This Large Cap Oil Producer is Outperforming, With More to Come

I usually write about small-cap oil stocks on Bison Insights, but back in December I shared my thesis on a large-cap company trading at an unwarranted discount to peers, with upside from improving refining margins and a highly accretive but misunderstood acquisition. I even published an interview with an industry expert with directly relevant experience, who helped provide more detail on what the market was missing about the assets - high return development upside and optimization potential.

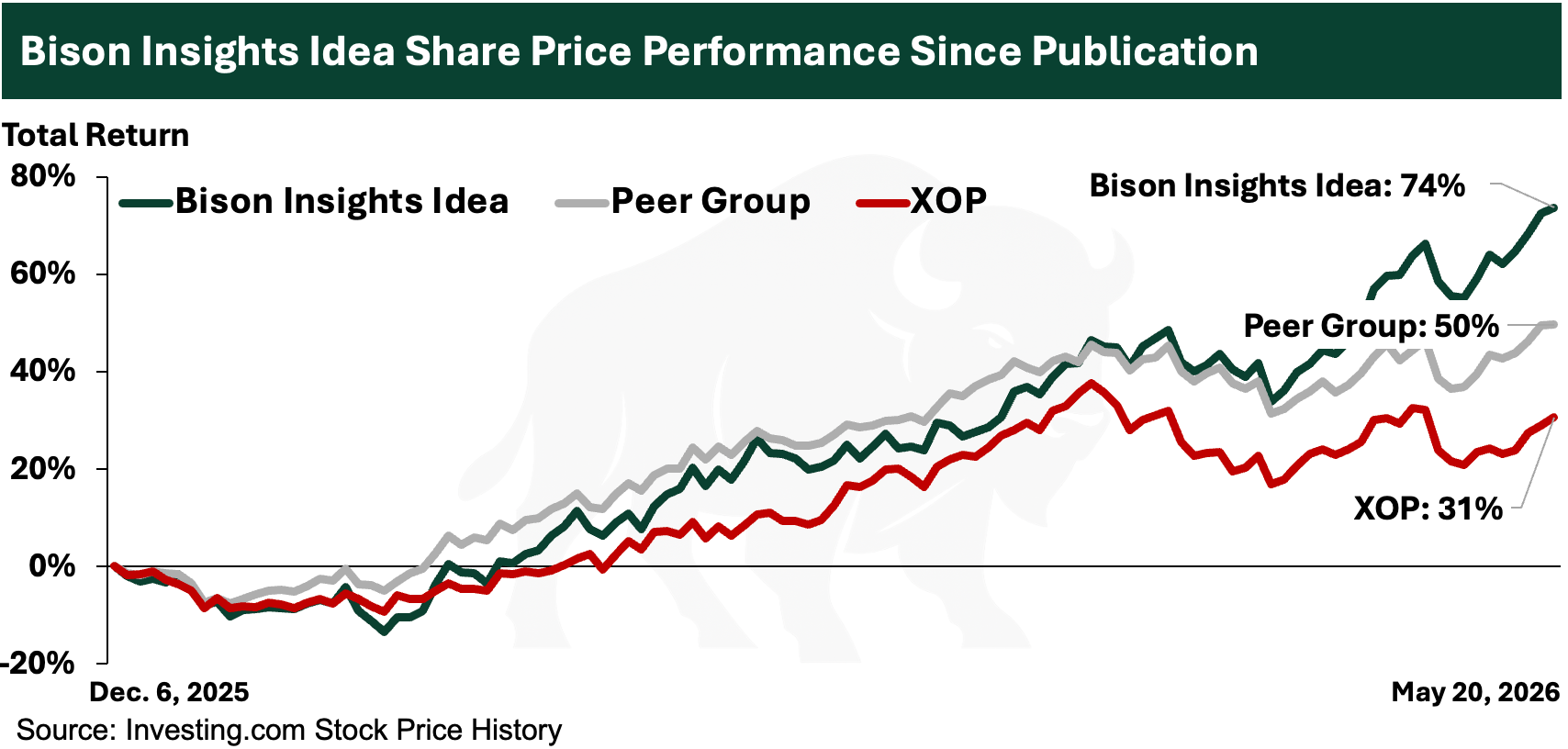

Since publication, the thesis has played out nicely. Of course, the substantial rise in oil prices has helped, but the performance of the shares of this particular company has substantially exceeded its own peer group and the broader oil and gas space:

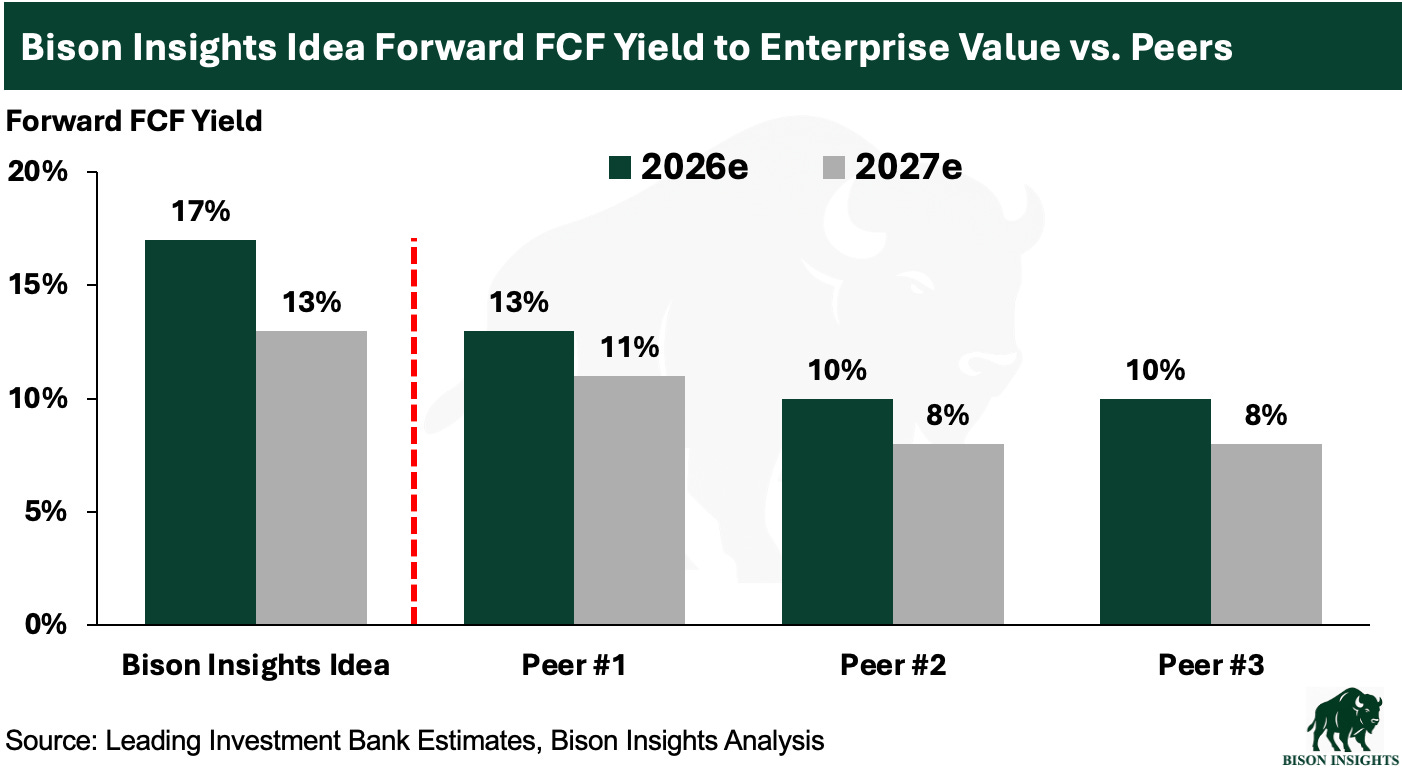

Despite this outperformance, the company still trades at a very attractive valuation and discount to peers. My own analysis and consensus forecasts estimate that the company trades at a higher expected forward free cash flow yield than its closest large-cap peers, at a compelling 17% fcf yield:

The discount reflects two issues that the market appears to be hanging onto but have recently inflected:

A period of heavy capital investment in non-producing assets, which have now flipped from cash flow negative to cash flow positive.

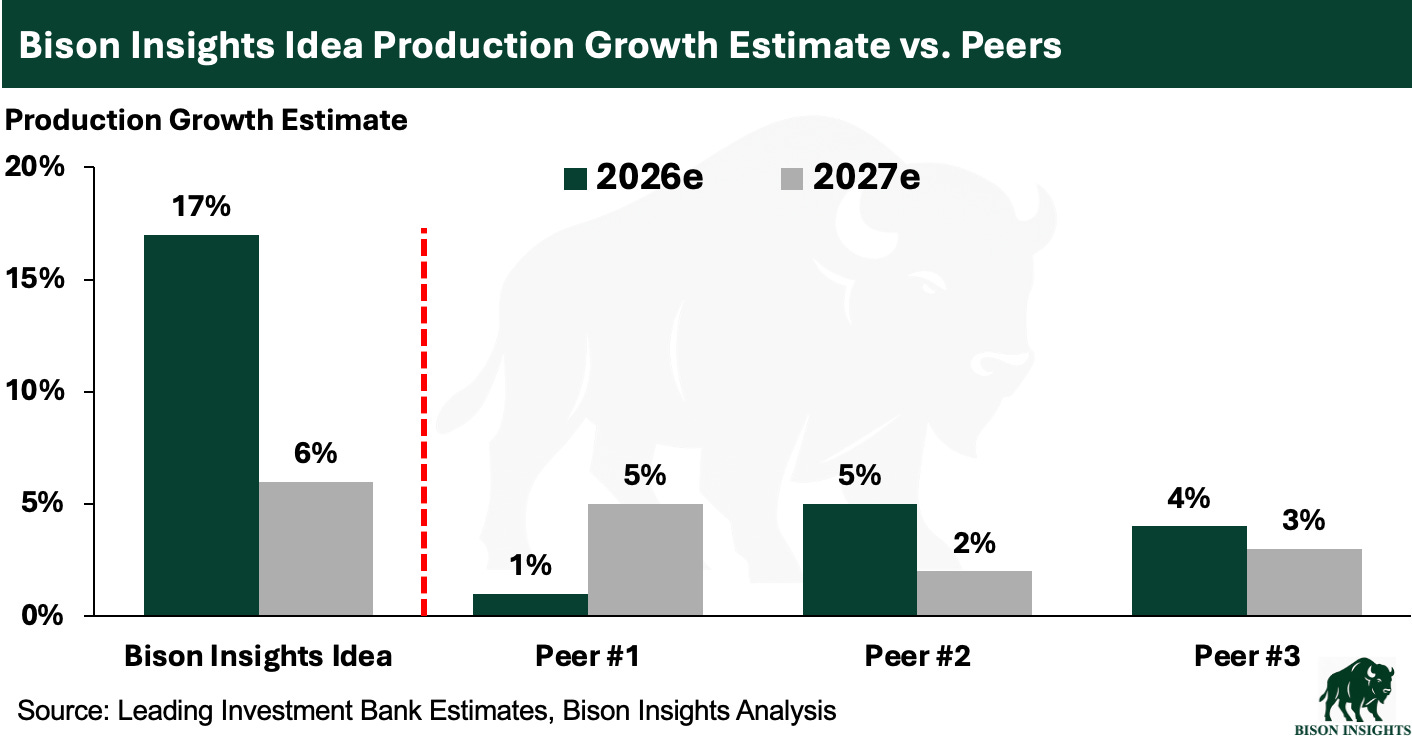

A key acquisition that was broadly misunderstood by the market, and which is now driving high production growth and enormous returns on investment.

This high production growth makes the current high free cash flow yield even more attractive, because this company isn’t only generating high free cash flow, it’s also growing:

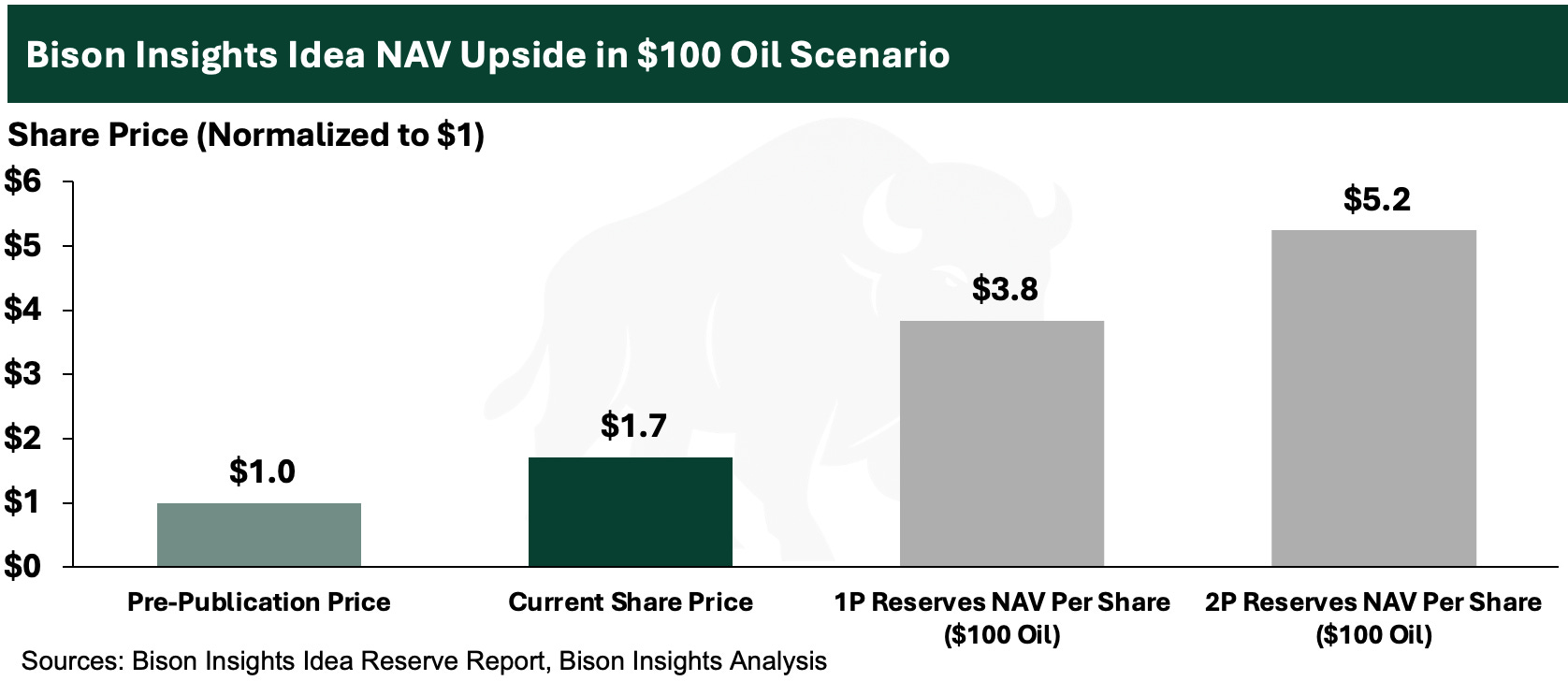

This company is also deeply undervalued compared to its likely net asset value at $100 oil, trading at a large discount to the value of its enormous reserves. It has high upside to higher oil prices, and should still have some upside if oil prices decline back to pre-war levels.

Below, I share my updated view on the stock.

Disclaimer: This is for informational and educational purposes only. This is not an offer, solicitation, or investment recommendation. Please consult an advisor and do your own diligence. Past performance may not repeat itself.