Update on Distressed Oil Stock With Huge Potential Upside

A company I’ve been following closely just released its annual results. In this article, I identify the company to all readers and share my updated analysis and expectations.

Over the last several weeks, I’ve been closely following a distressed oil stock, Prairie Operating ($PROP), that I originally wrote about it in “10x or Bust: An Asymmetric Distressed Oil Company Idea in the Midst of Soaring Oil Prices.” I’ve made that original article available to all readers, so that newer subscribers can review the background before this update, and so that free subscribers have a better idea of what I’m up to here on Bison Insights.

The basic thesis is straightforward: owning an undervalued DJ Basin producer with substantial reserve value and cash flow potential, with a stock price crushed by management issues and legacy financing issues - at a time when those issues may be fading into the rearview mirror.

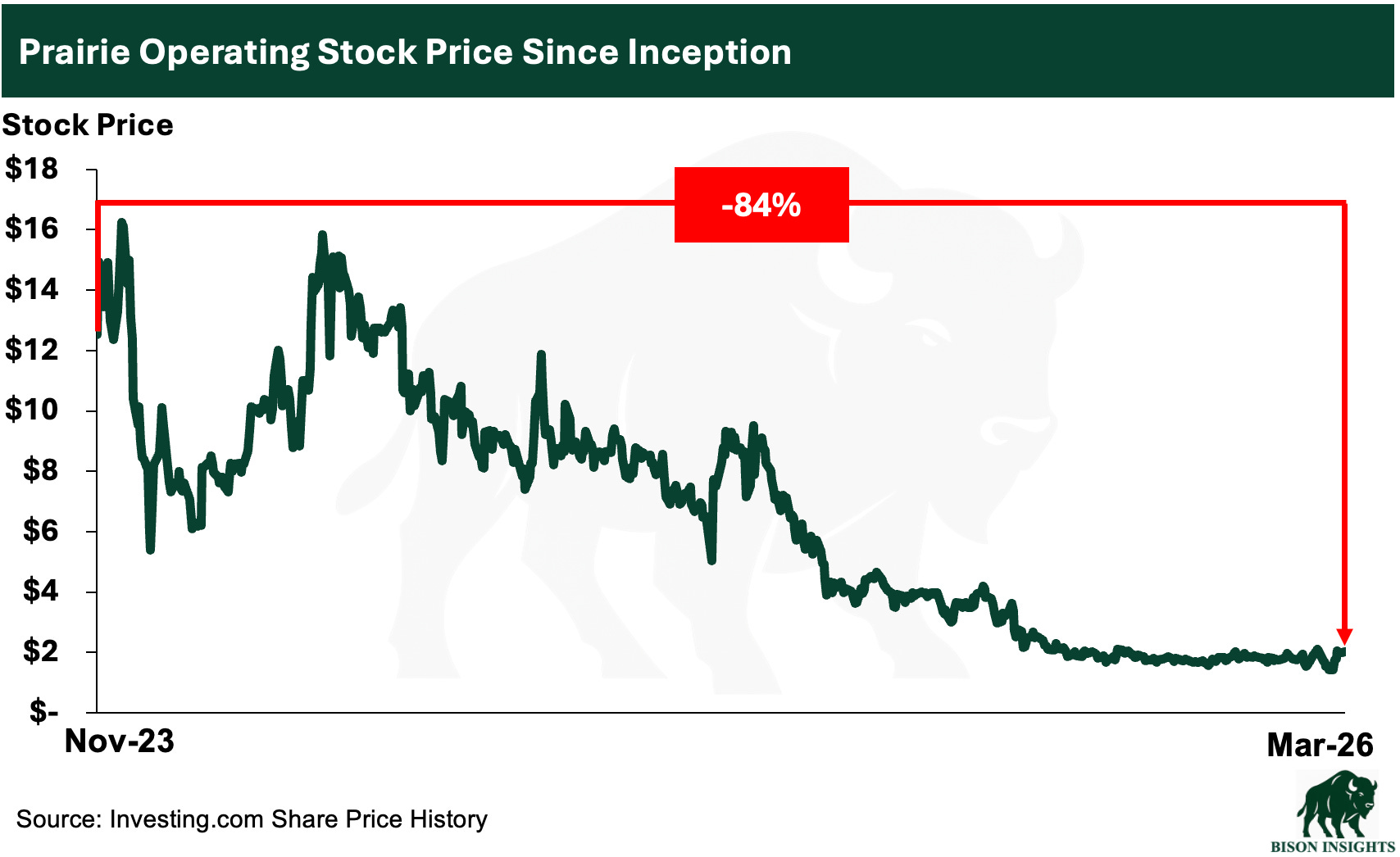

The financing issues included a punitive Series F preferred financing with strong holder protections, including conversion rights and a large warrant package that threatened substantial dilution to the common equity. These issues have driven substantial share price underperformance:

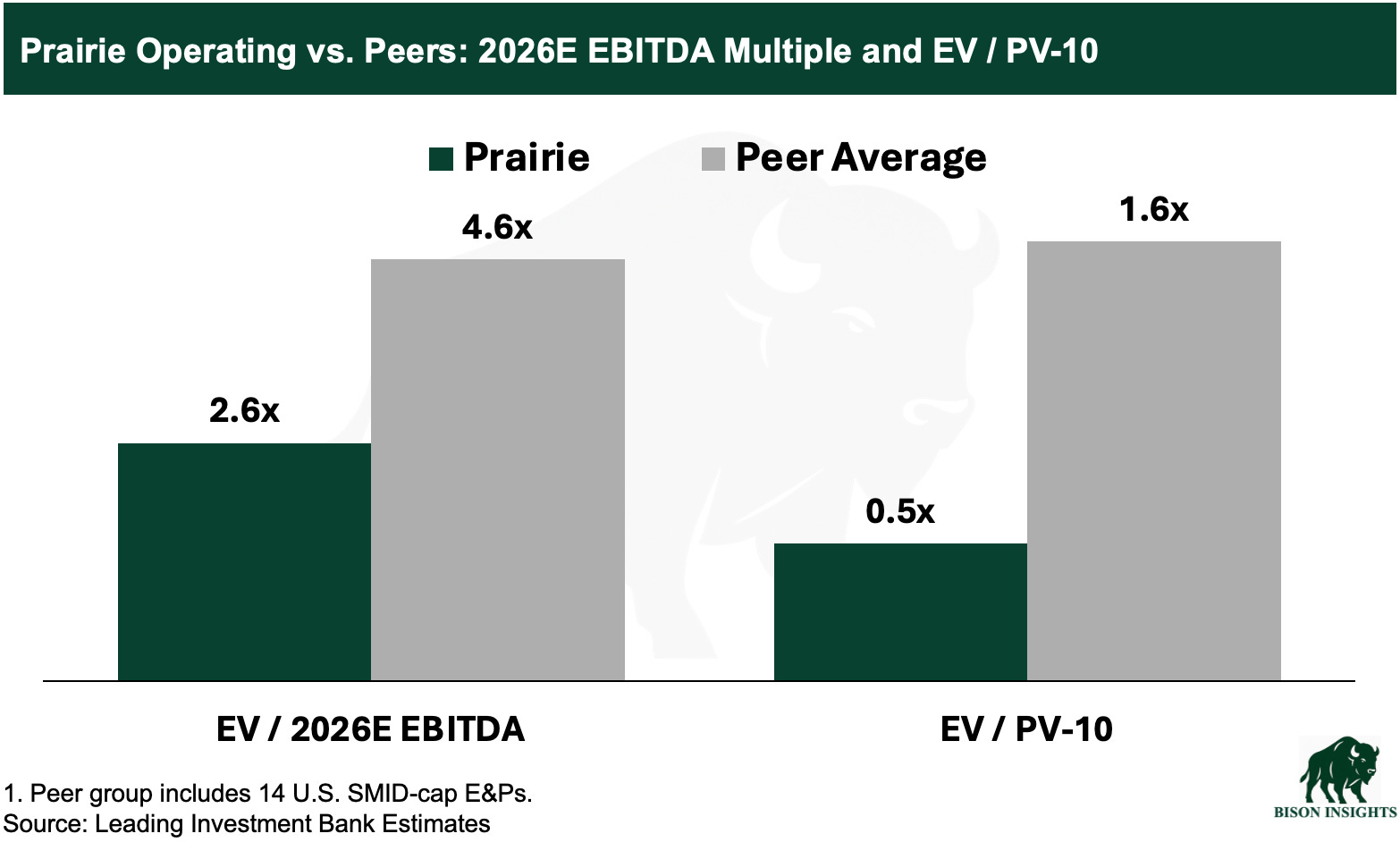

In my view, that stock price underperformance has been excessive — Prairie now trades at a very low valuation relative to its reserve value and cash flow:

With that in mind, I followed up my original write-up with “Catalyst Days Away in a Distressed Oil Stock with 10x Potential Upside,” where I analyzed the possible refinancing outcomes for the Series F preferred and what each could mean for the stock price.

One day after I published that piece, the company announced an extension of the warrant issuance deadline for the Series F preferred to April 7, 2026, postponing final clarity on how that overhang will be resolved.

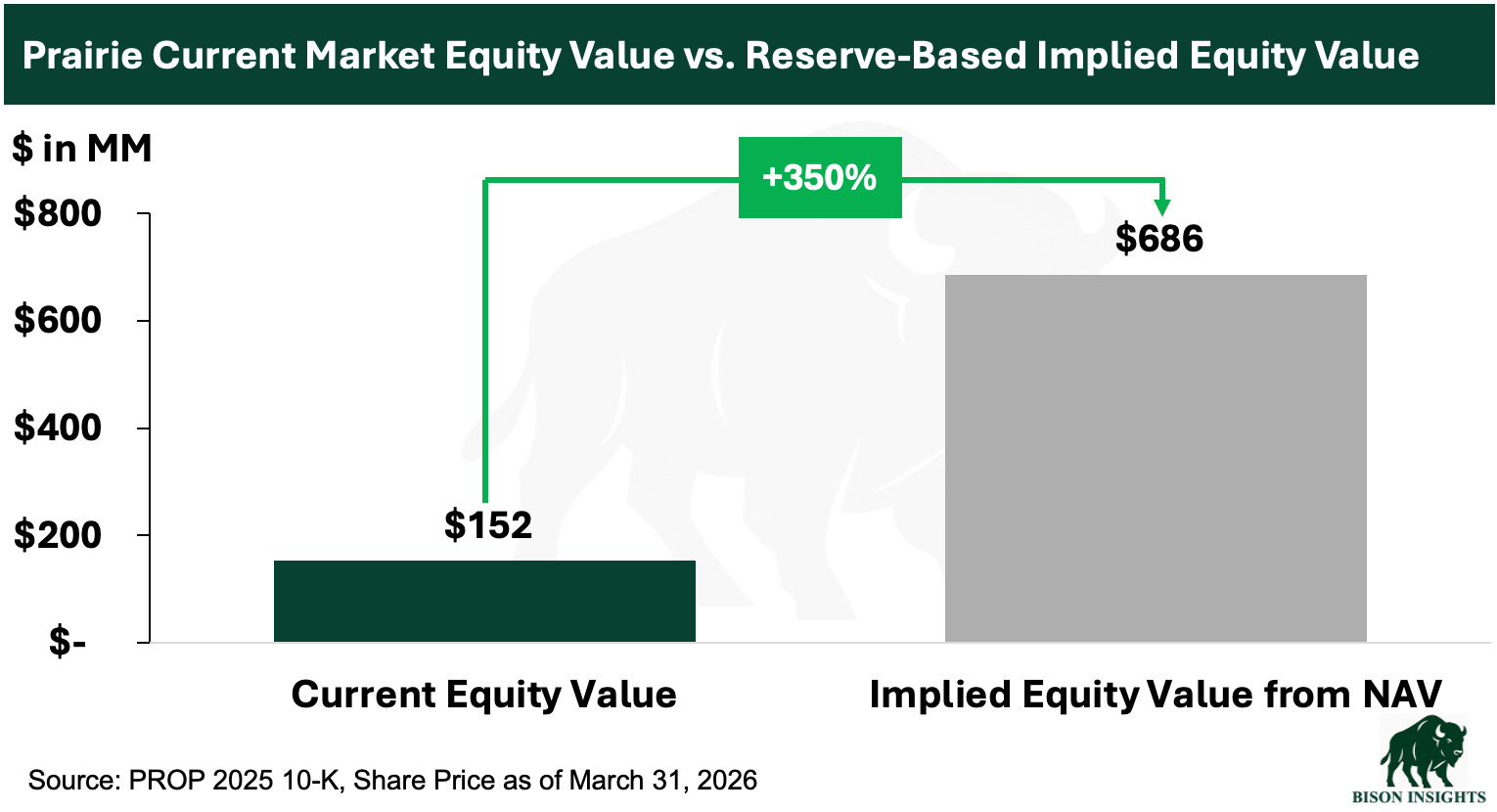

While that extension delayed the catalyst, the company’s annual results, released yesterday, offered an important reminder of the value that sits underneath the capital structure overhang. In the report, Prairie reaffirmed its PV-10 reserve value at approximately $1.2 billion, which after subtracting net debt, implies an equity value roughly 350% above the company’s current market cap (which importantly does not incorporate recent much higher oil prices):

In the update below, I walk through my updated view on the annual results and recent earnings call, and how I think the stock may trade after the announcement of Prairie’s final Series F outcome.

Disclaimer: I and funds I advise own Prairie Operating shares and related securities and may buy or sell them at any time without further notice. This is for informational and educational purposes only and is not an offer, solicitation, or investment recommendation. There can be no assurance of return or accuracy, and past performance may not be indicative. Please do your own diligence and consult an advisor if appropriate.