Expert Interview: A Misunderstood, Highly Accretive Acquisition with Decades of Oil Reserves

Interview with a leading expert on key assets for a recently discussed company, their just-closed acquisition, and the long-term economics the market appears to be overlooking.

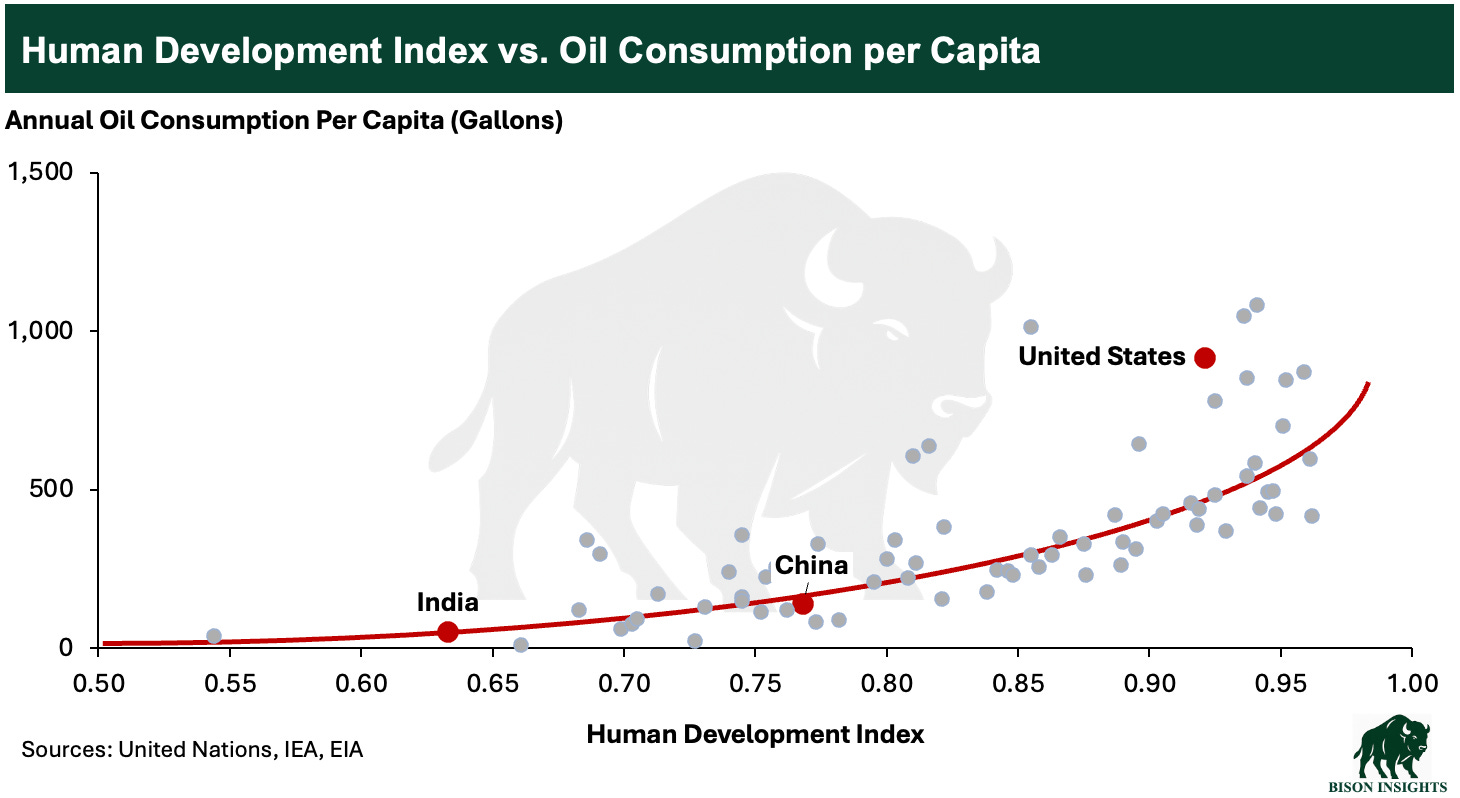

In my recent article, Immediate Upside and Long-Term Growth Potential, With Decades of Oil Reserves, I laid out my investment thesis on a company with long-life oil assets that I believe offer one of the most attractive ways to gain exposure to structurally growing global oil demand. Most of the world’s population lives in developing countries, and as incomes rise, energy consumption rises with them. Oil demand tends to grow almost automatically as living standards improve. In my view, the world still has substantial oil demand growth ahead:

The simplest way to gain exposure is to own a company with decades of oil reserves. As new supply becomes harder and more expensive to develop, oil prices must rise to incentivize drilling. But if you already control reserves that can last 30 to 40 years, you do not need to keep spending capital to replace production. When prices rise, the value of what you already own increases, and most of that upside flows directly into profits.

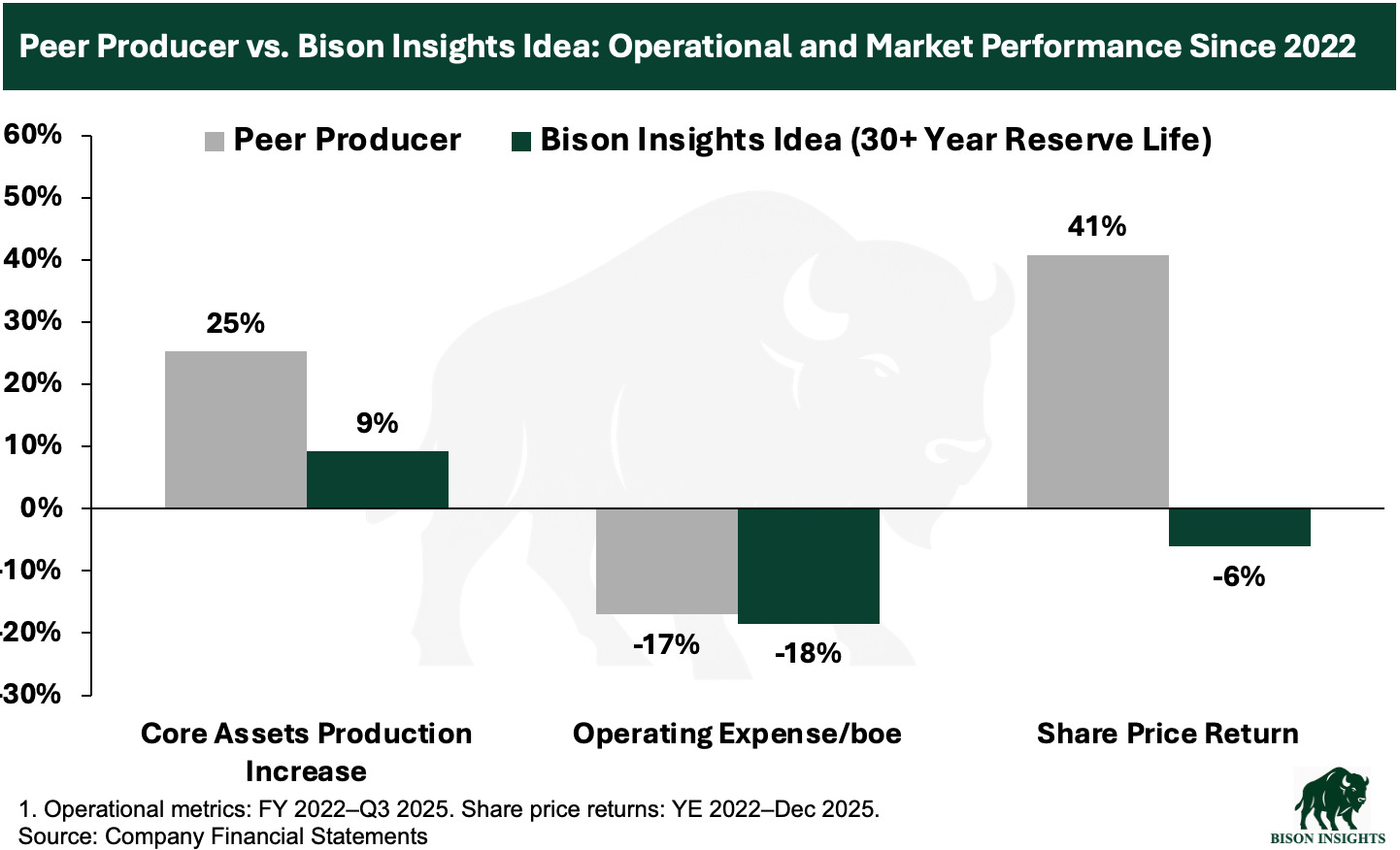

The company I highlighted has roughly 30 years of oil reserves at current production levels. And over the past several years, it has undergone a major operational inflection, delivering record production, steadily declining operating costs, and a meaningful improvement in its second major operating segment. A close peer that achieved a similar combination of production growth and cost reductions saw its share price rerate sharply higher. This company, however, has lagged meaningfully, despite comparable operating progress:

In my view, this valuation disconnect is unwarranted. In addition to substantially improving its core operating performance, the company recently completed a large acquisition that appears far more accretive than the market is giving it credit for, extending its already long reserve life and unlocking material operating efficiencies across its core assets.

To dig deeper into the quality of these assets and the true economics of the acquisition, I interviewed an expert who previously spent nearly a decade as a senior reservoir engineer at the company I wrote about, followed by several years in a similar role for a large U.S. oil producer with high-performing local assets. He is a thought leader, having advanced more than a dozen patents related to local area oil production and emissions reduction and now runs his own company helping local operators optimize production from their assets.

The full interview is available below, including a full transcript.