Update on Distressed Oil Company with Asymmetric Upside Potential

By popular request - I analyze a recent development and lay out my view of the updated downside, base and upside cases.

Over the last several weeks, I’ve been writing about a distressed oil producer whose stock was crushed by a punitive preferred financing structure layered on top of a large and valuable asset base.

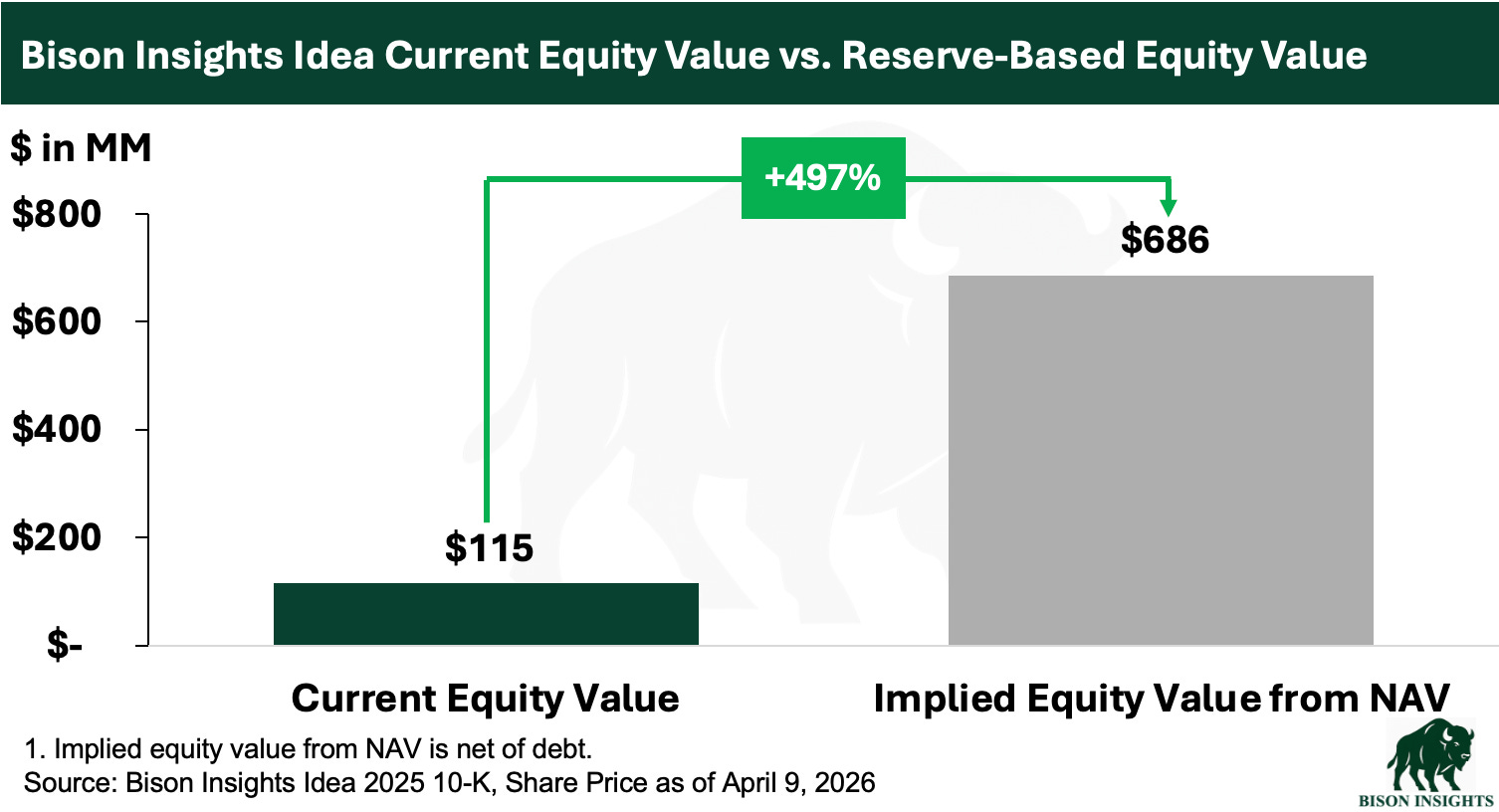

The company has substantial reserve value and equity upside potential, but investors have been focused on the risk that the preferred financing structure could yield high share dilution, and as a result have pushed the equity to a very low valuation:

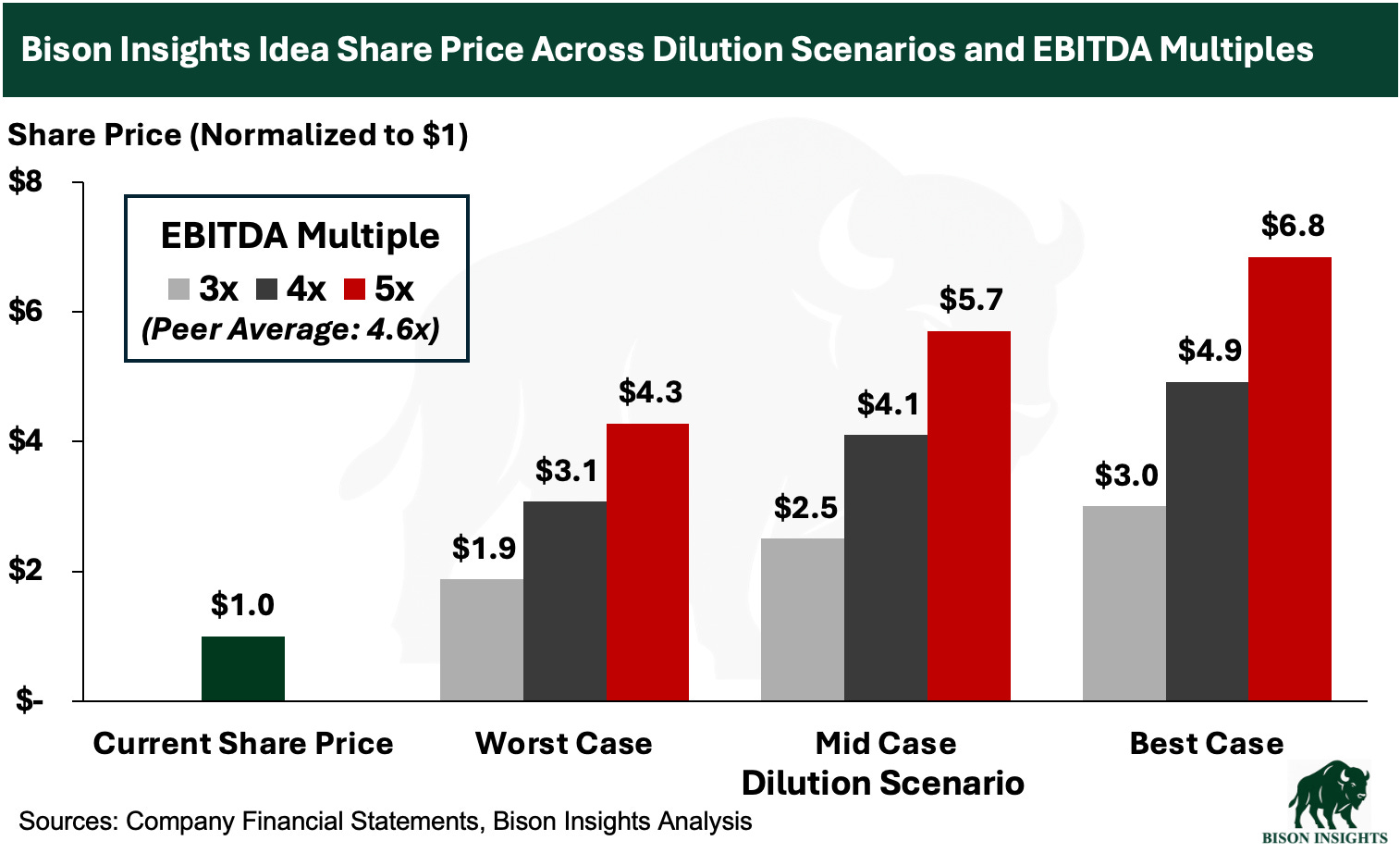

Recently, the company provided a key update that changes the dilution math. The new agreement isn’t a clean win for common shareholders, but the upside case is mostly intact. Also, the downside case outcome is likely much less severe than what had been possible before this development.

The key question now is straightforward: how many common shares will ultimately be outstanding once the preferred financing is gone? No matter the scenario, the upside appears compelling from here:

In the update below, I walk through the new agreement, estimate the likely ending share count, and then revisit what that implies for valuation.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance may not be indicative.