Update On Undervalued Oil Producer That is Buying Back Stock and Paying Off Debt

Alternative perspective from an even more bullish analyst.

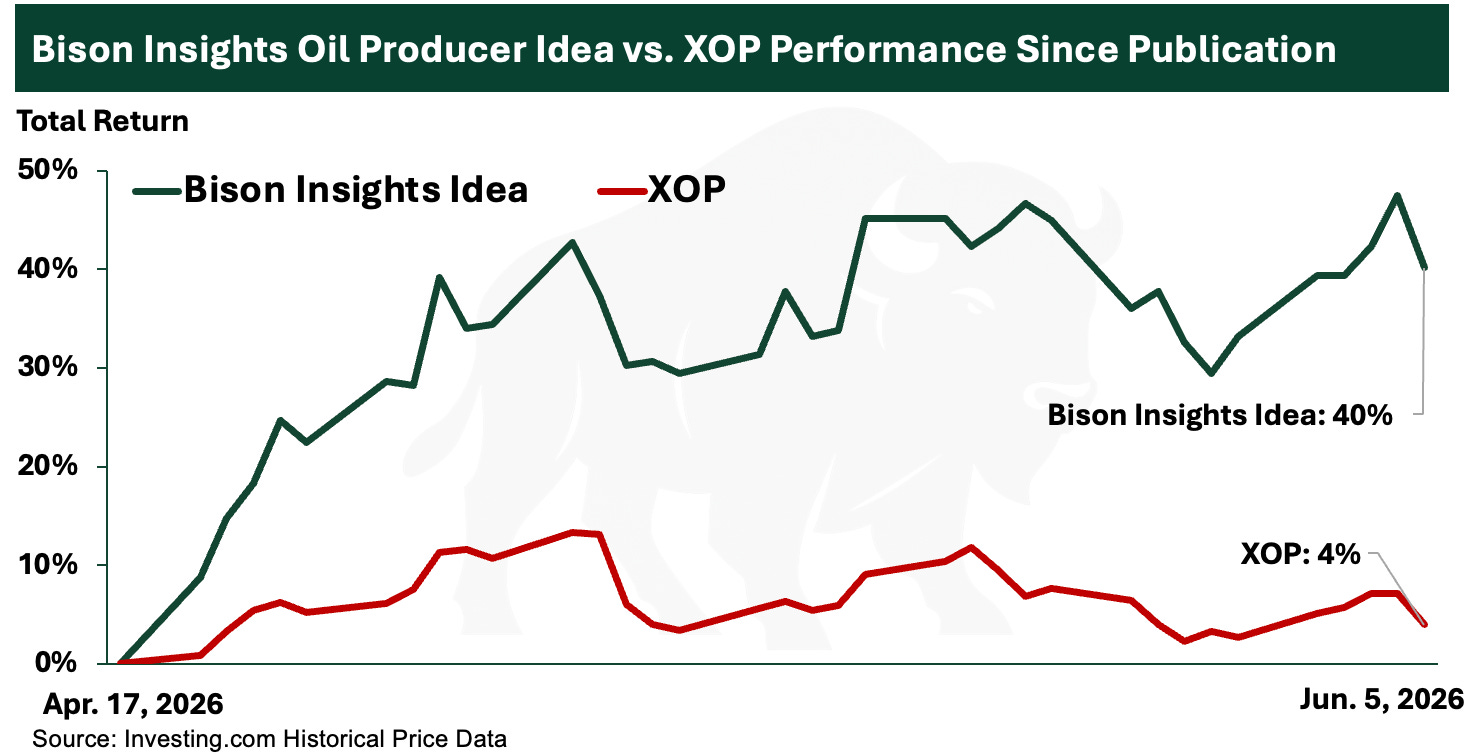

In April, I wrote about one of my favorite oil producer stocks, which has a lot of potential upside to higher oil prices, in This Undervalued Oil Producer is Buying Back Stock and Paying Off Debt. Since publication, the stock has performed well against the broader energy space, as measured by the energy XOP ETF:

The stock has oil weighted production and high cash flow sensitivity to rising oil prices, and it’s using that cash to rapidly deleverage. It has also consistently beat production expectations over each of the recent several quarters.

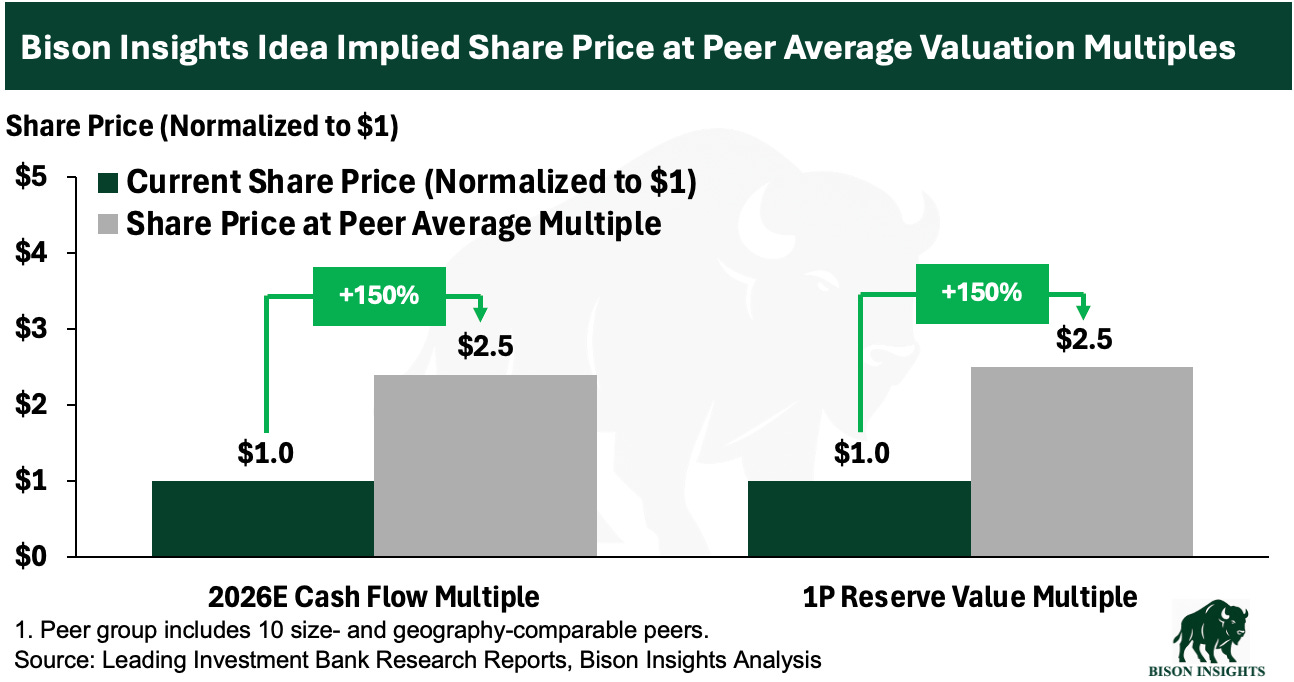

As it cleans up its balance sheet and continues paying down debt, I think the stock will close its large discount to peers, implying substantial future upside from here:

Occasionally I am reminded of the conservatism of my assessments. I recently came across another analyst’s work on this company, who was considerably more bullish on the stock than I am. I find it is helpful to consider alternative perspectives in both directions on current and prospective investments, so I share his take and my interpretation of it below.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance is not indicative of future results.