OPEC+ Is Increasing Oil Production, But Oil Prices May Rise Anyway

The OPEC+ Equation: Higher Production, Less Spare Capacity

For the last several years, the market kept a thumb on the scale because OPEC spare capacity sat in the background as a cushion. Extra barrels “available on short notice” meant any tightness could be met, so oil prices carried a discount, despite low inventory levels. That logic was simple: more cushion, less risk, lower price.

Today that cushion is largely gone. The barrels that once lived in spare capacity are now in production, and what remains is thin at best, as I’ve highlighted before in my work on OPEC+’s spare capacity. The per barrel trade-off between higher OPEC+ production and lower spare capacity may not be perfectly one to one, but it should be close: if the market discounted price for years because spare capacity reduced risk on the upside, then a meaningful reduction in that buffer should lift price by removing that insurance.

We aren’t seeing that uplift - yet. The market continues to price oil as if the spare-capacity cushion still exists, even though it has already been spent. That disconnect, combined with several other important fundamental factors, is offering what I see as a compelling bullish setup for the oil market.

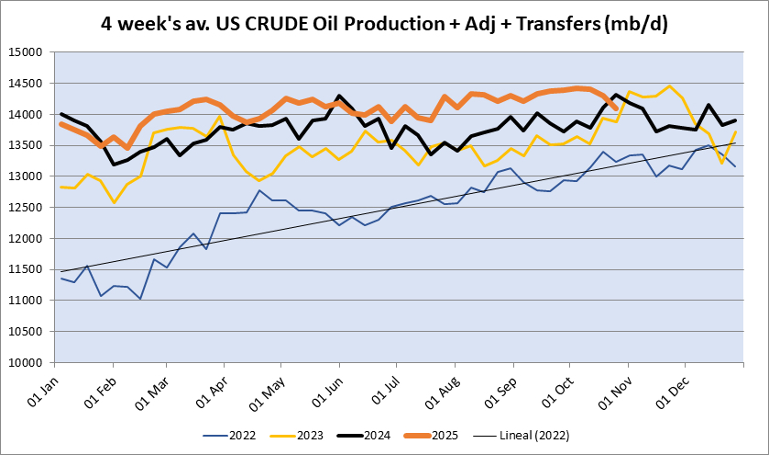

Concurrently, U.S. shale oil production appears to be rolling over. Shale was the marginal source of oil supply for the past 10+ years, and US shale production going into decline would be a compelling reason to buy oil and related equities here rather than waiting to see how the OPEC+ standoff resolves.

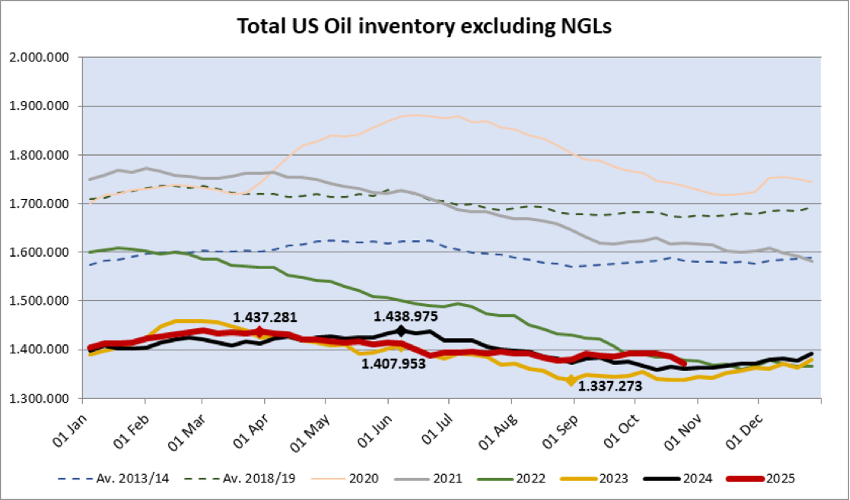

Meanwhile, U.S. oil inventories excluding NGLs haven’t risen meaningfully.

Instead, headlines have zeroed in on the increase in global crude supplies “on water,” without considering the offsetting factors of lower OPEC+ spare capacity, longer voyage times from Russia due to sanctions, and oil stuck in floating storage due to sanctions.

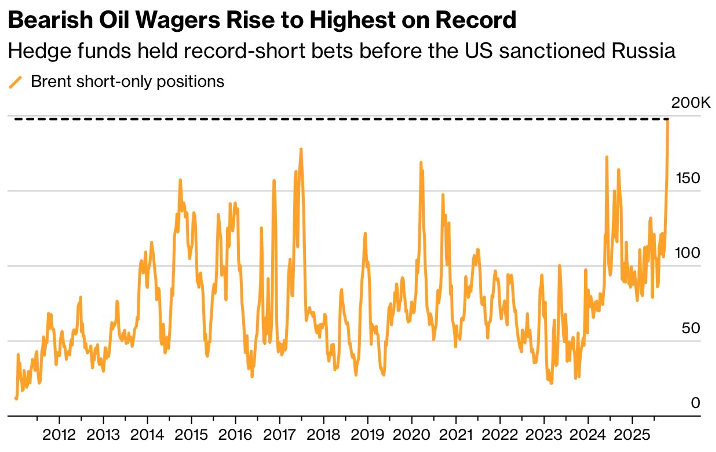

At the same time, bearish oil wagers were recently at record highs, suggesting this potential “glut” is already priced in. Extreme bearish market positioning limits downside risk and sets up high upside potential if sentiment swings the other way.

China, which has historically been the low bidder in the oil market, is taking advantage of current low prices by aggressively building inventories and adding eleven new oil reserve sites this year. What do they know?

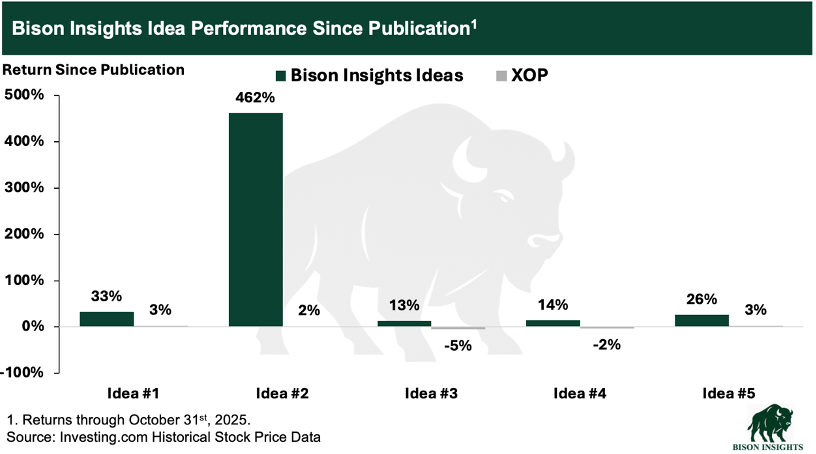

Overall, the medium- to long-term outlook for oil prices looks increasingly constructive. Despite short-term oil and gas price volatility, the ideas I’ve shared here on Bison Insights have performed very well since publication, as I recently highlighted in Oil Price Falls, Bison Insights Ideas Rise.

I look forward to continuing to share compelling, high potential upside ideas as we progress into a constructive setup for oil and gas markets.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance may not repeat itself.

Outstanding insights on the oil market

I wonder if oil price will experience much downward pressure once China decides they have enough oil in their strategic reserves.