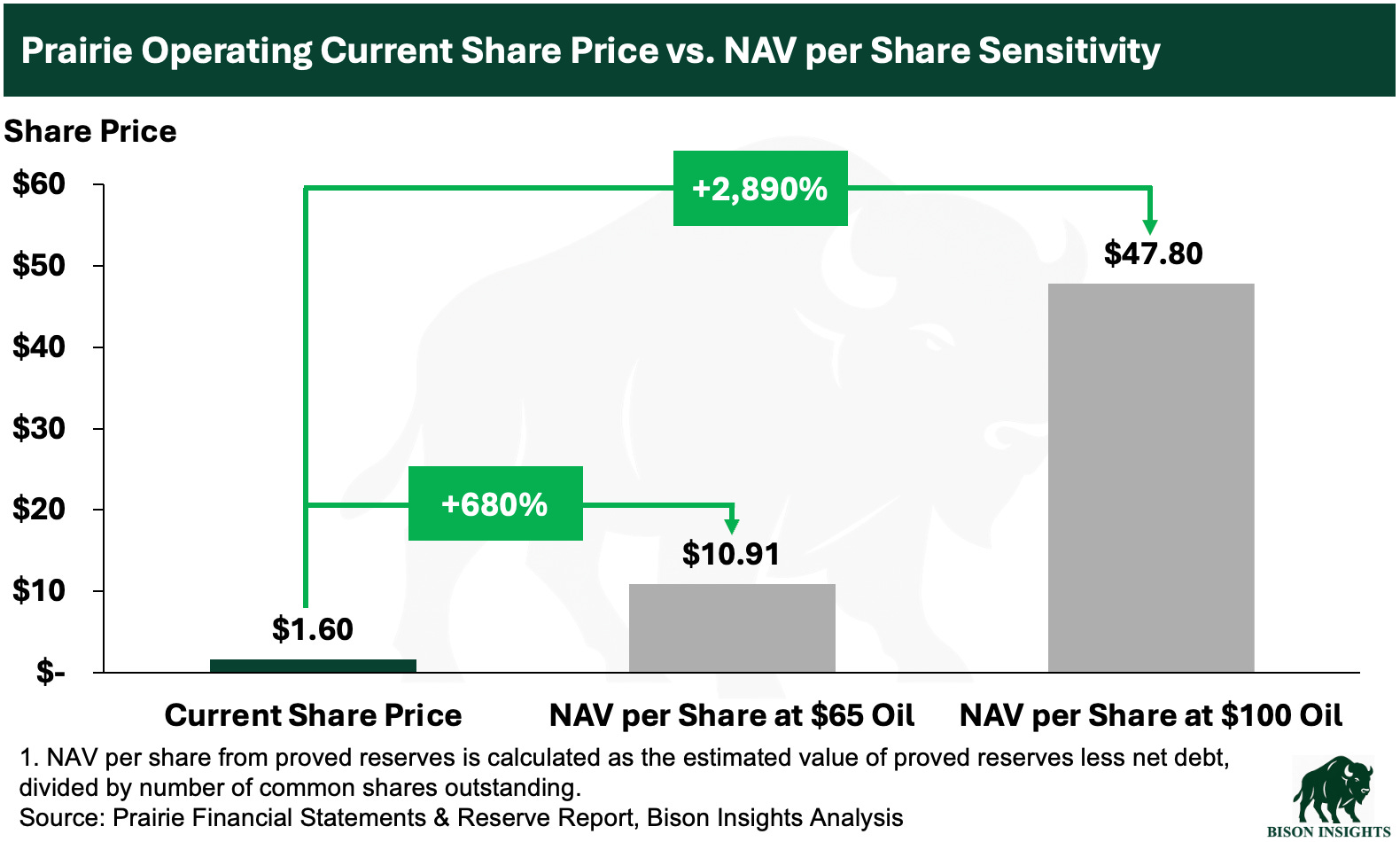

As I mentioned in the introduction, the value proposition here is simple: Prairie has a proved reserve base that is worth over a billion dollars at $65 WTI, but trades at a market cap of less than $100 million. In a “higher for longer” oil price environment, the upside to the equity is much more:

This potential value uplift from higher oil prices makes sense when considering potential cash flow in the $65 oil scenario vs $100 oil. While Prairie is hedged in the near term, new volumes would benefit and the long-term discounted cash flows from the assets would soar from much higher margins and longer reserve life from higher oil prices. The above $100 oil NAV is an estimate, which could be higher or lower depending on varying assumptions. I’m certainly not relying on it as a precise number, but it is helpful in thinking about potential upside optionality of PROP shares, particularly in the context of the recent share price increases of BATL and SOC.

Final Thoughts

Prairie today is a company sitting on an asset base with more than $1 billion of proved reserve value at much lower oil prices than today’s oil price, but in order to acquire those assets it bit off more than it could chew and aggressively diluted common shareholders.

The good news is that the leadership responsible for that capital structure is now gone. A new CEO with a much stronger operating track record has stepped in, and the bet here is that Prairie can refinance its Series F preferred before the warrants are issued on March 26th.

If successful, the equity would initially spike as the market reassesses the company’s equity without the overhang of the preferred, and then gradually grind higher as debt is paid down and equity replaces debt in the capital structure.

The setup is highly asymmetric. It’s worth noting that if Prairie fails to refinance its Series F preferred, the equity has already fallen so far that even with heavy dilution, the per-share NAV would still be above the current trading price. However, I treat that as a “bust” and the share price would likely fall further. In a successful refinancing scenario, the stock would likely rerate quickly and could begin a path to 10x or more if oil prices remain elevated.

In short, while there is risk of a substantial decline, much of the downside already appears priced in, leaving substantial upside if the situation improves.

*Disclaimer: I and funds I advise own PROP shares and related securities and may buy or sell them at any time without further notice. Bison Insights has a “cooling off” period for compliance where no shares are traded in a reasonable time period after publication. There can be no assurance of return or accuracy of anything written. Any investment decision requires diligence and, if appropriate, an advisor should be consulted. I am not your advisor, and this is meant for general information and educational purposes and not as personalized investment advice. No personalized advice can or will be provided by Bison Insights. Past performance may not repeat itself. The views expressed here are solely those of Josh Young and do not necessarily represent the opinions, strategies, or positions of any other person or organization.

Hi Josh, I just Checked this company a few days ago, what about the hegdes they have? It looks like is a big portion of their production of 2026 to 2028. It will limit a lot of the upside?

Thank you for your insights.

Thanks for this Josh. Do you have an idea what the coupon on the debt would look like, assuming they could refinance, and

Any insider buying recently?