Trump Calls for $50 Oil After Venezuela Intervention - This Will Backfire

"Do you want a shortage? Have the government legislate a maximum price that is below the price that would otherwise prevail.” — Milton Friedman

Earlier this week, President Trump signaled that he wants oil prices to fall to $50 per barrel following U.S. intervention in Venezuela and the redirection of Venezuelan crude toward U.S. refineries.

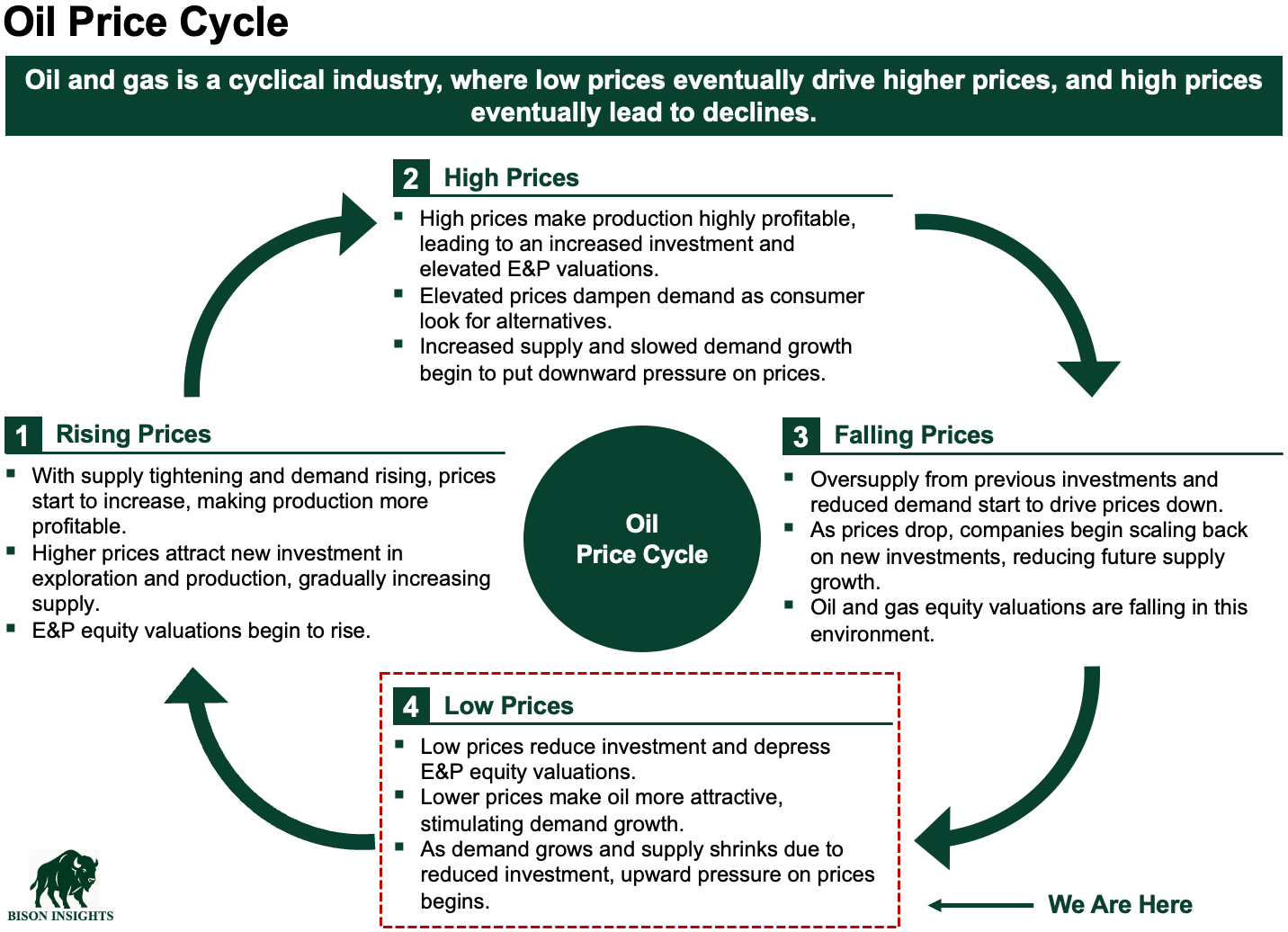

At a surface level, this appears bearish for oil prices. History suggests, however, that when governments attempt to push prices down, the result is often the opposite over time. Producers respond to profit incentives, not policy preferences; if the price of a good is not high enough to generate an acceptable return, reinvestment slows, leading to declining production. That reduction in supply ultimately forces prices higher (and sometimes much higher). Oil is no exception.

Oil Prices in Historical Context

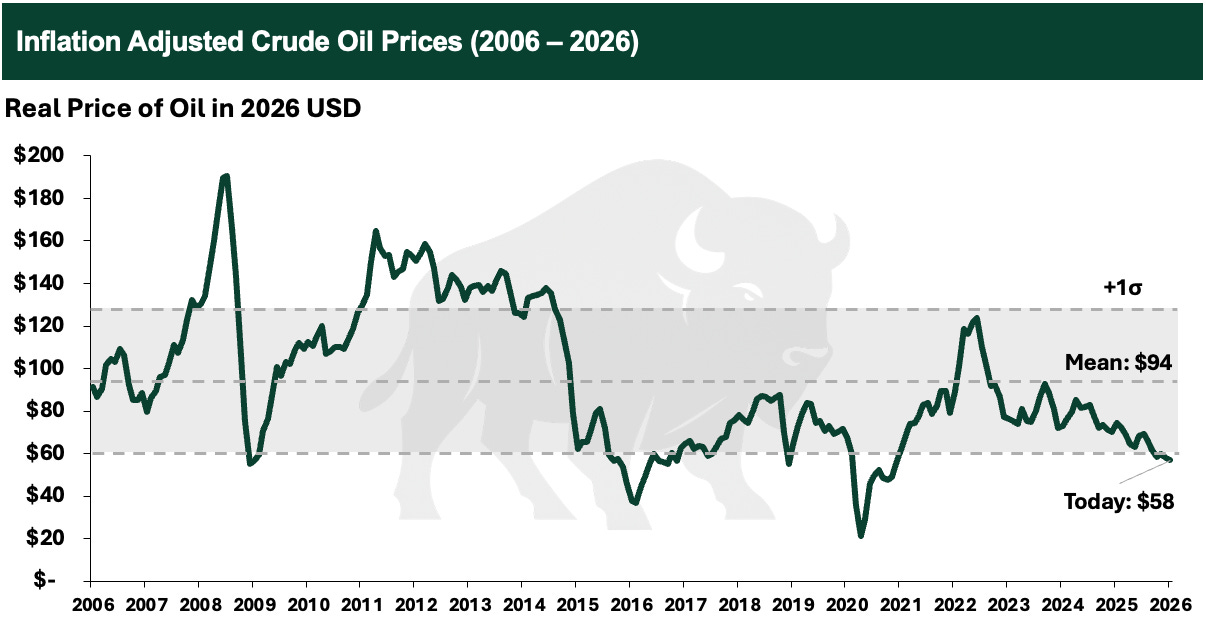

In real terms, oil prices today sit near the lower end of their historical range. A more “normal” WTI oil price, when adjusted for inflation, is closer to the low-to-mid $90s:

What is fascinating, however, is that oil prices rarely stabilize around fair value. Instead, they tend to overshoot in both directions, resulting in what can be described as “bi-modal” pricing:

This overshooting reflects the lagged response of oil production and the wide range of participants in the market, making meaningful central coordination nearly impossible. When prices are high, most producers respond. Capital floods in, drilling accelerates across the industry, supply grows, and prices eventually collapse. When prices are low, the opposite occurs. Investment pulls back broadly, drilling slows, decline rates take over, and supply erodes, eventually forcing prices higher to restore balance.

This is the recurring structure of the oil cycle. It also highlights the central irony of government efforts to suppress commodity prices. By pushing prices down, policymakers incentivize the very behavior—reduced investment and lower supply—that ultimately forces prices much higher.

How Producers Are Responding to Current Price Signals

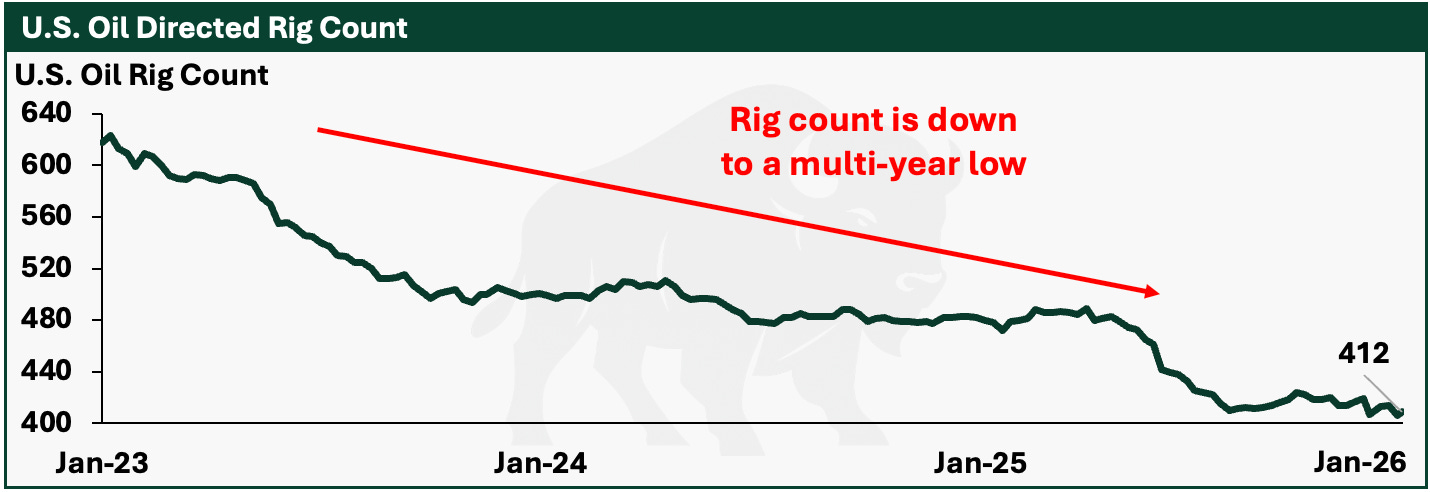

In real time, the cyclicality of the oil market is playing out. The oil rig count in the U.S., the largest oil producing country in the world, has been falling steadily as lower oil prices over the past several years has caused investment to dry up:

Because oil production declines naturally over time, operators must continuously drill new wells just to keep production flat — particularly with so much production from high decline shale fields. At today’s low rig count, operators are not drilling enough wells to maintain, let alone grow, oil production. As a result, U.S. oil production is expected to peak and begin declining in 2026.

In addition, from an expert interview I recently published in Peak Shale? An Insider’s Perspective, evidence suggests that U.S. shale productivity is peaking. The combination of declining well productivity and rig count means that today’s low prices increase the likelihood of lower production in the future and will also make it more difficult for operators to ramp up production when prices eventually rise.

Positioning for the Next Phase of the Cycle

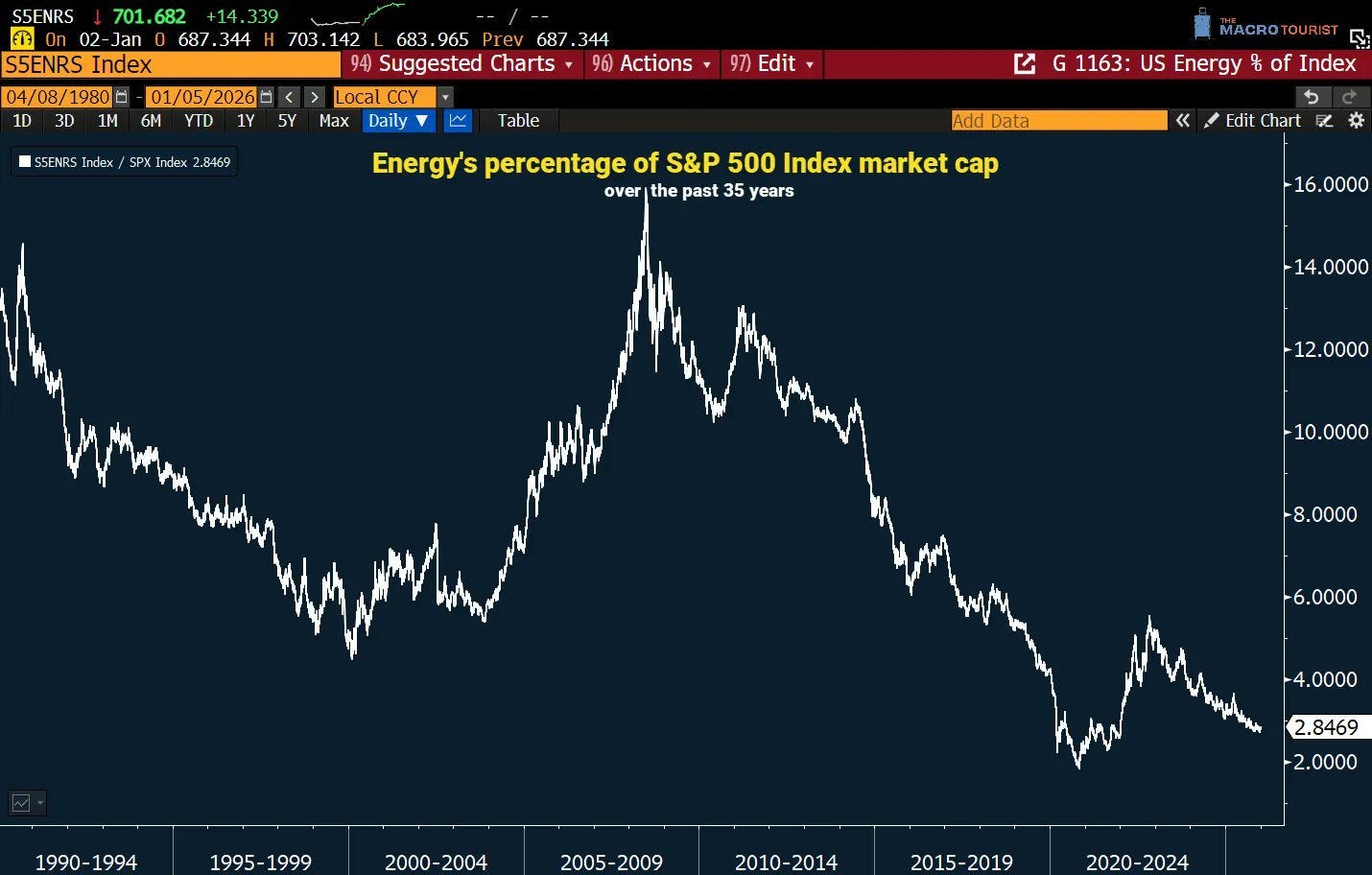

Given the cyclical nature of the oil market, the best time to invest in oil equities has historically been when prices are low and the sector is out of favor, as those are precisely the conditions that lead to future outperformance. Those conditions are now clearly present:

As production declines in response to underinvestment, oil prices are likely to rise, pulling service activity higher with them. One of my most compelling ideas, which I discussed in Cashing In on Gavin Newsom’s Presidential Ambitions – The Biggest Winner from California Energy Policy Moderation, has significant leverage to this upside and an unconventional margin of safety.

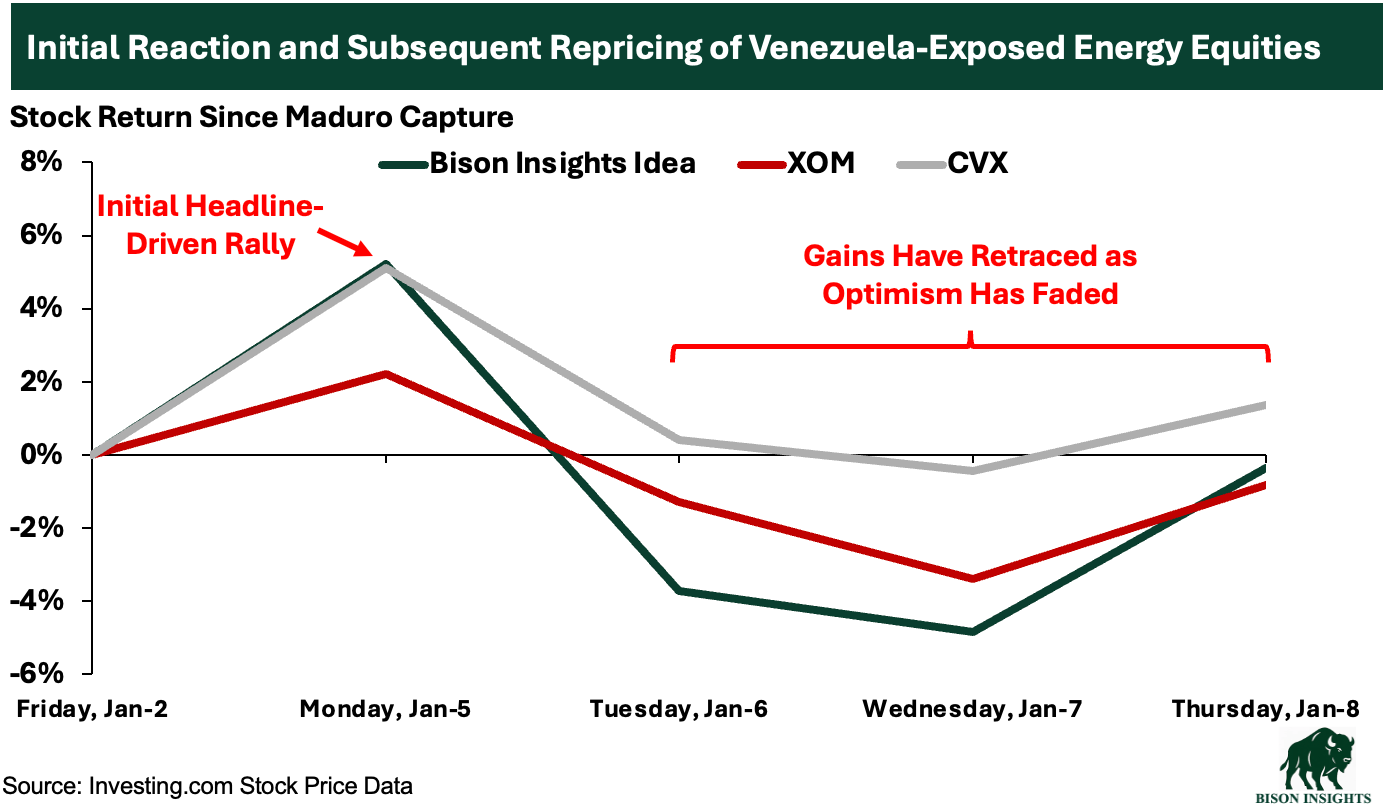

That company also has some exposure to the reopening of Venezuelan oilfields. This exposure is marginal and not the reason I own the stock, as any meaningful benefit from Venezuela may be years away. The market appears to share this view, as this company and other perceived Venezuelan beneficiaries such as Exxon and Chevron have given back their initial gains following news of Maduro’s capture:

I’ve also highlighted several other high-upside potential opportunities that stand to benefit from a recovery in oil prices, including:

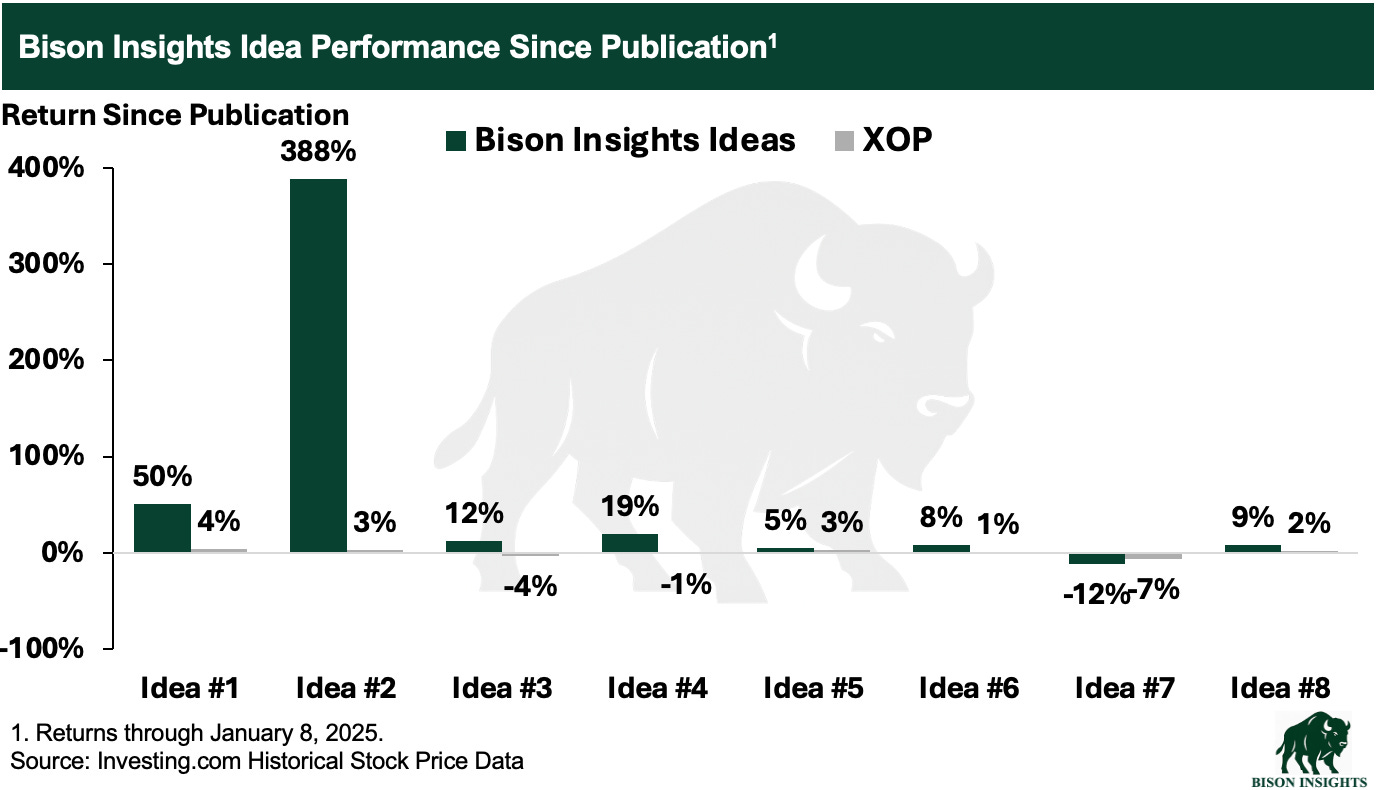

Overall, the performance of the ideas I’ve written about has been strong relative to the broader energy market, as measured against the Oil & Gas Exploration & Production ETF (XOP):

I’m excited about the next idea I’m working on, which I expect to publish in the coming weeks. It’s another high-upside oil opportunity, and I’ll also continue sharing my broader views on the oil and gas market along the way. Due to strong demand, I’ve extended my 50% off New Year’s sale through the end of the month, which can be accessed here:

Bottom Line

Oil producers don’t respond to political rhetoric. They respond to profit incentives. When prices are pushed below the level required to sustain supply, production falls, and prices eventually rise to restore balance.

Today, oil prices are low, investment is falling, and the sector is deeply underowned. Those conditions have historically marked the beginning, not the end, of periods of outperformance for oil equities, and is the backdrop against which I’m positioning today.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance may not repeat itself. These are the personal views of Josh Young, and do not represent any other individual or organization.

Outstanding article, and this needs to be recorded on a podcast and explained to more people- if there was only a podcast that was ranked #3 in the world for Energy podcasts, and we knew who that was. ... if only.....

It's been a very bizarre week. American companies are going to race into VZ spend their own money to drive the price down to fifty bucks?. That lesson was Trumps first term.